Company Overview - Bank of America Corporation is a bank holding company and a financial holding company. The Company is a financial institution, serving individual consumers and others with a range of banking, investing, asset management and other financial and risk management products and services. The Company, through its banking and various non-bank subsidiaries, throughout the United States and in international markets, provides a range of banking and non-bank financial services and products through four business segments: Consumer Banking, which comprises Deposits and Consumer Lending; Global Wealth & Investment Management, which consists of two primary businesses: Merrill Lynch Global Wealth Management and U.S. Trust, Bank of America Private Wealth Management; Global Banking, which provides a range of lending-related products and services; Global Markets, which offers sales and trading services, and All Other, which consists of equity investments, residual expense allocations and other.

BAC Details

Integrated business model focused on growth and sustainable returns: Bank of America Corp (NYSE: BAC) has a sustainable business model with 47 million consumers and small business relationships with 31 million retail customers and 11 million preferred customers. The customer portfolio includes one million high net worth of households. BAC's global market comprises 8,000 clients with 35 trading locations and 640 research analysts. With this integrated model of consumer banking, global wealth and investments, global banking and global markets, the bank has shown significant earnings improvement. The bank has held US #1 position in Retail Deposits, Home Equity lender and #2 position for retail Mortgage Origination volume. Bank’s Global Research is holding #1 position for 6th consecutive year. BAC has shown a remarkable increase in mobile banking active users which grew from 19.6 million in Q1FY16 to 22.2 million in Q1FY17.

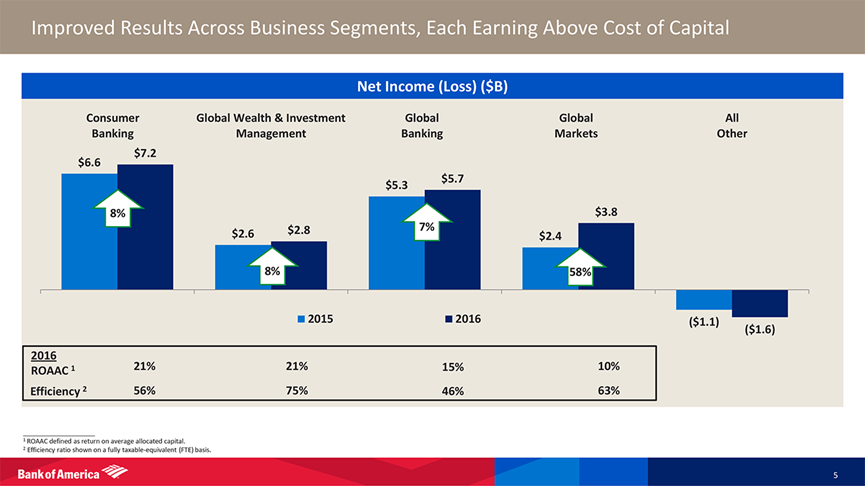

Better performance across business segments (Source: Company reports)

Buyback to remain in focus: In the period of 2008-2013, Bank of America has raised capital and financed the acquisition of Merrill Lynch. 2013 was the inflection point and from there onwards the bank has stopped issuing capital and started buying back stock. It spent a net of $2.8 billion in 2013 on share repurchase and recently $4 billion in 2016. CEO commented in latest annual letter that “now that our company is stronger we are focused on reducing the dilution and increasing the dividend.” Meanwhile, Warren Buffet has invested $5 billion of Berkshire Hathaway capital in Bank of America preferred stock. The deal warrants to purchase 700 million shares of the bank’s common stock any time before mid-2021.

Buyback history (Source: Company presentation)

Decent first quarter of FY17 performance: Bank of America delivered net income of $4.9B (up 40% from 1Q16) and earnings per diluted common share of $0.41, up 46% from 1Q16 while revenue growth was up 7%. BAC exceeded market expectation for the net interest income and fee income and showcased bank’s strong operating leverage. The bank reported combined revenues for global banking and markets of $9.5 billion, surpassing street’s $9.1 billion forecast and ahead of its $2.7 billion forecast. Investment banking revenues of $1.6 billion were reflecting its strength in debt capital markets, equity capital markets and merger and acquisition fees. The average total loans and leases were at $914 billion in Q1FY17 compared with $893 billion in Q1FY16. The average deposit grew to $1,257 billion from $1,198 billion. The bank declared regular quarterly cash dividend of $0.75 per share and regular quarterly dividend of $1.75 per share on the 7% cumulative Redeemable preferred stock.

Consumer banking segment performance highlights:This segment reported a rise of 7% in Net income to $1.9B during the first quarter of 2017 as compared to their prior corresponding period. Return on average allocated capital (ROAAC) was at 21% while the segment’s Pretax, pre-provision net revenue rose 17% to $3.9B. The segment’s revenue rose 5% year on year (yoy) to $8.3B while NII improved on the back of solid deposit growth. However, the non-interest income declined slightly, impacted by mortgage banking income pressure and no divestiture gains recorded in 1Q16. Provision also enhanced against the prior corresponding period while net reserve rose $66 million in 1Q17 as compared to net release of $208 million in prior corresponding period (pcp). Net charge-offs surged $33 million boosted by better credit card balances. Non-interest expense fell 3% on yoy basis as the operating efficiencies paid off despite higher FDIC and litigation expense. The Efficiency ratio enhanced to 58% as compared to 53%. The Average deposits improved 10% yoy to $636B from pcp. The segment also witnessed 50% of deposits in checking accounts and 89% primary accounts. Average cost of deposits declined 10 bps to 1.63%. The Average loans and leases increased $20B, or 8%, to $258B against pcp. Overall mortgage production fell $0.9B to $15.5B against pcp. Client brokerage assets surged $27B, or 21%, boosted by solid client flows and market performance while new accounts rose 11%. Overall debit and credit spending surged 5% yoy during the period. Mobile banking active users surged 13% to 22.2 million during the quarter. Further, one out of every five deposit transactions were found to be completed via mobile devices.

Built a strong client base:The bank has built 47 million Consumers and Small Business relationships. The consumer banking business built 31 million Retail customers with less than $50k house hold income. The segment has 11 million preferred customers with greater than $75K HHI / >$100K in assets. The segment also has 3 million Small Business customers, 22.2 million mobile customers and 34.5 million active digital users. As per Global Wealth & Investment Management business, the bank has built over 1 million high net worth households with more than $250K in assets (ML) and greater than $3 million in assets (UST). The bank has over $2.6 trillion client assets in this segment with $152 billion loans and leases, and $255 billion deposits. For Global Commercial Banking, the bank has over 15K clients with U.S middle market clients and international subsidiaries.

Digital Trends (Source: Company reports)

Investments for future benefits: The bank has invested ~$3 billion annually on technology initiatives. For the consumer segment, the bank intends to invest in new digital capabilities like Real-time P2P payments (Zelle), Free FICO scores and even launched Spanish mobile app. The bank also launched artificial intelligence functionality while more than 8,500+ cardless-enabled ATMs were launched in first quarter of 2016. The bank deployed 3,500+ digital ambassadors in financial centers. They are focusing on interactive voice response (IVR) capabilities to improve client experience. With regards to the Wealth Management, the bank made a multi-year investment in Merrill Lynch One (fee based advisory platform) and launched Merrill Edge Guided Investing – online investing + professional portfolio management. The bank also invested in Practice Management & Development (PMD) program (new advisor training) while improved their wealth advisors by over 700 from 2014. For Banking and Markets segment, the bank invested more than $1B in GTS over last four years to boost functionality and their core treasury business. The bank also enhanced local coverage in Global Commercial Banking and Business Banking while improved percentage of clients served by a local market coverage officer rose from 59% to 90%. The bank also made a centralized wholesale credit function to drive efficiencies and migrating to new trading platform with better functionality.

Expectation of stronger economy: A stronger economy would boost Bank of America with better spending, borrowing and financing. However, it would also impact rates. Although the Federal Reserve chose not to raise rates at the back of Q1 weak GDP report and bleak March job report, the higher rate of interest is expected to benefit the bank (a rate hike could have added $150 million in net interest income in the second quarter). Further its ongoing expense initiative is continuing to manage the operating costs. It is also noteworthy that BAC has shown much more robust recovery after the financial crises as compared to other big banks.

Stock performance:The shares of BAC surged over 28.7% in the last six months (as of May 10, 2017) and have enjoyed a stellar run last year. The bank sees a seasonal drop in expenses in the second quarter compared with the first, with more revenues and benefits from other sources which would add to the bottom line. Bank of America is updating 1,500 of its branches across the country and 53 in New England in next two years to mimic the Federal Street branch. This would help improve the services and increase bank’s income. Any improvements in the economic conditions are expected to boost the stock performance in the long-term. We give a “Buy” recommendation on the stock at the current price of $ 24.15

BAC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...