Company Overview: Wells Fargo & Company is a bank holding company. The Company is a diversified financial services company. It has three operating segments: Community Banking, Wholesale Banking, and Wealth and Investment Management. The Company offers its services under three categories: personal, small business and commercial. It provides retail, commercial and corporate banking services through banking locations and offices, the Internet and other distribution channels to individuals, businesses and institutions in all 50 states, the District of Columbia and in other countries. It provides other financial services through its subsidiaries engaged in various businesses, including wholesale banking, mortgage banking, consumer finance, equipment leasing, agricultural finance, commercial finance, securities brokerage and investment banking, computer and data processing services, investment advisory services, mortgage-backed securities servicing and venture capital investment.

.png)

WFC Details

Efforts to revamp brand reputation: Wells Fargo (NYSE: WFC) is initiating a marketing campaign called "Re-Established" to revamp the trust among stakeholders. Wells Fargo has been facing allegations from several months regarding the opening of the unauthorized new accounts. The initial component of the campaign is a one-minute commercial called "Trust" that airs nationwide; ads would run across print, digital, broadcast, and mobile channels. For the first quarter of 2018, Management tried to meet customers’ financial needs and also made progress on rebuilding trust with their customers, team members, communities, regulators, and shareholders. They focused to enhance their compliance and operational risk management programs, investing in innovative products and services. The group finished surveying 387,000 branch customer experience surveys as of first quarter 2018, with ‘Loyalty’ scores reaching their highest levels since August 2016, while ‘Overall Satisfaction with Most Recent Visit’ scores continued to improve as compared to the earlier quarter. Debit card point-of-sale purchase volume rose 8% year on year (yoy) to $81.8 billion as of first quarter of 2018 while Credit card point-of-sale purchase volume rose 8% yoy to $17.4 billion. The group reported 28.8 million digital (online and mobile) active customers, including 21.8 million mobile active users.

Controlling non-performing assets: During the first quarter of 2018, the group’s nonperforming assets fell $388 million, or 4%, from December 31, 2017, which is the eighth consecutive quarter of decreases. Better consumer and commercial portfolios coupled with lower foreclosed assets drove this item. Moreover, nonperforming assets comprised 0.88% of total loans, which is the lowest level since the merger with Wachovia in 2008. Nonaccrual loans also fell $317 million against the earlier quarter on the back of a fall in commercial nonaccruals. Moreover, foreclosed assets fell $71 million against the prior quarter. The group was also able to maintain a decent credit result loss given their focus to build high quality loans. Net charge-offs were $741 million, or 0.32% (annualized) of average loans, against $805 million a year ago (0.34%). This fall in net charge-offs in first quarter 2018, was on the back of fall in losses in the commercial and industrial loan portfolio, including in the oil and gas portfolio. During the quarter, commercial portfolio net charge-offs were $78 million, or 6 basis points of average commercial loans, against net charge-offs of $143 million, or 11 basis points, a year ago. However, net consumer credit losses rose to 60 basis points (annualized) of average consumer loans against 59 basis points (annualized) in pcp.

.png)

Fall in non-performing assets (Source: Company reports)

Better than expected first quarter performance: Investors were expecting a weaker performance from Wells Fargo for the first quarter given their reputation and ongoing regulation and compliance pressure. But the group managed to deliver an overall better than expected performance. Preliminary earnings of $5.9 billion were initially reported with an indication of a need to be revised to reflect additional accruals for the CFPB/OCC matter. Lately, net income fell to $5.1 billion (or diluted earnings per common share of $0.96) during the quarter against $5.6 billion (or diluted earnings per common share of $1.03) in pcp. Despite the $414 million fall in their provision for credit losses, a $86 million fall in net interest income, a $235 million fall in noninterest income, and a $1.3 billion rise in noninterest expense drove the performance. Income tax rate was lower during the quarter, leading to the net interest income representing 56% of the revenue, against 55% for the same period a year ago. Noninterest income was $9.7 billion in first quarter 2018, representing 44% of revenue, against the $9.9 billion (45%) in first quarter 2017. The group incurred a $800 million discrete litigation accrual in connection with entering into the consent orders with the CFPB and OCC on April 20, 2018. Revenue fell $321 million to $21.9 billion against pcp while net interest income fell 1% and noninterest income fell 2% from a year ago. Average loans fell $12.6 billion, or 1%, to $951.0 billion, against pcp. Total deposits fell $21.8 billion, or 2% to $1.3 trillion against pcp. Return on assets (ROA) fell to 1.09% from 1.18% in pcp while return on equity (ROE) declined to 10.58% against 11.96% in pcp. Nonaccrual loans fell $2.0 billion, or 21%. Despite the overall performance pressure, the group returned $4.0 billion to shareholders via common stock dividends and net share repurchases, and thus the quarter was the 11th consecutive quarter of returning more than $3 billion.

Mixed segmental performance: Community Banking segment reported for net income fall of 22% to $2.7 billion, during the first quarter of 2018 against fourth quarter 2017 but revenue rose 1% to $11.8 billion, against fourth quarter 2017, boosted by sales of Pick-a-Pay loans and higher market sensitive revenue. Wholesale banking net income rose 21% yoy to $2.9 billion, against fourth quarter of 2017 boosted by a decline in income tax rate. The segment’s revenue fell 2% to $7.3 billion against the earlier quarter, on the back of decrease in net interest income, lower commercial real estate brokerage fees, lower insurance income related to the sale of Wells Fargo Insurance Services USA (WFIS). On the other hand, Wealth and Investment Management net income rose 6% to $714 million, against fourth quarter 2017 but revenue fell 2% to $4.2 billion against earlier quarter, on the back of fall in gains on deferred compensation plan investments (offset in employee benefits expense), lower net interest income, and lower transaction revenue, partially offset by higher asset-based fees. Retail Brokerage segment’s client assets rose 4% yoy to $1.6 trillion, while Advisory assets surged 10% yoy to $540 billion, boosted by higher market valuations and positive net flows Wealth Management. Total assets under management rose 3% yoy to $497 billion, boosted by better market valuations, positive money market and fixed income net flows, while IRA assets rose 5% yoy to $403 billion. Institutional Retirement plan assets rose 7% to $386 billion against pcp.

Capital position requirement: Wells Fargo Common Equity Tier 1 ratio was higher than the regulatory minimum and their internal target of 10%. Common Equity Tier 1 ratio (fully phased-in) reached 12.0% as of the March quarter indicating their lower risk weighted assets. The Capital generation from earnings was more than offset by about (20) bps of OCI leading to higher interest rates and over (35) bps capital return. Net payout ratio was 85%. The group expects their eligible external TLAC (Total Loss Absorbing Capacity) as a % of total risk-weighted assets of 24.0% against the expected 2019 required minimum of 22.0%.

Aiming to control expenses: The group expects their total expenses for FY18 to be in the range of $53.5 - $54.5 billion which comprises over $0.6 billion of typical operating losses, and excludes litigation and remediation accruals and penalties. They forecast their efficiency initiatives to cut expenses by $2 billion annually by year-end 2018 while those savings would support their investment in the business. The group forecasts a further $2 billion in annual expense reductions by the end of 2019. These savings are expected to go to the “bottom line” and be fully recognized in 2020.

.png)

Fall in Noninterest expense (Source: Company reports)

Focusing on credit card lending: Consumer loans fell $2.6 billion as compared to the last quarter as growth in nonconforming first mortgage loans was more than offset by fall in auto and legacy consumer real estate portfolios including Pick-a-Pay and junior lien mortgage loans due to run-off, sales and credit discipline. First mortgage loans fell $1.4 billion as compared to the last quarter but rose $8.0 billion on a YoY basis. Accordingly, Wells Fargo is making efforts to resume U.S. non-customers with mailing credit-card offers later this year.

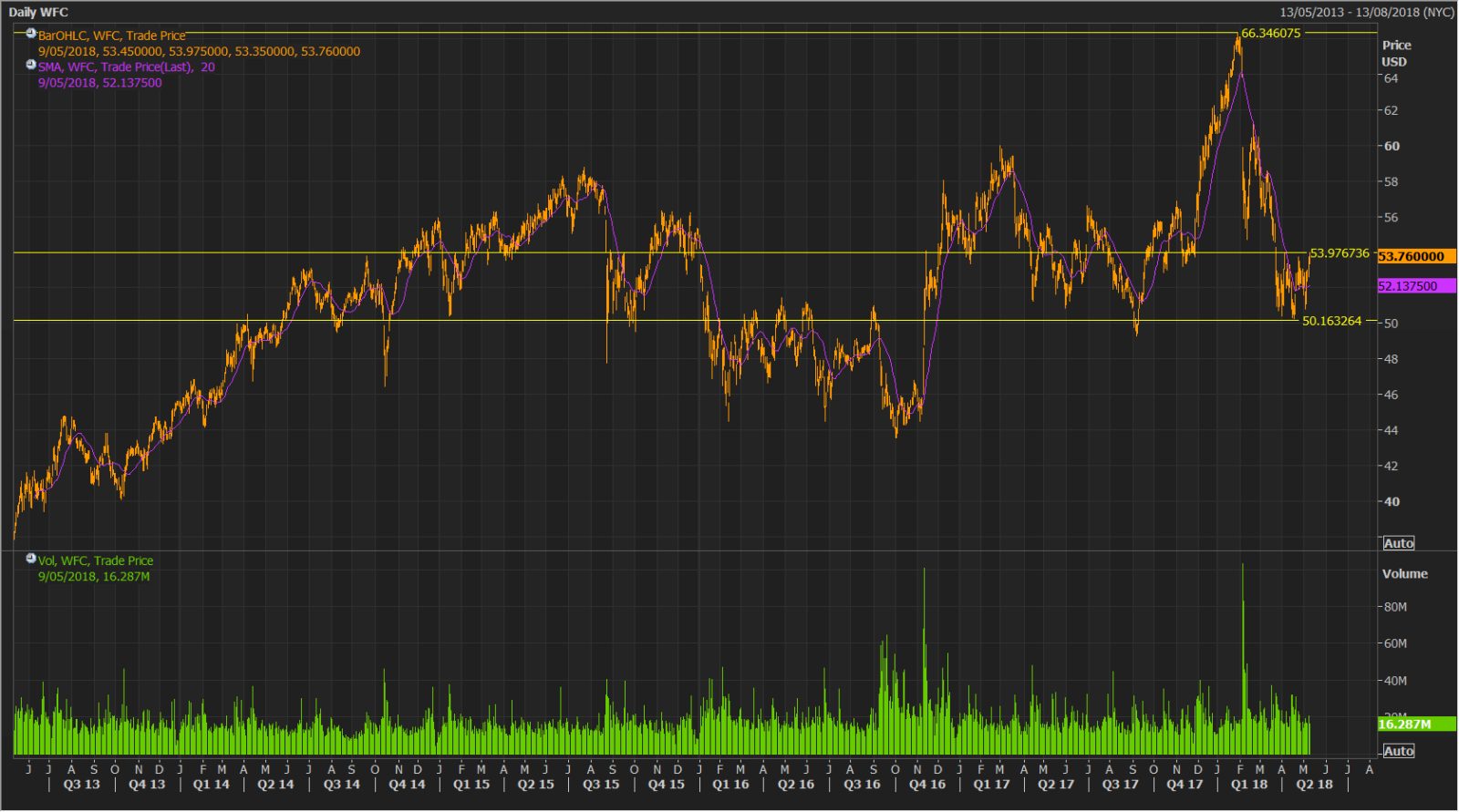

Stock performance: Wells Fargo’s assets fell $36.4 billion as of the first quarter of 2018 as compared to the earlier quarter. Over $32 billon fall in commercial deposits from financial institutions, including ~$15 billion of actions taken to comply with the Consent Order asset cap hurt the performance. On the other hand, the earnings impact from managing within the asset cap was relatively modest during the first quarter of 2018 on the back of the minimal actions taken during the quarter. The group sees this impact to rise in subsequent quarters, while expects net income after tax impact to be within their earlier guidance of $300- 400 million range for 2018. WFC stock already corrected over 12% in this year to date placing the stock at a reasonable level. We believe WFC’s efforts to build back its brand reputation coupled with efficiency initiatives would boost its performance in the coming periods. While the last few years have been challenging for WFC with the group in the process of paying back customers under a $142 million settlement related to millions of unauthorized accounts, the near term catalysts look favorable with low expense guidance expected to be touched upon during the investor day, and any positives from Comprehensive Capital Analysis and Review (CCAR) in June. Given the emerging valuation scenario, we rate a “Buy” on this dividend yield stock at the current price of $ 53.76 (up 1.1% on May 09, 2018), ahead of its investor day revelations scheduled for May 10, 2018.

WFC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...