Company Overview - Intel Corporation is engaged in designing and manufacturing products and technologies, such as the cloud. The Company's segments are Client Computing Group (CCG), Data Center Group (DCG), Internet of Things Group (IOTG), Non-Volatile Memory Solutions Group (NSG), Intel Security Group (ISecG), Programmable Solutions Group (PSG), All Other and New Technology Group (NTG). It delivers computer, networking and communications platforms to a set of customers, including original equipment manufacturers (OEMs), original design manufacturers (ODMs), cloud and communications service providers, as well as industrial, communications and automotive equipment manufacturers. It offers platforms to integrate various components and technologies, including a microprocessor and chipset, a stand-alone System-on-Chip (SoC), or a multichip package. The CCG operating segment includes platforms that integrates in notebook, two in one systems, desktop computers for consumers and businesses, tablets, and phones.

INTC Details

Inking new associations with key industry players: Intel Corporation (NASDAQ: INTC), the U.S. chipmaker that delivers computer, networking, and communications platforms to a broad set of customers including original equipment manufacturers (OEMs), original design manufacturers (ODMs), cloud and communications service providers, etc., along with Mobileye N.V. and BMW Group has now been joined by global automotive supplier, Delphi Automotive PLC in the stride towards making self-driving vehicles. This is expected to support future OEM customer needs in an appropriate manner. Recently, INTC also won Amazon’s Echo Show Design.

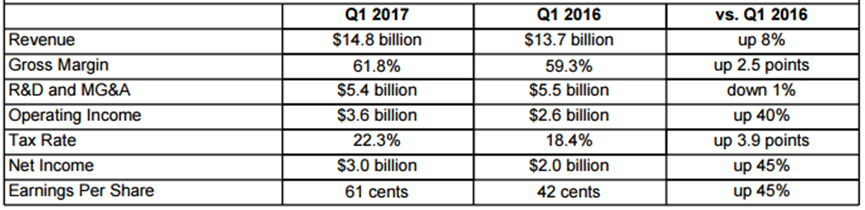

Decent Quarterly Result: INTC reported a revenue growth of 8% year over year to $14.8 billion (Record First-Quarter Revenue), while reporting 40% and 45% year over year growth in operating income and net income at $3.6 billion, $3.0 billion, respectively for Q1FY17. Further, the company generated ~$3.9 billion in cash from operations while paying dividends of $1.2 billion during the same period. The company has repurchased $1.2 billion worth of shares and approved a $10 billion increase to Intel’s share buyback program, which brings the amount currently available for future buybacks to approximately $15 billion. On the balance sheet, company holds $17.3 billion (up $0.2 billion vs Q4FY16), of which $14.2 billion is held by non-U.S. subsidiaries.

Q1FY17 financial summary (Source: Company reports)

On guidance front, for Q2FY17, company is expected to report revenue of ~$14.4 billion and gross margin of ~62%, while the earnings per share are forecasted to be at $0.53. Further, R&D and MG&A spending for Q2FY17 is expected to be around $5.2 billion. For the full year 2017, the group is estimated to post a revenue of $60 billion and gross margin of about 62% driven by performance across the business segments including growth in the memory business. R&D and MG&A spending for the year is expected to be approximately $20.5 billion while the earnings per share for full year is expected to be ~$2.56.

Investing in growing and evolving businesses:In 2016, the company successfully integrated Altera (now Intel’s Programmable Solutions Group) and announced plans to divest Intel Security and establish it as a separate company to increase the focus while participating in the new McAfee’s future success. Notably, the recent data revolution is a big opportunity for Intel and expected to drive virtuous cycle of growth as it provides essential technologies for processing, analyzing, storing, and sharing data. Further, it drives the continuing build-out of the cloud and the transformation of networks, and enables new computing experiences like artificial intelligence, autonomous driving, and merged reality. The major portion of Intel’s 2016 capital investment of $9.6 billion was used to build and equip the most advanced wafer fabrication facilities in the world as they allow the company to optimize performance, cost, and power consumption across the product lines. Currently, Intel is focused on key priorities, such as accelerating growth in the data center while keeping the existing client business healthy and strong; and the launch and ramp of memory technologies and programmable solutions. The company has witnessed progress in directing more resources to growing and emerging businesses in line with the long-term strategy and fewer to mature, less profitable businesses.

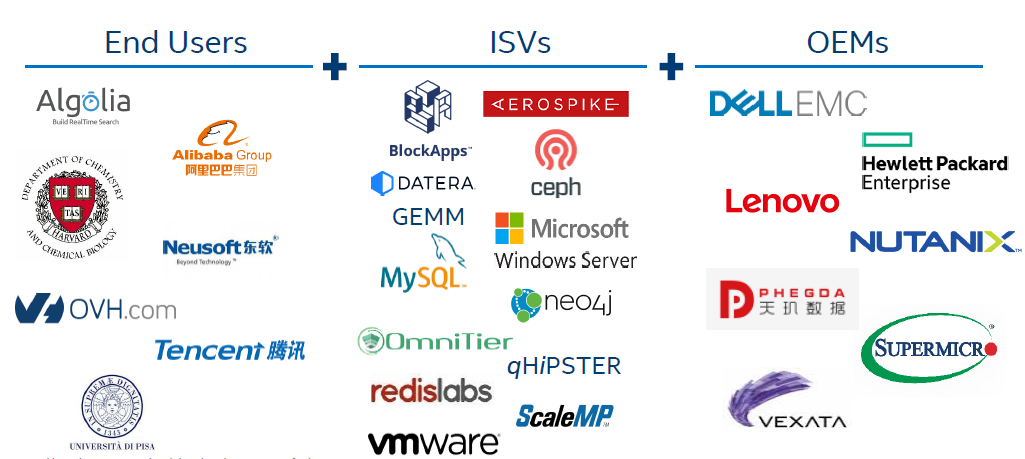

Broad and Growing Ecosystem (Source: Company reports)

Innovative technologies to address the emerging workload demands:In the recent days, individuals are experiencing a dramatic shift in their relationship to technology as things and devices stand even more connected to each other and merging the digital and physical worlds. The company’s new strategy, Virtuous Cycle of Growth leverages Intel’s core assets to power the cloud and drive the increasingly smart and connected world. Further, Intel’s businesses across the cloud and data centers are accelerated by memory and field programmable gate array (FPGA) technologies. Advancements in memory technology and programmable solutions, such as FPGAs (field programmable gate array) make entirely new classes of products for the data centers to meet the increasing need for faster storage and greater memory capacities. Further, this unlocks the value in the cloud as the demand to automate and analyze exponential quantities of data increases. Moreover, FPGAs can efficiently manage the changing workload demands of next-generation data centers and offer the flexibility for users to change their workloads real-time.

Creating a footprint in Autonomous Driving: During the quarter, the company acquired Mobileye, the global leader in computer vision for Advanced Driver Assistance Systems (ADAS) by acquiring all shares of Mobileye. Acquisition combines Mobileye’s best-in-class computer vision with Intel’s computing, data center, and connectivity expertise, and is expected to be immediately EPS accretive. Further, integrated entity is expected to accelerate auto industry innovation by delivering world class E2E solutions at lower cost, faster time-to-market as automated driving market is estimated to reach $70 billion by 2030.

The Opportunity: >$100b total addressable market (Source: Company reports)

Own manufacturing facilities providing a competitive advantage: Silicon manufacturing process technology is a semiconductor device fabrication process used to create the integrated circuits that are present in everyday electrical and electronic devices. Intel has made significant investments (R&D expenditures of $12.7 billion in 2016 vs $12.1 billion in 2015) in research and development into its integrated manufacturing network, which enables it to have more direct control over design, development, and manufacturing processes and quality control. It primarily manufactures products in its own manufacturing facilities, while most of the competitors rely on third-parties and subcontractors for manufacturing and assembly and test needs. Moreover, Own manufacturing enables the company optimize product performance, shorten time-to-market, and scale new products more rapidly. The increased cost of constructing new fabrication facilities to support smaller transistor geometries and larger wafers has led to a reduced number of companies that can build and equip leading-edge manufacturing facilities.

Designing and optimizing products to bring industry leading performance: Intel is designing and optimizing its products to deliver industry leading performance and best in class total cost of ownership for cloud workloads as its shaping the future of the smart and connected world. Importantly, Intel is adding new products and features to its portfolios to address emerging, high growth workloads such as artificial intelligence, media, and 5G. Currently, Intel products utilize 14-nanometer (nm) process technology, which are in the market and it is continuing to work on the development of next-generation 10nm process technology.

Process Technology (Source: Company reports)

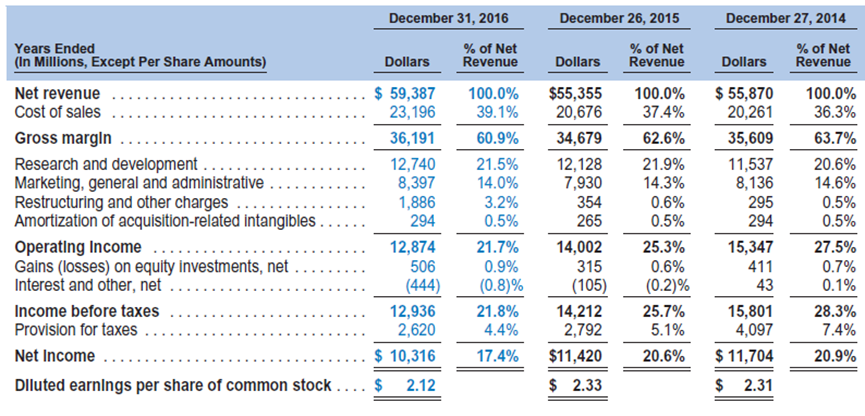

FY16 Financials: During FY16, Intel reported a revenue growth of 7% yoy to $59.4 billion led by Data Center Group, continuing demand from cloud services, ramp-up of new adjacent products, and big gains in networking service. Importantly, despite a decline in the PC market, the Client Computing Group’s revenue and profitability was led by a robust segmentation strategy and a mix of Intel Core processors. Gross margin revenue grew by $1.5 billion to $36.2 billion during the same period. However, the gross margin declined by 1.7% to 60.9% primarily driven by Altera integration and other amortization of acquisition-related charges, higher factory start-up costs and higher product warranty and intellectual property charges.

Financial Summary (Source: Company reports)

The company generated cash flow of $22 billion from operations in FY16 against the average of $20 billion over the past five years. Return on equity stood at 16% compared to average of 19% in the last five years. In addition to the acquisition of Altera, Intel completed 11 other acquisitions in 2016 for total consideration of $15.5 billion, consistent with the number of transactions and levels of investment in 2015 and 2014. In 2016, Intel returned about $7.5 billion to shareholders, paid $4.9 billion in dividends and repurchased $2.6 billion in stock. Notably, over the last five years, Intel has returned a cumulative total of $54.4 billion to stockholders in dividends and stock repurchases.

Stock performance:INTC stock moved over 17.2% in the last twelve months (as of May 17, 2017), however, it has slipped 1.2% in last one month with some concerns on risks prevailing in the sector and Q1FY17 results related to operating margins. Given the company’s progress in modern technologies and significant investments to address the increasing demand from clients, we believe that the Intel is well positioned to sustain the growth and generate value through earnings. Strengthened relationships with key industry players is an added advantage. Risks around security in chipsets, competition from other players etc. prevail, but the exciting product lines and other developments do call in for a consideration. For instance, the group is also signaling about the launch of its next-generation server processor family (Skylake-SP) for improved performance, power efficiency, and platform features. INTC might also get a boost from memory products such as Optane that can act as a future sales catalyst. The stock has been down over 2% as at May 17, 2017 and is holding its annual stockholders meeting on May 18, 2017. We give a “Buy” recommendation on the stock at the current price of $ 35.04

INTC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...