CA

CA  AU

AU UK

UK US

US NZ

NZWhat do you mean by Fully Amortising Payment?

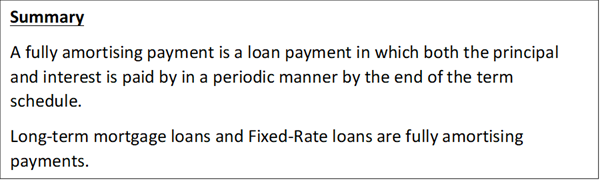

A fully amortising payment alludes to a kind of periodic repayment on an obligation. When a borrower makes installments per the amortisation schedule, the debt is completely paid off before its set term finishes. If the loan is a fixed-rate advance, each fully amortising installment is an equivalent dollar sum. If the credit is an adjustable-rate advance, the completely amortizing installment changes as the financing cost on the advance changes.

An amortised loan is a kind of credit with predetermined periodic installments applied to both the principal amount and the interest due. The amortised advance installment first takes care of the pertinent interest cost for the period, after which the rest of the installment is put toward lessening the principal sum. Average amortised loans incorporate automobile credits, home advances, and individual advances from a bank for little tasks or obligation unions.

Copyright © 2021 Kalkine Media

Understanding Fully Amortising Payment

Credits for which completely amortizing installments are made are known as self-amortsing loans. Home loans are common self-amortizing credits and are mostly fully amortising installments.

An example of an utterly amortising installment, a man requires a 30-year fixed-rate contract with a 4.5% financing cost, and his regularly scheduled installments are $1,266.71. Toward the start of the loan, most of these installments are dedicated to the interest component and simply a small part to the principal; close to the furthest limit of the advance's term, most of every installment covers principal, and just a little bit is designated to interest part. Since these installments are thoroughly amortizing, if the borrower makes them every month, he takes care of the credit before its term.

Copyright © 2021 Kalkine Media

There are contrasts between how amortisation chips away at fixed and flexible rate contracts. On a fixed-rate contract, your home loan installment remains something similar for the duration of the existence of the advance, with just the blend between the measures of principal and interest changing every month. The solitary way your installment changes on a fixed-rate advance is if you have a difference in your duties or mortgage holder's protection. With a flexible rate mortgage, principal and interest sums change toward the finish of the credit's time frame. Each time the principal and interest change, the distinction is re-amortised to be paid off toward the finish of the term.

On a customisable rate contract, you have entirely amortising installments, although the loan cost can go up or down toward the finish of the time frame. The teaser period is the way long your financing cost stays fixed toward the start of the advance. This period is commonly 5, 7, or 10 years. At the point when you're contrasting customisable rate contracts, understand what you're seeing when looking at rates. If you see a 5/1 flexible rate with 2/2/5 covers, that implies that the underlying rate will remain fixed for five years and change once each year after that. The covers are how much the installment can increment. For this situation, the installment could go up 2% on the first adjustment and 2% on subsequent adjustments. In any case, for no situation can the installment go up by over 5% over the whole lifetime of the advance. The only thing restricting how much an installment can go down is the edge on the credit, which will be specified in your home loan documentation. This isn't generally the situation, but, usually, flexible rate loans have up to 30 years or more. The installment re-amortises over the rest of the advance, so your balance will be zero toward the end of the term.

Frequently Asked Questions

What are the differences between Fully Amortising Payment and Interest-only Payments?

An interest-only installment is something contrary to a completely amortising installment. If our borrower is covering the interest on every installment, he isn't on the timetable to take care of the credit before the finish of its term. When the lender permits the borrower to make beginning installments that are not precisely the completely amortising installment, the completely amortising installments later in the existence of the credit are fundamentally higher.

To represent, envision somebody takes out a $250,000 contract with a 30-year term and a 4.5% loan cost. In any case, instead of being fixed, the financing cost is movable, and the moneylender guarantees the 4.5% rate for the initial five years of the advance. After that point, it changes naturally.

If the borrower were making completely amortising installments, he would pay $1,266.71, as demonstrated in the principal model, and that sum would increment or reduce when the credit's interest charge changes. In any case, if the credit is organised, so the borrower pays interest installments for the initial five years, his regularly scheduled installments are just $937.50 during that time. However, they are not entirely amortising. Subsequently, after the starting loan fee terminates, his installments may increment up to $1,949.04. By taking non-completely amortising installments e, the borrower focuses on making bigger completely amortising installments later in the credit's term.

In an alternate kind of interest-only loan, only the interest component is repaid for specific years. Towards the end of that period, there's an inflatable installment where all or a segment of the equilibrium is expected. If only half of the total loan is remaining paid, the rest of the credit installments are typically completely amortised for however much time stays on the term.

Please wait processing your request...

Please wait processing your request...