What is opening stock?

The quantity of goods/ products held by an organization at the beginning of an accounting or financial year is known as opening stock. The opening stock at the beginning of a year is equivalent to the closing stock of the previous year. The value of the stock is dependent upon the accounting norms adopted by an organisation and the nature of the business.

Summary

- The quantity of goods/ products held by an organization at the beginning of an accounting or financial year is known as opening stock.

- The opening stock at the beginning of a year is equivalent to the closing stock of the previous year.

- The value of the stock is dependent upon the accounting norms adopted by organisations and the nature of the business.

Frequently asked questions (FAQs)

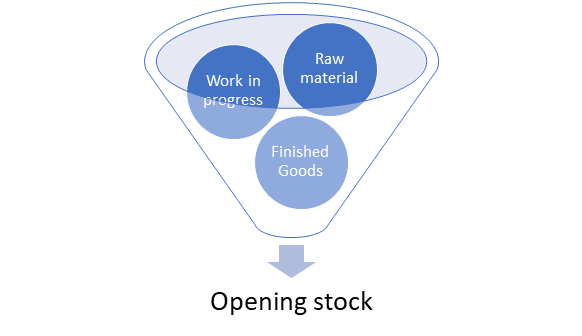

What are the types of opening stock?

The inventory type held by an organisation depends upon the nature of the business. For example, the inventory will be different for a retailer, service providers and a manufacturing firm. However, the inventory can be categorized into three types –

Raw material – It is the most common form of inventory. Raw material stands for the material that has not been processed or transformed into the final goods. Presence of raw material in the opening stock projects that the material has been purchased and stored.

Work in Progress – Under this inventory type, the raw material has undergone the transformation, conversion, and modification phase, but the raw material is not processed completely. The inventory needs to be processed further to sell it in the market.

Finished goods – It is the last stage of manufacturing or production, in which the final good has been created and is complete in all aspects. The finished goods are ready to be sold in the market.

Source: Copyright © 2021 Kalkine Media

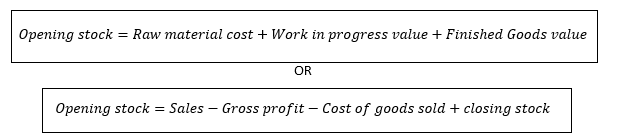

How to calculate opening stock?

The formula for calculating the opening stock is dependent upon the information available –

What is the journal entry for opening stocks?

Usually, the opening stocks are carried over from last year’s closing stock. The opening stock account will be credited when the closing stock is bought forward. However, the trading account is debited as opening stock is taken from the trading account when the carry forward transaction is conducted in the new accounting or financial year.

What is the difference between opening and closing accounts?

- Closing stock can be defined as unsold or unprocessed goods at the end of a year. The opening stock’s value is like the closing stock as it is carried forward from the closing stock only.

- Opening stock is the number of goods at hand for sale in the new year. But the closing stock is the unsold goods.

- Both closing and opening stock includes raw material, finished goods and work in progress inventory.

Image source: © Chrismoncrieff | Megapixl.com

What are the advantages of opening stock?

- Opening stock presence can help the organisations to meet the market demands and fulfil the customer needs.

- Customer satisfaction is enhanced as opening stock ensures a better supply of goods and services.

- The raw material presence ensures the smooth functioning of the manufacturing process and the timely delivery of the finished products and services.

What are the limitations of opening stock?

- A holding cost is associated with the inventory. If the large inventory is available in the stores, then it adds cost for the organisations in terms of the storage rent, time value of money on the inventory and so on.

- The market conditions are always changing, and it adds risk for the organisations as the unsold goods can become obsolete.

- The risk of loss is adjoint with the opening stock, which is, the risk of theft or damage.

- The presence of a large amount of opening stock indicates the company’s inability to sell its products and can be seen as a negative aspect by the stakeholders.

What are the accounting rules for opening stock?

- Numerous amendments have been introduced in the accounting standards, and accounting assumptions. Therefore, the way opening stocks should be treated has been changed, in terms of calculation and accounting disclosure.

- Generally, stocks are recorded by retailers or manufacturers. However, now service providers also must record opening stocks in their books. For a service provider, the stock will be stationary.

- Opening stock calculation plays a significant role as it has a direct impact on the profitability of organisations.

- The opening stock calculation not only considers the product in which the company deals but it also considers the spare parts or the inventory of capital assets.

Where is opening stock recorded in a balance sheet?

Opening stock is an asset for the organisations and is categorized as a current asset. The opening stock technically is not recorded in the balance sheet as the balance sheet is constructed on a specific date, that is, the ending of the financial or accounting period. Therefore, only the closing stock is recorded in the balance sheet.

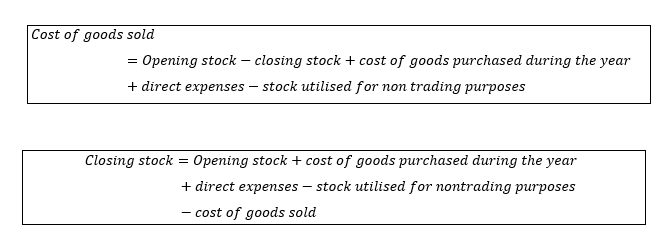

How opening stock is used?

Opening stock is primarily used for calculating the value of the cost of goods sold. The formula for cost of goods sold is –

Moreover, the average inventory is calculated with the help of the opening stock. Average inventory is utilized for calculating the inventory turnover which projects the organizational performance. The closing stock can also be used for the formula but using an average of opening and closing generates a smoothing effect.

What calculations are associated with the opening stock?

Please wait processing your request...

Please wait processing your request...