What is Zero Liability Policy?

Zero liability policy refers to the provision or condition in the contracts of credit card that says the credit card holder is not accountable for unauthorised charges. The Zero liability policy, which is being offered by the issuers, states that a cardholder is not responsible to make payments for any unauthorised charges and a cardholder can’t be legally oppressed.

Copyright © 2021 Kalkine Media

Understanding Zero Liability Policy

The zero liability policy defines a provision or condition in the agreement of a credit or debit card which states that a card holder is not liable for any unauthorised transaction made in the card. The issuers of the credit cards provide protection to their cardholders and assure them that in case of any fraudulent charges that are detected by the issuer or reported will be removed from the cardholder’s account, and the account holder is not liable to pay for them. The issuers of credit cards offer zero-liability policies to attract the customers as they found risky to have a credit card and it reduces the revenues of the issuer of credit card.

Debit cards also provide with similar protections. A debit cardholder may suffer from some losses, if the cardholder is failed to report the unauthorised use of the debit card. However they are regulated under distinct federal regulation.

The providers of credit cards are largely accountable for managing and coping with the frauds of credit cards as per the federal law. The credit cardholder’s liability for losses is restricted to the maximum limit of $50 in case of potential for loss. Mostly credit and debit cards are issued with the restricted liability clause, but in case of debit cards, the issuer (bank) may make excuses for the losses due to lighter regulation of debit cards so a debit card holder should read the policy very well to ensure that a bank does not give any excuse at the time of losses.

Copyright © 2021 Kalkine Media

Frequently Asked Questions

How to implement Zero Liability Policy?

Zero Liability Policy is offered by the issuer of the credit cards and debit cards to attract individuals as they are risky. The provider of the credit card issues the card to an individual with zero liability policy for any misuse and fraud until the specified obligations have been completed. These include the credit card holder has to inform the issuer of the card as soon as any wrong and fraudulent transaction is detected and take best possible care to prevent the theft of the credit card. The cardholder is not liable for any unauthorised transactions made through a phone, app, online or in person. The zero liability policy in credit card is applied regardless of way of fraudulent transactions.

The issuer of credit card provides cards to customer with zero-liability policies because they may otherwise avoid using them as they do not want to involve them in high cost risks. Zero liability policies may not applicable to the transactions of all commercial credit cards or to all foreign transactions. The obligations and policies are clearly mentioned in the agreement of the cardholder.

What are the risks associated with Zero Liability Policy?

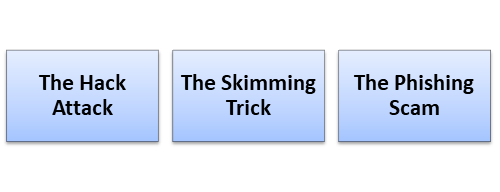

There are several risks around the zero liability policy. Some of them are:

Source: Copyright © 2021 Kalkine Media

- The Hack Attack: The hack attack is one of the most common risks associated with zero liability policy, where a hacker may have accesses the company’s databases such as retail store chain, online stores that has record of consumers information such as credit card. And then this information is sold in the black market to another criminal who uses this information to make unauthorised purchases. This is the reason customer may refuse to use credit cards without having zero liability policy.

- The Skimming Trick: The Skimming Trick refers to the process through which a criminal can interfere with a swiping device at store so that the criminal can access or capture the authorisation of purchase and the related account information at the time of use (purchase) and use it for other unauthorised transactions. In order to avoid this Skimming Trick, the credit cards transition designed that contain a chip.

- The Phishing Scam: The phishing scam is also a big risk for the customers. In a phishing scam, criminal sends a fraudulent message to the customers that goes out to a large number of possible victims in a bid that a few customers would fall in the trap. The message is sent by criminal as the trusted agency or company through an email, phone, or text message that asks for the account’s information of recipients, and it can be misused.

Please wait processing your request...

Please wait processing your request...