Company Overview: ABIOMED, Inc. is a provider of temporary percutaneous mechanical circulatory support devices. The Company offers care to heart failure patients. The Company operates in the segment of the research, development and sale of medical devices to assist or replace the pumping function of the failing heart. The Company develops, manufactures and markets products that are designed to enable the heart to rest, heal and recover by improving blood flow to the coronary arteries and end-organs and/or temporarily performing the pumping function of the heart. The Company's product portfolio includes the Impella 2.5, Impella CP, Impella RP, Impella LD, Impella 5.0 and AB5000. The Company's products are used in the cardiac catheterization lab (cath lab), by interventional cardiologists, the electrophysiology lab, the hybrid lab and in the heart surgery suite by heart surgeons.

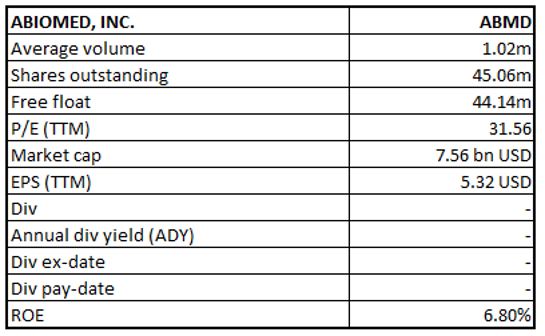

ABMD Details

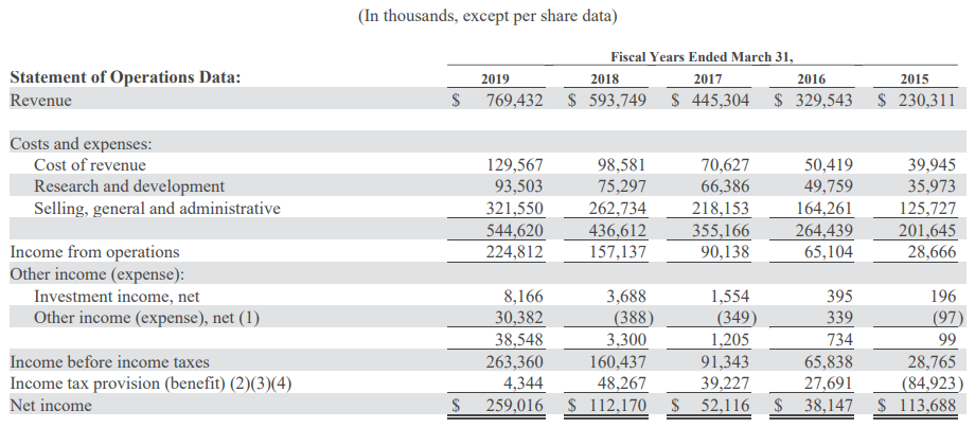

Growth from Impella Devices Led to Margin-expansion: Abiomed, Inc. (NASDAQ: ABMD) is a leading supplier of medical devices that provide circulatory support. The products are designed to enable the heart to rest by improving blood flow and performing the pumping of the heart. The Company’s products are used across the cardiac catheterization lab, or cath lab, by interventional cardiologists and in the heart surgery suite by cardiac surgeons. These are used for the patients who need hemodynamic support prophylactically or emergently before, during or after angioplasty or heart surgery procedures. The company is focusing on higher market penetration of its products like Impella® heart pumps Impella 2.5®, Impella CP®, Impella RP®, Impella LD® and Impella 5.0® devices. The business has received approvals for its marketing of 2.5, Impella 5.0, Impella LD, Impella CP and Impella RP devices from the regulatory bodies like U.S. Food and Drug Administration, CE Mark, Health Canada and from European Union, Canada and from the Japanese Ministry of Health Labour & Welfare (MHLW). Looking at the historical performance over the period of FY15-FY19, the company’s total revenue improved from $230.311 million in FY15 to $769.432 million in FY19, posting a CAGR of 35.2%. Net Income grew from $113.688 million to $259.016 million in FY19, witnessing a robust CAGR growth of 22.9% over the same period.

The business competes with several companies with greater financial, product development, sales and marketing resources. In addition to this, new product development and technological shift differentiate the fields in which the business competes. The company will continue to develop and market new products and technologies to remain competitive within the cardiovascular medical technology market. The company believes that it is well equipped to deal with its competition aided by clinical superiority supported by extensive data, and innovative features that enhance patient benefit, product performance, ease of use and reliability.

5-Year Income Statement Highlights (Source: Company Reports)

Going Forward, the business will focus on creating the new field for heart recovery and developing the standard of care for circulatory support. Despite the challenges with the diffusion of any new break-through invention, the company is taking specific actions to address these issues. Long-term outlook for the company remains intact and the business is collaborating with physician experts to simplify and instruct the community on Impella best practice protocols and the consequences of clinical. The company expects to continue to make additional pre-market approval, or PMA, supplement submissions for the Impella portfolio of devices for additional indications.

Revenue Recognition: Revenue is recognized when the terms of a contract are satisfied, which occurs when control of the promised products or services is transferred to customers. Revenue is calculated as the amount of consideration the company expects to receive in exchange for transferring products or services to a customer. The company recognizes its product revenue when the customer acquires the company’s products, which occurs at a point in time, and during the delivery of the product, based on the customer’s preferences. Recognition of the Service revenue is done when the services are provided to the customer based on the extent of improvement on accomplishment of the performance obligation. The business recognizes service revenue over the term of the service contract. Services are expected to be assigned to the customer throughout the term of the contract while the Company believes recognizing revenue ratably over the term of the contract best represents the transfer of value to the customer. The company also generates revenue from preventative maintenance calls, recognized during the time when the services are provided to the clients.

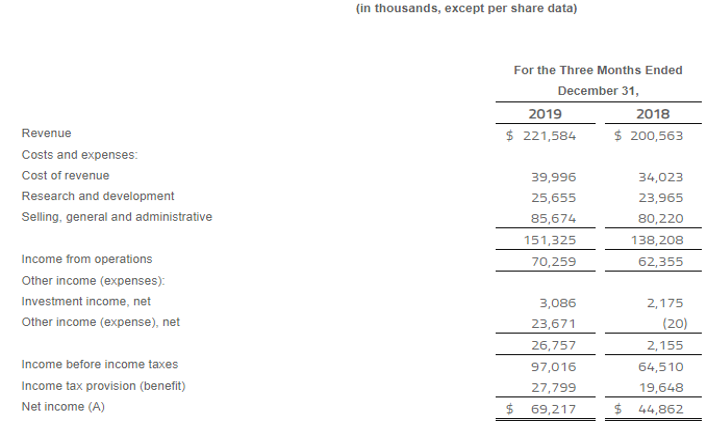

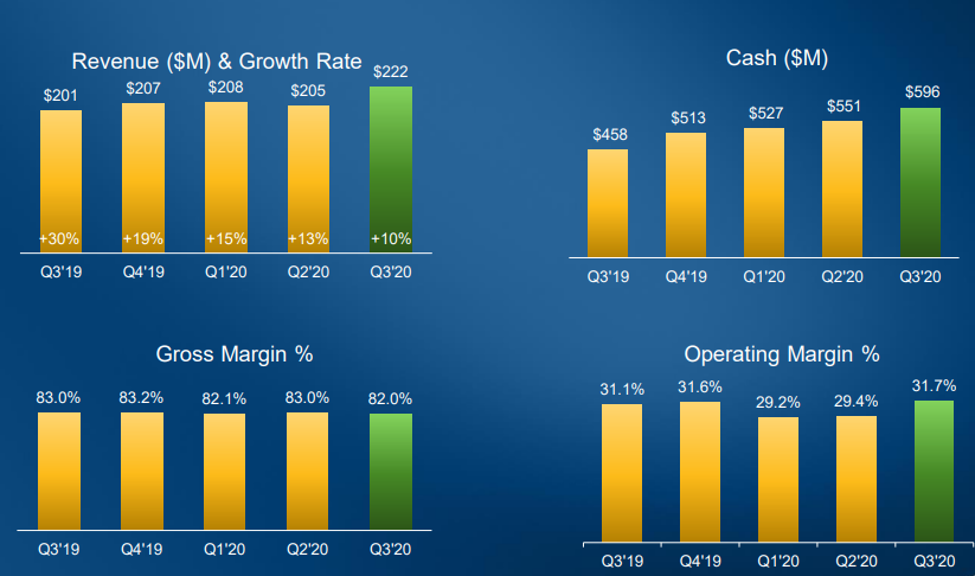

Q3FY20 Business Highlights for the Period ended 31 December 2019: ABMD declared its quarterly results, wherein the company posted its revenue of $221.584 million, up 10% on y-o-y basis. The business witnessed a strong start to the quarter, aided by growth across all geographies, highlighted by 24% global revenue growth and 16% growth in U.S. patient usage during October 2020. U.S. revenue came in at $185.6 million, representing an increase of 8% from the previous corresponding quarter while the business witnessed a 5% pcp growth across the U.S. patient segment. Other than the U.S., the company derived its total revenue at $36.0 million, up 29% from Q3FY19, aided by robust growth in Germany and Japan. Cost of revenue came in at $39.99 million, grew by 18% from the previous corresponding period on account of the increase in the cost of product revenue related to higher demand for the Impella devices and greater production volume and costs to support demand for the Impella devices. Gross margin stood at 82.0%, witnessing a marginal decline from 83.0% in Q3FY19 due to increased investment across direct labor and overhead. Selling, General and Administrative expenses (SG&A) stood at $85.7 million from $80.2 million in Q3FY19. The increase in selling, general and administrative expenses was primarily due to the hiring of additional field sales and clinical personnel in the U.S., Germany and Japan, higher spending on marketing initiatives as the company continues to educate physicians on the benefits to patients of hemodynamic support with the Impella products, and legal expenses related to ongoing patent litigation and other legal matters. Research and development expenses for the three months ended December 31, 2019 increased by $1.7 million, or 7%, to $25.7 million from $24.0 million. The company delivered its net income of $69.2 million as compared to $44.9 million in the previous corresponding period, driven by higher Impella product revenue due to higher utilization of Impella devices and strict expense control by the business.

Q3FY20 Income Statement Highlights (Source: Company Reports)

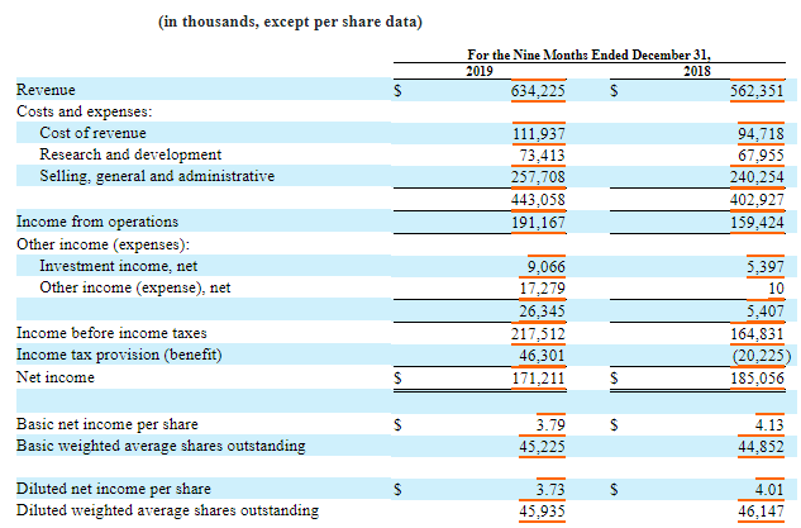

Nine Months Financial Highlights for the Period ended 31 December 2019: The company also mentioned its nine-months performance, wherein it reported a revenue of $634.225 million as compared to $562.351 million on pcp basis. The business witnessed a higher cost of revenue and research & development expenses of $111.937 million and $73.413 million, as compared to $94.718 million and $67.955 million, respectively in the previous corresponding period. The company delivered a net income of $171.211 million, lower from $185.056 million in pcp on account of an income tax benefit of $20.225 million in 9MFY19.

Key Income Statement Highlights for Nine Months ended (Source: Company Highlights)

Key Quarterly Highlights (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 54.01% of the total shareholding. The Vanguard Group, Inc. and PRIMECAP Management Company hold the maximum interests in the company at 10.62% and 6.84%, respectively.

(31).png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Metrics: The Company reported strong numbers in Q3FY20, wherein ABMD posted gross margin at 81.9%, higher than the industry median of 68.1%. EBITDA margin, during the year, stood at 34.1%, improved from 32.9% in Q3FY19. Operating margin during the quarter came in at 31.7%, improved from 31.1% in Q3FY19 and stood higher from the industry median of 9.3%. Net margin at 31.2% in December quarter FY20 stood higher than the industry median of 4.9%. On similar lines, return on equity also stood higher at 6.8%, as compared to just 1.8% of the Industry Median.

Key Metrics (Source: Thomson Reuters)

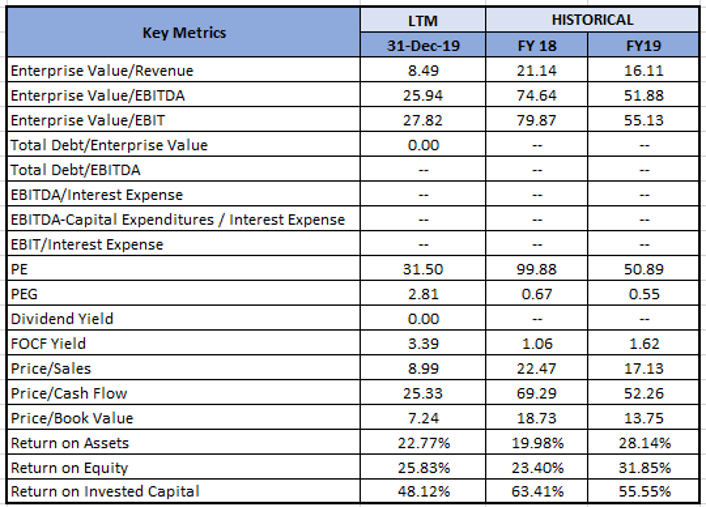

Key Valuation Metrics (Source: Thomson Reuters)

Outlook: The business expects FY20 revenue to be within the range of $846 million to $877 million, depicting a growth of 10% to 14%, respectively. On a GAAP basis, the business expects its FY20 operating margin in the range of 28% to 30%. ABMD will emphasis on investments in field sales and clinical personnel with cath lab expertise to aid recovery awareness for acute heart failure patients and expects higher sales and marketing costs for FY20. The business also strategizes to enhance its marketing, service and training investments across the U.S., particularly for its Impella devices as the business is enhancing its presence across Germany, Japan and other new markets outside of the U.S.

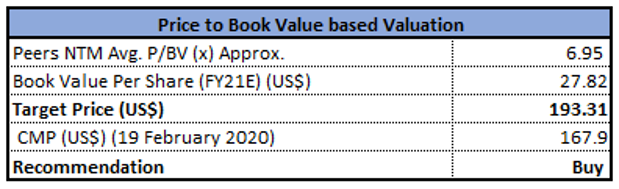

Valuation Methodology: P/BV Based Valuation

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of ABMD closed at $167.90 with a market capitalization of $7.56 billion. The stock made a 52-week low and high of $155.02 and $364.31 and is currently trading at the lower band of its 52-week trading range. The stock has corrected 14.26% and 53.27% in the last six-months and one-year, respectively. The company remains committed to its goal of creating the new field of heart recovery and becoming the standard of care for circulatory support for high-risk PCI and cardiogenic shock. Considering the aforesaid facts, current trading levels, business prospects, etc., we have valued the stock using Price to book based relative valuation method. For this, we have considered peers like Boston Scientific Corp (NASDAQ: BSX), Edwards Lifesciences Corp (NASDAQ: EW), Abbott Laboratories (NYSE: ABT), etc., and arrived at a target price which is offering a lower double-digit upside (in % terms). Hence, we give a ‘Buy’ rating on the stock at the closing price of $167.90, down 0.65% as on 19th February 2020.

ABMD Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Canada Advisory Services Inc. and provided on this website is general information only and it does not take into account your investment objectives, financial situation and the particular needs of any particular person. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. The website www.kalkine.ca is published by Kalkine Canada Advisory Services Inc. The link to our Terms & Conditions has been provided please go through them. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Please wait processing your request...

Please wait processing your request...