Company Overview: Levi Strauss & Co. is an apparel company. The Company designs, markets and sells its products under the Levi's, Dockers, Signature by Levi Strauss & Co. and Denizen brands directly or through third parties and licensees. Its products include jeans, casual and dress pants, tops, shorts, skirts, jackets, footwear, and related accessories for men, women and children across the world. The Company's trademarks include Arcuate Stitching Design, the Tab Device, 501, the Two Horse Design, the Housemark and the Wings and Anchor Design. The Company operates in three geographic segments: the Americas, Europe and Asia. The Company's products are sold in more than 110 countries. The Company licenses its Levi's and Dockers trademarks for a range of product categories in markets in each of its regions, including footwear, belts, wallets and bags, outerwear, sweaters, dress shirts, kidswear, sleepwear and hosiery.

.png)

LEVI Details

Value-Added Products Boosted Profitability: Levi Strauss & Co. (NYSE: LEVI) is one of the leading branded apparel companies and is a global leader in the jeans segment. The company designs and distributes jeans, casual wear and related accessories for men, women, and children under the Levi's®, Dockers®, Signature by Levi Strauss & Co.™, and Denizen® brands. The products of the company are available across 110 countries through a combination of chain retailers, department stores, online sites, and a global footprint of approximately 3,000 retail stores and shop-in-shops. Based on distribution channels, the company categorizes its revenue into two segments, namely wholesale and direct-to-consumer (DTC). LEVI recognizes wholesale revenue channelized through third-party retailers such as department stores, specialty retailers, leading third-party e-commerce sites and franchise locations dedicated to brands. The direct-to-consumers includes products which are sold through a variety of formats, including company-operated mainline and outlet stores, company-operated e-commerce sites and select shop-in-shops located in department stores and other third-party retail locations.

In FY18 (for the period ended on November 2018), total net revenue stood at $5,575.44 million, posting a growth of 13.7% as compared to $4,904.03 million during FY17. Net profit for the company was recorded at $283.142 million, grew 0.6% on y-o-y. Looking at the past performance, LEVI delivered a CAGR growth of ~4.1% in revenue over the period of FY14 to FY18, while net profit posted a CAGR growth of ~27.8% over the same period.

Going forward, LEVI is looking for strategic choices, which include diversifying the business by “expanding for more” into categories where the company is underpenetrated and have outsized growth opportunities. The Company is broadening its product categories beyond men’s bottoms as women’s, which has grown consecutively since FY15, and currently accounts for nearly one-third of the total revenue. LEVI’s tops business, which continues to grow with double digits, has more than doubled over the last three fiscal years (FY16-FY18).

.png)

Five-Year Income Statement (Source: Company Reports)

3QFY19 Financial Highlights For the period ended August 2019: LEVI declared its third-quarter results for financial year FY19 wherein, the company reported revenue of $1,447.08 million as compared to $1,394.15 million in Q3FY18. The company reported net income at $124.51 million as compared to $130.124 million, with a net profit margin of 8.6% in Q3FY19.

.png)

Q3FY19 Income Statement (Source: Company Reports)

LEVI reported net revenue at $1447.1 million, grew by 5.2% on pcp terms on a constant currency basis, excluding $19 million in unfavorable currency effects. The company's direct-to-consumer business grew by 12% on a constant currency basis during the third quarter, driven by expansion and improved performance of the retail network and e-commerce. Net revenue from the company's wholesale business grew by 1% on a reported basis and 2% on a constant currency basis, aided by growth across Europe and Asia.

.png)

Q3FY19 Net Revenue (Source: Company Reports)

LEVI’s gross profit came in at $767 million during Q3FY19, up 5.2% y-o-y on constant currency. Gross margin stood at 53% of net revenue, compared with 53.2% in Q3FY18, driven by the growth in direct-to-consumer and international segment, followed by price increases of several products, which was partially offset by unfavorable currency effects of 60 basis points and investment in the product.

Selling, general and administrative (SG&A) expenses for the third quarter came in at $596 million on a reported basis, compared with $582 million in the previous corresponding quarter. SG&A as a percentage of net revenue stood at 41.16% as compared to 41.76% during the third quarter of FY18. The improvement of 60 basis points was despite higher investments in direct-to-consumer expansion, technology, and distribution capacity, which was offset by leverage on base costs and lower incentive compensation expense. SG&A includes a reduced impact from the previously-cash-settled stock-based compensation awards.

Operating income for the third quarter came in at $171 million, up 8% from the prior corresponding year on a reported basis. The business witnessed higher net revenue in Europe and Asia, which were partially offset by higher SG&A expenses associated with the expansion of the company-operated retail network.

Adjusted EBIT, during the quarter, came in at $176.4 million, up 3.6% y-o-y on constant currency, aided by revenue growth. Adjusted EBIT margin at 12.2% witnessed a mild downtick as compared to 12.4% on the previous corresponding year on account of adverse currency effect on gross margin.

.png)

Q3FY19 Adjusted EBIT and Adjusted EBIT Margin (Source: Company Reports)

Segment-Wise Analysis:

The business has three reporting segments: Americas, Europe, and Asia (which includes the Middle East and Africa).

Americas: The Americas segment reported Q3FY19 net revenue at $770.8 million on a constant currency, reporting a 2.8% decline on y-o-y basis due to a decline in the wholesale business. However, revenue was partially offset by the growth seen in the direct-to-consumer business. Net revenue from direct-to-consumer grew by 9%, driven by growth across Levi’s brands across the region. The decline in the wholesale primarily reflected a Dockers® line reset during the second half of 2018, reduced shipments to the off-price channel in 2019, and the impact in 2019 of a pending acquisition of a South American distributor. This region witnessed a y-o-y decline of 7% in the operating income on both reported and constant currency due to the lower net revenue and a lower operating margin. The business witnessed higher SG&A investments in retail and distribution, which was offset by a higher gross margin from direct-to-consumer growth. This segment derived nearly 53.28% of the total group’s revenue.

Europe: In Europe, net revenue came in at $463 million as compared to $406 million in the previous corresponding period, registering a yoy growth of 14% on a reported basis and 18% on a constant currency basis. This segment contributed ~32% of the company’s sales, reflecting continued broad-based growth in both direct-to-consumer and wholesale channels across the region. Operating income from Europe grew 34% (y-o-y) on a reported basis and 39% (y-o-y) on a constant currency basis, reflecting the net revenue growth and a higher gross margin from direct-to-consumer growth, partially offset by higher selling costs.

Asia: In the Asia segment, net revenue increased by 9% (y-o-y) on a constant currency to $213 million, reflecting decent performance across traditional wholesale and direct-to-consumer channels across the region. Revenue growth was broad-based across most of the markets. Asia’s operating income grew by 25% y-o-y on a constant-currency basis, reflecting higher net revenue, partially offset by higher SG&A to support retail expansion. The business derived 14.72% of the total revenue to the group’s income.

.png)

Segment-wise Revenue (Source: Company Reports)

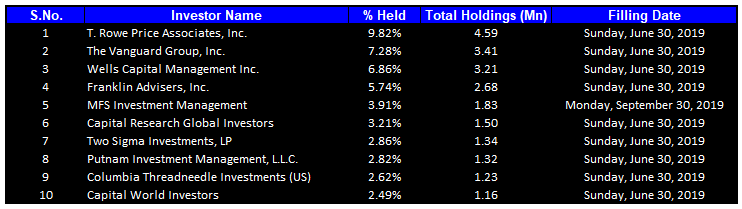

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 47.61% of the total shareholding. T. Rowe Price Associates, Inc. and The Vanguard Group, Inc. hold the maximum interests in the company at 9.82% and 7.28%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

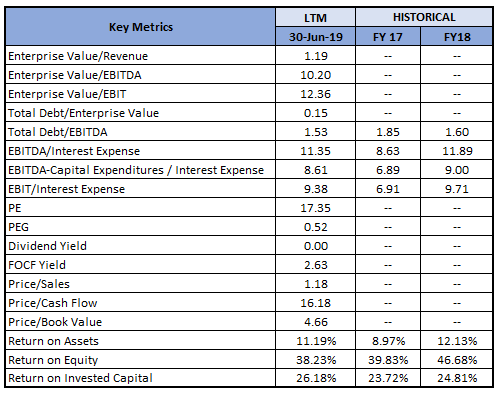

Key Metrics: The Company posted decent margins during the third quarter of FY19. Gross margin for Q3FY19 stood at 53%, slightly higher than the industry median of 52.2%. Operating and net margin for Q3FY19 came in at 11.8% and 8.6%, higher than the industry median of 11.5% and 7.6%, respectively. Return on Equity (ROE) during the quarter stood at 9.0% in Q3FY19, higher than the industry median of 4.2%.

Key Metrics (Source: Thomson Reuters)

Latest Update:

Recently, LEVI announced that it has entered into an asset purchase agreement to acquire all operating assets related to the Levi’s® and Dockers® brands from The Jeans Company (“TJC”), LS&Co.’s distributor in Chile, Peru and Bolivia, for the value of ~ $35 million, plus transaction costs.? This includes approximately 80 Levi’s® and Dockers® retail stores, distribution with the region’s leading multi-brand retailers, and the logistical operations in these markets. This acquisition is likely to be closed by the first quarter of 2020.

Key Ratios (Source: Thomson Reuters)

Outlook: As per the Management guidance, the company expects net revenue for FY19 to grow at 5.5% to 6% for FY19, including the impact of the South American distributor acquisition announced in August. The company expects gross margin to remain flat as compared to the previous year. The business expects capital expenditure within $190 million to $200 million to be utilized for opening 100 new stores during FY19. Adjusted EBIT margin is expected to come in flat on corresponding prior year on a reported basis; and the business expects adjusted EBIT to witness a margin expansion in the range of 10 basis points, excluding currency effects from translation. Full-year weighted-average diluted share count is expected to be within the range of 410-415 million shares.

Valuation Methodologies

Method 1: Enterprise Value to Sales Multiple Approach:

EV/Sales Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

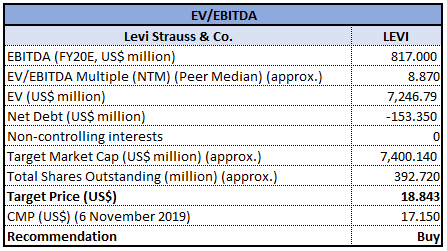

Method 2: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 3: Price to Earnings Multiple Approach:

.png)

PE Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: At the market close, the stock of LEVI ended at $17.15 with a price to earnings multiple of 17.35x and market capitalization of ~$6.735 billion. LEVI will continue to drive diversification through high-growth, high-margin businesses while protecting and growing its profitable core. The company’s strategic choices have continued to pay off, followed by values-driven leadership continuing to differentiate the company in a crowded marketplace. Considering the aforesaid facts, we have valued the stock, using three relative valuation methods, i.e., Price to Earnings Multiple, Enterprise Value to Sales Multiple, and Enterprise Value to EBITDA Multiple, and arrived at a target price of higher single-digit to lower double-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the closing price of $17.15, down 1.15% on 06 November 2019.

LEVI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...