What is a Balance Sheet?

A balance sheet is a financial statement of an enterprise. It is one of the three primary financial statements used in analysing a business or modelling forecast for a business. Other two include the income statement and cash flow statement.

It shows the financial positions of business in a given period and includes critical information like the value of assets, liabilities, cash and shareholders’ equity. In this way, a balance sheet enables the information seeker to evaluate the net worth of an enterprise.

Good read: Evaluating Financial Statements

The balance sheet is a source of information for a number of stakeholders, including investors, creditors, bankers. It helps stakeholders to make efficient decisions and provide transparency.

Enterprises are primarily judged on the financial position, which is based on the income statement, balance sheet and cash flow statement.

The balance sheet is also referred to as Statement of Financial Position and is applied, along with other financial information, in deriving financial ratios, financial modelling, stress testing, credit appraisal, credit rating etc.

It reflects the position of an enterprise during a given period, which could be quarterly, semi-annual, and annual. Corporations are required to publish financial information regarding the business under different laws across jurisdictions.

Why does the balance sheet balance?

Balance sheet is balanced because of the double entry bookkeeping system, which necessitates the effect of transaction on two accounts. For instance, an entrepreneur starting a business with $5000 cash will increase cash (Assets) and capital (Shareholder’s Equity). The below equation is the result of double entry bookkeeping system.

Assets

In the assets section, balance sheet represents the value of a business which can be converted to cash and is owned by the enterprise. Assets represent the ownership of an enterprise. Companies derive assets through transactions, investments, acquisitions, internal developments etc.

Assets are generally recorded at a cost which was paid at the time of transaction. But conservative accounting principle necessitates companies to record assets at current costs, and the difference between actual cost and current cost is charged to profit and loss account.

The balance sheet does not include internally generated assets like Domino’s Pizza Logo, McDonald’s logo that are valuable for business. However, such intangible assets are recorded in the balance sheet when an enterprise purchases intangible assets or acquire by way of business combinations.

Companies are required to report assets less than costs at times like anticipated losses from a receivable are charged to the income statement, and receivable are reduced by same amount in the balance sheet.

Depreciation and amortisation is the process charging expenses of long-term assets to the income statement and reducing the same amount from the balance sheet value of long term assets.

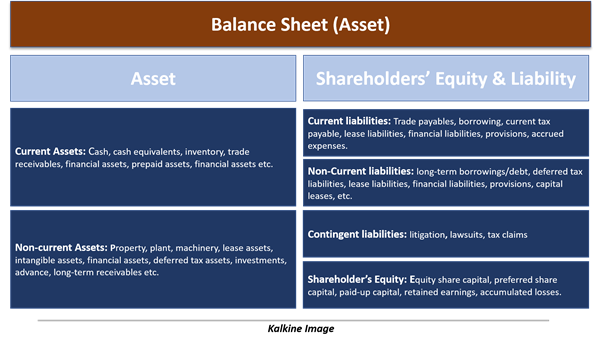

There are two types of assets: current assets and non-current assets

Current Assets: Current assets are those assets that could be realised in cash in one year. These assets include cash, cash equivalents, inventory, trade receivables, financial assets, prepaid assets, financial assets etc.

Current assets also indicate the expected amount of cash a business can potentially convert over one year period. It also includes assets held for sale purpose. Current Assets are used to calculate working capital and other financial ratios.

Non-current Assets: Non-current assets are those assets that would not be converted into cash easily. These are long term assets of the business and expected to generate long term benefits for the business.

Non-current assets include property, plant, machinery, lease assets, intangible assets, financial assets, deferred tax assets, investments, advance, long-term receivables etc.

Liabilities

Liabilities represent the obligations of an enterprise. It can be the source of assets and also represent a claim on assets of an enterprise. A liability is recorded as a result of past event or transaction, and settlement of liability is expected to result in an outflow of funds, resource or economic benefits.

There are three types of current liabilities: current liabilities, non-current liabilities and contingent liabilities.

Current liabilities: Current liabilities are short term commitments of an enterprise that are needed to be settled within one year. It reflects the amount of funds that would be required by an enterprise to pay-off its short-term obligations.

Current liabilities include trade payables, borrowing, current tax payable, lease liabilities, financial liabilities, provisions, accrued expenses. Information seekers use current liabilities to evaluate the liquidity of an enterprise and various other ratios.

Non-current liabilities: Non-current liabilities are also known as long term liabilities of an enterprise because these are due after one year. A company with a loan maturing in ten years’ time will be required to report principal amount under non-current liabilities.

Non-current liabilities include long-term borrowings/debt, deferred tax liabilities, lease liabilities, financial liabilities, provisions, capital leases, etc.

Contingent liabilities: Contingent liabilities are the obligations of a firm that could become due to the outcome of a future event. Moreover, these are potential obligations of a firm. A common example of contingent liabilities could be litigation against the company, which may force it to pay money upon judgement.

Shareholder’s Equity

It is the amount of capital the owners or shareholders of an enterprise have provided to the business. Shareholder’s equity also includes the amount of cash generated by the business after repaying all necessary obligations in a given period.

Shareholder equity includes equity share capital, preferred share capital, paid-up capital, retained earnings, accumulated losses. Negative shareholder equity would mean that the liabilities of the company exceed assets of the company. A positive shareholder’s equity indicates that the company has surplus assets over liabilities.

Please wait processing your request...

Please wait processing your request...