What is a standby letter of credit (SBLC)?

Unknown sellers and buyers use a standby letter of credit (SBLC) for international or domestic transactions. By using an SBLC, they try to hedge risks associated with the transaction. The risks hedged include bankruptcy and insufficient cash flows with the buyer for making timely payments to the seller. An SBLC comes with a promise from the bank to ‘make good the dues’ in case of any adverse events. However, the payment is a credit on the buyer, who is then obliged to pay principal and interest to the bank. The SBLC underlines the conditions and interest details on the face of the document. The bank doesn’t have any interest in the transaction being hedged by the SBLC.

Summary

- A standby letter of credit (SBLC) is an instrument valid by law and issued by a bank for its client, guaranteeing their payment dues under a transaction.

- It is commonly used in international and domestic sale-purchase agreements involving unknown parties.

- An SBLC acts as a safety net for the seller, provided by a bank on behalf of the buyer if they fail to make the payment on time.

Frequently Asked Questions (FAQ)-??

How does SBLC work?

An SBLC issued by the bank works like insurance. However, collateral is needed by the bank to protect itself in a default situation. The collateral amount and size of the SBLC depend on the risk involved and the client’s business strength.

In a sale contract or a shipment of goods, the buyer gets an SBLC issued from their bank, known as ‘issuing bank’. This SBLC issued then reaches the buyer’s bank called the ‘advising bank’. The advising bank then confirms the SBLC with the seller. In this way, the sale contract gets executed with an insured payment from the buyer to seller via an SBLC.

Before releasing an SBLC, the issuing bank primarily considers the repayment capacity of the client on whose behalf the SBLC will be issued. Once the bank completes its due diligence regarding the client for whom it is issuing the SBLC, it provides a letter to the client. Upon receipt of the letter, a fee is payable by the client for each year that the Standby Letter of Credit remains outstanding.

Source © Maslahkhatulkhasanah | Megapixl.com

How is SBLC different from a letter of credit (LC)?

Both letters of credit (LC) and a standby letter of credit (SBLC) are issued by a bank on a buyer’s request for international trade. The basic difference, however, is that an SBLC is payable even on non-fulfilment of conditions. However, an LC guarantees payments only when the buyer meets certain specifications and all documents are received from the seller’s advising bank. Other Key differences are the following.

- Performance Clause-

An LC has basic documentation, packing, etc., but is still a plain instrument. An SBLC, on the other hand, can have specific clauses buyers must fulfill before using the instrument. Thus, SBLCs come with certain performance criteria.

- Issuing bank’s requirements-

Before issuing an LC, the issuing bank measures the buyer’s credit score and repayment capacity. Also, LC is usually issued by a bank with long-term relations with the buyer asking for LC. Therefore, LC is usually unsecured. However, an SBLC is obligatory on the bank, therefore issuing bank asks for collateral to secure itself against an SBLC.

- Purpose-

An LC is issued primarily to use for the completion of a transaction. It gives assurance to the seller that the buyer will make payment for the goods supplied. It is, therefore, a standard payment document used in international transactions involving unknown parties. In contrast, an SBLC is a secondary payment instrument used only if something goes wrong at the buyer’s end.

- Time period-

An LC is a short-term instrument, with an expiry usually up to 90 days. Whereas an SBLC is a long-term instrument, having validity of one year or more. A standby letter of credit is often used to provide security for a long-term obligation such as a long-term construction project.

- Geographical coverage-

An LC is often used for undertaking export-import transactions. However, an SBLC can be used in a global or domestic transaction, thus having a wider scope in terms of geographical coverage.

- Issuance cost-

An SBLC is often more expensive than an LC. Banks charge higher for issuing an SBLC, which covers a longer time duration.

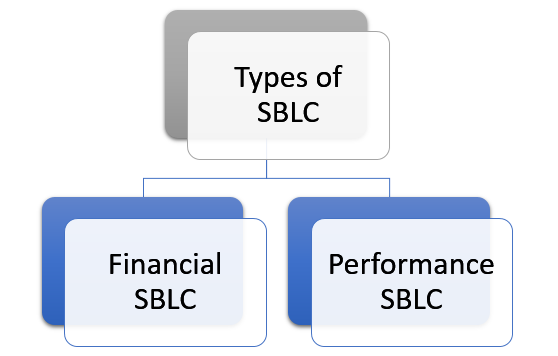

What are various types of SBLC?

There are basically two main types of SBLC-

Copyright © 2021 Kalkine Media

- Financial SBLC-guarantees payment as specified in the agreement. If a buyer does not make payment on the required date, the seller can demand payment from the buyer’s bank. Since under SBLC the amount paid remains a credit on the buyer, the bank collects a principal and interest later from the buyer. Before issuing a financial SBLC issuing bank will evaluate the buyer’s repayment capacity and credibility. In case it is found questionable, bank issues the SBLC against collateral.

- Performance SBLC- guarantees completion of work under a project within a pre-fixed schedule. On non-performance of contract within schedule, the bank promises to reimburse the seller with a certain amount of compensation. Thus, payment under a performance SBLC functions as a penalty to encourage an on-time completion contract.

What are the advantages of SBLC?

Image Source © Rawpixelimages | Megapixl.com

- An SBLC eases out risks posed by worse case scenarios in the international trade of goods and services.

- If pirates or the goods carrier steals the shipment meets with an accident, the standby letter of credit will still work to make the seller’s losses good.

- The seller is eligible to present the SBLC to the issuing bank for payment. It also mitigates the risk of an order getting changed or cancelled by the buyer.

- SBLC’s, therefore, encourage global trade by reducing uncertainties involved in dealing with unknown or new parties globally.

- In addition, small businesses can gain a competitive edge over bigger and well-established market rivals.

- Further, an SBLC reflects on the credibility of the buyer in front of a seller.

Please wait processing your request...

Please wait processing your request...