Company Overview: Dropbox Inc., is an online company that provides online file storage and sharing services. The Company provides a Dropbox collaboration platform, which enables users to create, access, organize, share, collaborate and secure the content. Its Dropbox paper allow users to co-author content, tag others, assign tasks with due dates, embed and comment on files, tables, checklists and code snippets in real-time. Its Dropbox Smart Sync enables users to access their content on their computers without taking up storage space on their local hard drives. Its Dropbox Showcase enables users to present their work to clients and business partners through a Webpage.

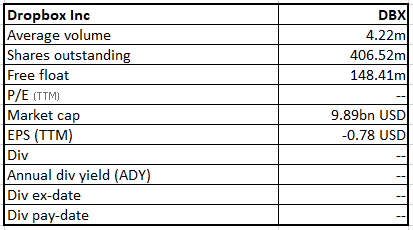

DBX Details

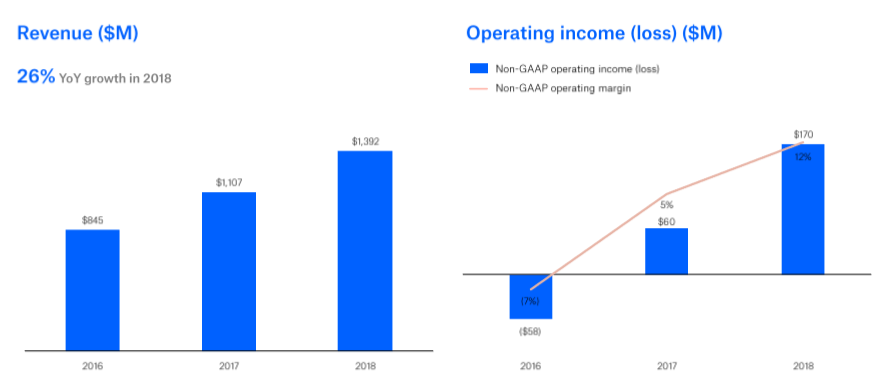

Dropbox Inc. (NASDAQ: DBX), an online company providing file storage and sharing services, has lately reported a good Quarter four result (Q4) that exceeded expectations for most of the fundamental metrics. Despite the adverse FX scenario, the gross margin of the company as per the latest quarterly result has been up to close around 75%, as at December 2018; and this is inching towards the industry median mark of 77.7%. Operating Margin has also demonstrated improvement on year on year basis. The EV/EBITDA mark as at February 28, 2019 is around 24 while the peers seem to be settling around 29. The forward outlook is in a decent zone given the 2019 revenue expected to be above market expectations while operating margin guidance is yet to be watched given growth related investments and other one-time events of 2019. The group’s revenue for FY18 has been $1.4 billion (up 26% year over year) with over 500 million registered users. Healthy growth in business accounts and strategic moves are expected to boost the performance while some short-term challenges might need attention. Primarily, the group expects to benefit from continuous growth in net paying users and growth in average revenue per user (ARPU) with decent EPS improvement and gross margin expansion, and the share price upside looks to be in double digit range in the next 12-24 months.

Ratio Performance (Source: Company Reports and Thomson Reuters)

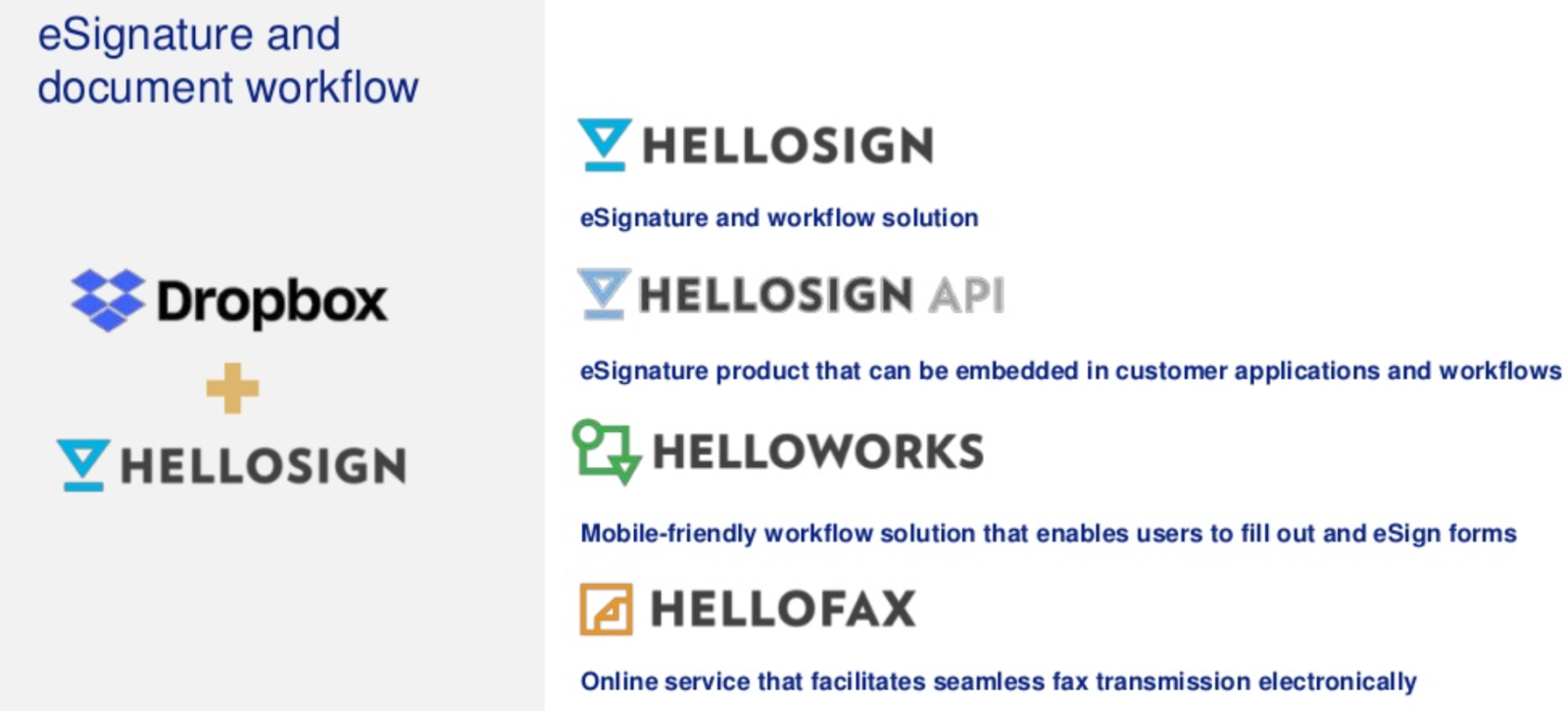

Expedited Document Workflows expected through HelloWorks’ Conditional Logic: Dropbox had recently completed the acquisition of HelloSign, which is a platform meant for an eSignature and document workflow. HelloSign already had more than 80,000 customers. The company had acquired HelloSign for the total consideration of $230 million in cash. HelloSign customizes the document workflow solutions as per the requirement with the help of HelloWorks (product meant for workflow automation) and HelloSign API. Therefore, with the help of the platform the customers can improve everyday processes, can close the deals faster, can easily hire new people onboard, and can complete the documents without errors. Recently, HelloSign has launched the updated version of HelloWorks, that can speed up the workflows three times faster, which means that the revenue will also increase. The rate of completing the forms can increase from 70% up to 96% with this new version. Meanwhile, HelloSign in calendar 2018, had reported for the revenue of approximately $20 million. While HelloSign’s contribution to DBX FY19 revenue might not be material in view of the expected write-downs, the acquisition is expected to add value in the long run.

Acquisition driven value enhancement (Source: Company Reports)

Delivered Better than Expected Results For The Fourth Quarter Of 2018: The company has posted better than expected results for the fourth quarter of FY 18. During the fourth quarter, the net losses narrowed to $9.5 million from the losses of $37 million in the year-ago period. DBX in the fourth quarter of FY 18 has reported the adjusted earnings per share of 10 cents, beating the market estimates for the adjusted earnings per share of 8 cents. The company had reported the adjusted revenue growth of 23 percent to $375.9 million in the fourth quarter of FY 18, beating the market estimates for revenue of $370 million. The company’s revenue grew on the back of the rise in the total paying users and also due to an expansion of ARPU. During the fourth quarter of FY 18, the total number of paying users grew to 12.7 million from 12.3 million at the end of the third quarter of 2018. ARPU during the quarter grew by 5% to $119.56 from $113.39 for the same period last year. The ARPU expansion on a year-over-year basis has been supported by new paying users who have now adopted DBX premium professional and advanced plans; and the group’s strategy to convert value users for sustainable monetization and retention seems to be working well.

Efficiency boosted margins: During the fourth quarter of FY 18, the Non-GAAP gross margin had improved to 75.7% from 70.9% in the same period last year, reflecting an expansion of five percentage points. The company has expanded the gross margin due to the improvement in the unit cost efficiency and the infrastructure hardware, which was partially offset due to the higher expenses related with the employees. Meanwhile, for the fourth quarter, the R&D expense has risen to 29% of revenue to $108 million, compared to 25% in the corresponding quarter a year ago. The rise of R&D expense as a percentage of revenue was on the back of higher headcount and investments in the development and testing of new product. However, S&M expense fell to 25% of revenue to $94 million in the fourth quarter, from 30% in the corresponding quarter a year ago. The decline in this spend is on back of lower marketing expenses compared to the fourth quarter of 2017 as the company started with the global brand campaign. As a result, the company for the fourth quarter has reported the operating profit of $42 million. DBX has posted the Non-GAAP operating margin of 11.0%, as compared to 3.3% in the corresponding period last year, which reflects an expansion of eight-percentage-point from the fourth quarter of 2017. Additionally, the company had ended the fourth quarter of 2018 with cash and short-term investments of approximately 1.1 billion. The company’s cash flow from operations was of $124 million in the fourth quarter 2018. The company during the quarter had incurred the capital expenditures of $35 million, which led to the free cash flow of $88 million or 23% of revenue. The capital expenditure included the spend on the new headquarters of $28 million of. Excluding this expenditure, the company would had posted the free cash flow of $116 million or 30% of revenue. The company has not received any tenant improvement allowance reimbursement for their new headquarters during the fourth quarter 2018. In the fourth quarter 2018, the company also added $26 million to the company’s capital lease funds for data center equipment. Additionally, for FY 18, the company has reported 26% year-over-year growth in the total revenue to $1.392 billion. The gross margin improved by seven percentage points to 75%, from the prior year, and the company’s operating margin also improved by a decent percentage point movement. During the FY 18, net cash from the operating activities increased to $425.4 million from $330.3 million in the prior year. Free cash flow for FY 18 also increased to $362.4 million from $305.0 million in the prior year. The company has incurred the capital expenditures of $63 million during FY 18.

Financial Performance (Source: Company Reports)

Growth Drivers: The company will be able to grow after the conversion of the registered users to the paid users on plans related to individual and team. The company in order to boost growth has to enable the existing paying users to upgrade their current plans to premium ones or they purchase more licenses. Overall, DBX can grow with new product innovations and with expansion of the ecosystem.

.png)

Growth Drivers (Source: Company Reports)

Future Outlook: For the first quarter of FY19, the company expects the revenue to be in the range of $379-382 million. Non-GAAP operating margin for 1Q 2019 is expected to be in the range of 7-8%, and diluted weighted average shares outstanding have been projected to be in the range of $418-423 million. The company projects this based on their trailing 30-day average share price. For the first quarter, the market is expecting the adjusted earnings to be of 10 cents a share on the revenue of $378 million. For the full-year 2019, the company projects the revenue to be in the range of $1.627-1.642 billion. The company also expects that the FY19 gross margin will be more or less in line with the FY18, though it will slightly be lower during the first two quarters of the FY 19. The company is projecting that the HelloSign acquisition will reduce the margins by about 100 basis points. Further, there will be 200 basis point decline in the company’s margins as DBX is moving its offices in San Francisco, for which the company will have to pay rent at both the locations during part of 2019. DBX is now expecting the Non-GAAP operating margin for FY 19 to be in the range of 10.5-11.5% and the free cash flow is projected to be in the range of $375-385 million. Moreover, the company anticipates that the expenses related with investments along with one-time expenditure on the headquarters, to decline in the second half of the FY 19. As a result, the operating margin expansion will resume its growth path by the end of 2019. It is worth noting that during the first quarter of every year, the operating margin is generally on a lower side on the back of higher costs related with employees (manpower) like the reset of payroll taxes etc.

Stock Recommendation: DBX stock is trading at a price of $24.24, and has support at $19.38 level and resistance at $27.4. The company has delivered better than expected performance for both the earnings and revenue for the fourth quarter of 2018. While market has been concerned over the lower operating margin for the first quarter of 2019, the long term potential is decent. With company’s investment plan and strategic moves, the growth narrative is expected to improve based on better and sustainable scenario from 2019 onwards. Accordingly, we give a “Buy” recommendation on DBX at the current price of $24.24.

.png)

DBX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...