Company Overview: DXC Technology Company provides digital information technology (IT) services and solutions. The Company provides a range of services, including analytics, applications, business process, cloud and workload, consulting, enterprise and cloud applications, security, and workplace and mobility. The Company offers a portfolio of analytics services, to provide insights and accelerate users’ digital transformation. Its analytics services and solutions include Data Discovery Experience, Data Workload Optimization and Managed Business Intelligence Services. The Company addresses analytic solution needs to run the business, including customer analytic services, warranty analytics, predictive maintenance analytics, social intelligence analytics, healthcare analytics, insurance analytics, data pipeline and operations, banking analytics, airline analytics and operational analytics. The Company also offers e-commerce, finance and administration products and services.

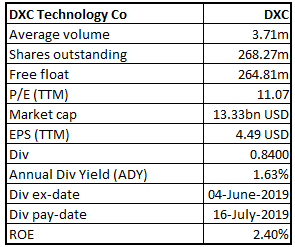

DXC Details (ROE* figure for 4Q FY19)

An Advanced Digital Workplace Services' Provider, DXC Technology Co (NYSE: DXC) has been formed post separation of Hewlett Packard Enterprise's Enterprise Service segment and from the merger with Computer Sciences Corporation and Electronic Data Systems. The company mainly operates in regions like North America, Europe, Asia, and Australia. The company recently announced a mixed set of numbers for 4QFY19 with an increase in the dividend. As per the most recent outcome from NelsonHall Evaluation & Assessment Tool (NEAT), the company has been positioned as a Leader in Advanced Digital Workplace Services-Overall market segment. Additionally, the company was named as a leader for Build Services Focus and Run Services Focus. The company has enjoyed a large client base across multiple industry verticals such as travel and transportation, retail, public sector, energy, banking, healthcare, insurance, etc.

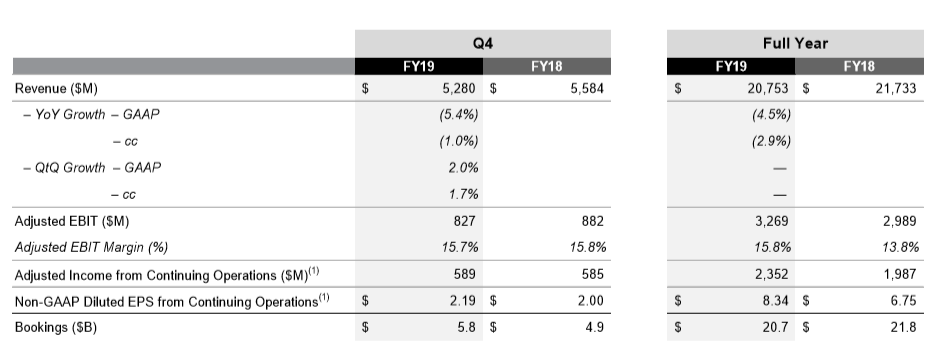

Mixed Results for 4Q FY19 with an Improvement in Bookings & Revenue on a Sequential Basis: The company witnessed mixed performance for the fourth quarter of FY 19. Net income for the company came in at $271 million in 4Q FY19 as compared to $560 million posted in the prior corresponding period. The net income for the quarter included the restructuring costs of $(35) million, $66 million loss due to transaction, separation and integration-related costs, $101 million loss on back of amortization of acquired intangibles, and pension and OPEB actuarial, and settlement losses of $116 million. Excluding these adjustments, the company recorded the Non-GAAP net income of $589 million for the 4Q. The company reported a 1% decline yoy (year-on-year) in the revenue to $5.28 billion in 4Q FY19, however, improved sequentially and grew by 1.7%. For the fourth quarter of 2019, the company posted a y-o-y growth of 18.9% in the Bookings and an improvement of 2.5% on a sequential basis. Adjusted EBIT at $827 million in the fourth quarter of 2019 was slightly lower as compared to $882 million reported in the prior corresponding period. As a result, for the quarter, the adjusted EBIT margin was mildly down to 15.7% as compared with 15.8% in the year ago quarter and declined 50 basis points on a sequential basis. Fall in the margin was due to the strategic investments in digital assets and capabilities which included the major hiring of the employees. The ongoing savings which DXC is currently offering to its clients to underpin their digital transformations, also led to some pressure to the margin. However, the company posted 200 basis points of improvement in the adjusted EBIT margin to 15.8% for FY19 on the back of the ongoing execution against the key cost-saving measures. DXC, in the quarter, reported the adjusted earnings per share of $2.19. The company generated the adjusted free cash flow of $917 million in the 4Q FY19, representing 155% of the adjusted net profit. This was driven by controlled management of working capital. Adjusted free cash flow for FY19 stood at $2.1 billion, showing ~90% of adjusted net profit. During the fourth quarter, net cash provided by operating activities was improved to $748 million as compared to $557 million in the year ago period. Additionally, the company incurred the capital expenditure of $316 million during the quarter, which was ~6% of revenue. For the full year of FY19, capital expenditure came in at $1.15 billion, which was ~5.5% of revenue. DXC generated the cash of $2.9 billion at the end of Q4 and FY 19.

Fourth Quarter of FY19 Financial Highlights (Source: Company Reports)

Segment Performance During the Fourth Quarter of 2019: Profit margin for Global Business Services (GBS) segment at 20.4% for 4Q FY19 was improved by 100 bps on y-o-y basis and by 220 basis points on a sequential basis. This improvement was on the back of optimization of ongoing workforce and the seasonality in the business. Profit margin for Global Infrastructure Services (GIS) segment for 4Q FY19 declined by 50 basis points and 340 basis points on y-o-y and sequential basis, respectively, which was due to the investments undertaken by the company. GBS revenue declined 3.1% (y-o-y) in 4Q FY19 in constant currency but was up 0.9% on a sequential basis to $2.2 billion. However, GBS bookings in the quarter witnessed an improvement of 40% yoy and grew 27% on a sequential basis. In the fourth quarter, GIS revenue grew 0.6% y-o-y in constant currency basis whereas on a sequential basis, it grew 2.3% to $3.09 billion. This growth was primarily on the back of strong progress seen in the Mobility business, Workplace, etc. GIS bookings improved by 3.7% year-on-year to $2.97 billion. Digital revenue grew year-over-year, reflecting clients’ accelerating shift to Digital.

The company posted strong Digital bookings, and its book-to-bill stood at 1.8x in the quarter due to strong bookings witnessed by cloud infrastructure and digital workplace. The digital revenue for FY19 grew by 15.8%. The strong demand was experienced in digital capabilities, as both the digital bookings and pipeline, grew by more than 50% year-over-year.

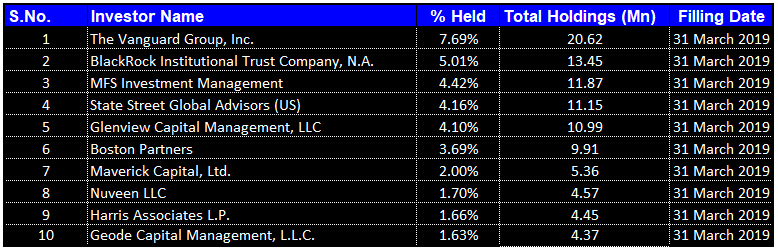

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 36.06% of the total shareholding. The Vanguard Group, Inc and BlackRock Institutional Trust Company, N.A. hold maximum interest in the company at 7.69% and 5.01%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Mergers & Acquisition: DXC is acquiring Luxoft for about $2 billion as part of strategic investment in digital capabilities, and the acquisition is expected to be closed by the end of June. With the Luxoft acquisition, the company will also expand the access to digital talent, as Luxoft has highly skilled digital employees of more than 13,000, in which 80% have a master’s degree or Ph.D. DXC is expanding its digital workforce and has employed more than 1,000 digital people. Further, the company plans to re-skill about two thousand of its employees in digital technologies. Meanwhile, from Luxoft acquisition, DXC is projecting the incremental revenue in the range of $200 million to $400 million from the combined company by the fiscal year 2022. DXC will use Luxoft's strong presence in key markets such as Eastern Europe, for attracting digital talent and enhance its presence across North America, Europe, and the Asia Pacific region through the digital strategy consulting and engineering capabilities. Moreover, as part of the ongoing investments in digital assets and capabilities, DXC has recently announced its intention to acquire the services division of EG A/S, a leading company that integrates Microsoft Dynamics 365 in Northern Europe. However, the company has not disclosed the terms of the deal. Additionally, DXC plans to acquire a data centre situated in New Jersey from Credit Suisse through its subsidiary. DXC has entered into a managed colocation services agreement for 13-plus years with the US division of Credit Suisse. With this, the company will be able to capitalize on the existing infrastructure assets to provide the service to enterprise clients, and it will be close to the New York metropolitan market.

Capital Management: DXC raised its dividend to 21 cents per share. The company will pay the dividend on 16 July 2019 to its shareholders who are on record at the close of business on 06 June 2019. During the fourth quarter of FY19, DXC returned $142 million to shareholders. This was comprised of dividends paid to the shareholders of $51 million and share repurchases done by the company of $91 million. During FY19, DXC has given back $1.55 billion of capital to its stockholders. This was comprised of dividend amount to $210 million and share repurchases of ~$1.34 billion.

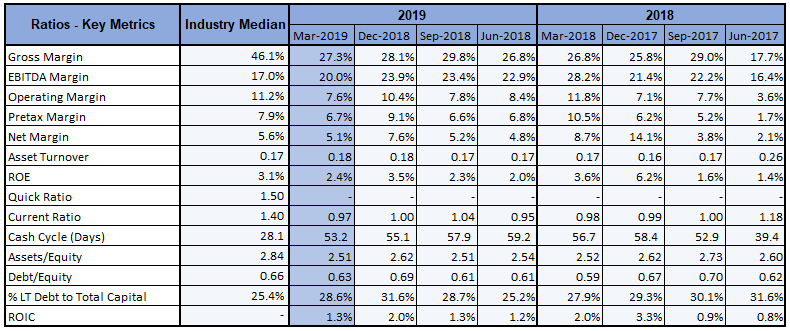

Key Metrics: The company has enjoyed a healthy gross margin at 27.3% in 4Q FY19. EBITDA margin stood at 20.0% in 4Q FY19, which is above the industry median of 17.0%. Net margin and ROE came in at 5.1% and 2.4%, reflecting a decent position, although below the industry median of 5.6% and 3.1%, respectively.

Key Metrics (Source: Thomson Reuters)

Future Outlook: DXC expects the topline to be in the range of $20.7 billion to $21.2 billion for FY20. This target includes the effect of the acquisition of Luxoft which is expected to be closed at the end of June. The company expects the non-GAAP earnings per share to be in the range of $7.75 to $8.50. Adjusted free cash flow is projected to be 90% or more of the adjusted net income.

FY 20 Targets (Source: Company Reports)

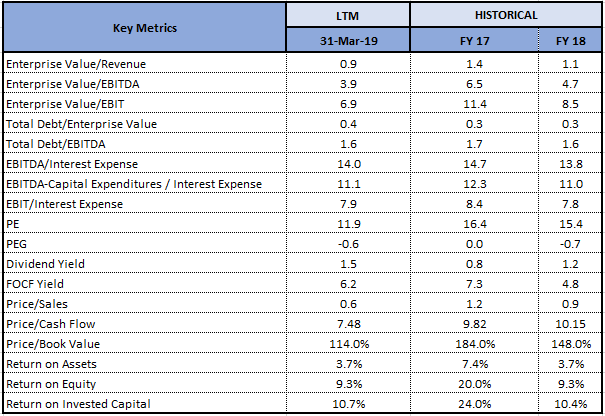

Key Valuation Metrics (Source: Thomson Reuters)

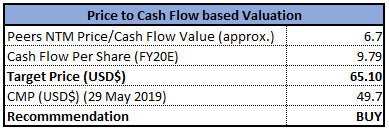

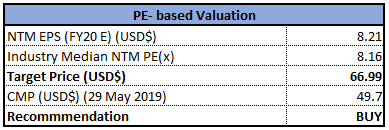

Valuation Methodology: Below tables highlight exemplary methods of deducting upside potential of the stock.

Method 1: Price to Cash Flow Multiple Approach (NTM):

Price/Cash Flow Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2: Price to Earnings Multiple Approach (NTM):

Price/Earnings Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: At the closing price of $49.7, the stock is trading at reasonable PE multiple of 11.07x with the market capitalization of circa $13.33 Bn as of 29 May 2019. Furthermore, the company is continuously investing in digital assets and capabilities including the accelerated hiring efforts. DXC expects the acquisition of Luxoft to be completed by the end of June 2019. Meanwhile, the company witnessed a sequential improvement in bookings & revenue during the fourth quarter. Overall, DXC posted mixed results for the fourth quarter of 2019 due to ongoing investments in digital capabilities and due to various adjustments done in the net profit. Considering aforesaid parameters and favorable outlook in the business, we have valued the stock using two Relative valuation methods, Price-to-cashflow and PE multiple and have arrived at target price upside in the range of double-digit (in %)). Hence, we give a “Buy” recommendation on the stock at the current market price of $49.7 per share (down ~3.33% on 29 May 2019).

.png)

DXC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...