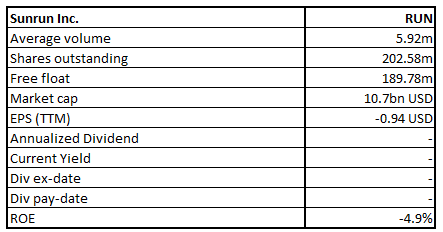

Sunrun Inc.

RUN Details

Sunrun Inc. (NASDAQ: RUN) is engaged in the design, development, installation, sale, ownership and maintenance of residential solar energy systems in the United States. It has over 550,000 customers and it has sold its solar service in 22 states, DC & Puerto Rico. The company has a market capitalization of ~US$10.7 billion as on 25th March 2021.

Result Performance – For the Year Ended 31 December 2020

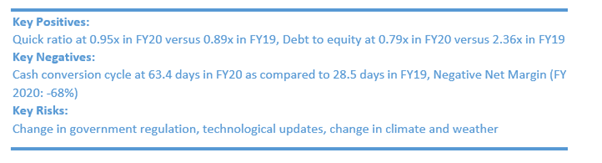

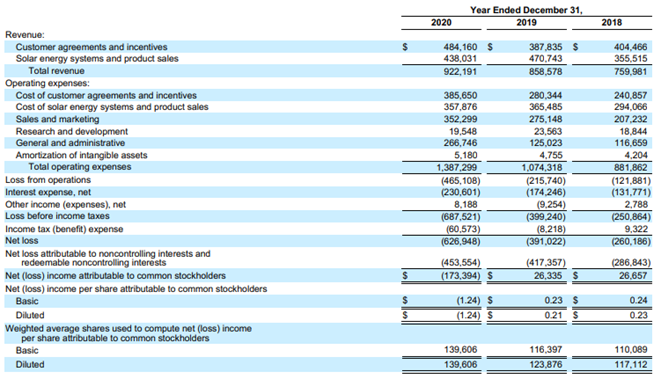

For the year ended 31 December 2020, the revenue increased by 7% to $922.2 million from $858.6 million in the corresponding period last year. The rise in revenue was mainly led by rise in customer agreements which grew by 25% to $432.5 million from $345.5 million in FY19. However, incentives grew by 22% to $51.6 million from $42.3 million in FY19. However, the solar energy systems fell by 5% in FY20 to $269.9 million from $283.4 million.

The company’s net loss grew to $626.9 million from $391.0 million in FY19.

Key Data (Source: Company Reports)

Recent Updates

On 26 January 2021, the company announced the pricing of $350 million aggregate principal amount of 0% convertible senior notes due 2026 in a private placement to qualified institutional buyers.

As per the release dated 23 February 2021, SolarEdge Technologies, Inc. has entered into a strategic supply agreement with Sunrun. As part of the agreement, Sunrun would be offering SolarEdge’s next generation PV inverter, Energy Hub, for the residential customers.

On 25 February 2021, the company announced its Q4FY20 and full year results. As per the release, it has added approximately 23,500 customers in Q4FY20. Further, its announced net subscriber value of $9,051 resulting in total value generated of $170 million during Q4FY20.

As per the release on 10 March 2021, the company has priced a securitization of leases and power purchase agreements. The securitization consists of a single-tranche of A- rated notes with a $201 million initial balance, representing an 80.0% advance rate.

Outlook:

On 8 October 2020, the company announced that it has completed the acquisition of Vivint Solar. With this transaction, the company establishes its position as the leader in home solar and energy services across the United States and a top owner of solar assets globally with over three gigawatts of solar energy and more than 500,000 customers.

Now, the company is better placed in the industry to provide affordable, reliable and clean electricity at new scale. As per the management, residential solar market is massive & underpenetrated.

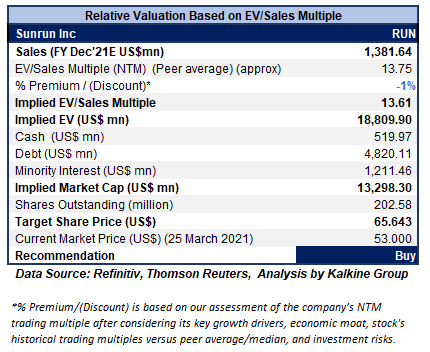

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Stock Recommendation:

With the acquisition and ambition to fill the existing gap in the residential solar market, the company has cemented its footstep for future growth. The combination of direct-to-consumer, solar partnerships and strategic partnerships offers fundamental advantages to the company. The stock has witnessed a fall of ~22.8% in 3 months and over the last 6 months, it has fallen by ~12.6%. However, the stock reported a triple digit growth of ~166.6% in 9 months and ~335.8% in 1 year. The stock has a 52-week low and high of US$8.75 and US$100.93, respectively and is currently trading below the average of 52-week high-low range.

Considering the aforesaid facts, we have valued the stock using an EV/Sales multiple-based illustrative relative valuation and have arrived at a target price which reflects a rise of low double-digit (in % terms). We believe the company can trade at a slight discount to its peer EV/Sales (NTM Trading multiple) considering the company has negative EBITDA margin and net profit margins versus peers, while also considering its elevated debt levels.

The first resistance has been marked at US$84.80 and first support has been marked at US$49.02.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of US$53.00 per share, down ~4.07% on 25th March 2021.

RUN Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

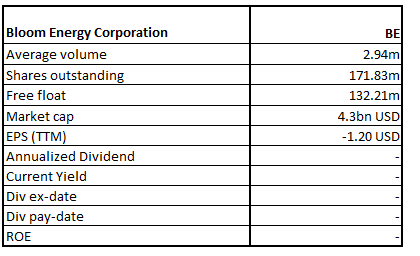

Bloom Energy Corporation

BE Details

Bloom Energy Corporation (NYSE: BE) designs, manufactures, sells as well as, in certain cases, installs solid-oxide fuel cell systems for the on-site power generation. The company has a market capitalization of ~US$4.3 billion as on 25th March 2021.

Result Performance – For the Year Ended 31 December 2020

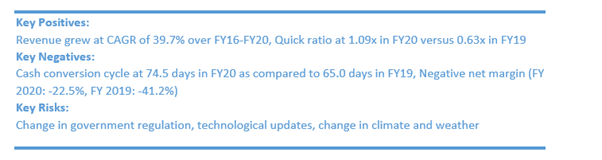

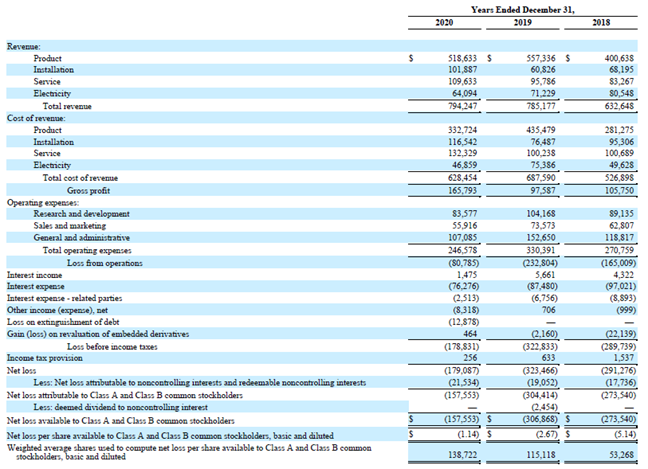

For the year ended 31 December 2020, the revenue increased by 1.2% to $794.2 million versus $785.2 million in 2019, primarily led by 11.1% increase in acceptances, offset by the favorable impact of the PPA II upgrade that occurred in the year ended December 31, 2019.

The company reported 1,326 acceptances, or 132.6 MW. The company had a cash position, including restricted cash, as of 31 December 2020 was at $416.7 million, compared to $504.4 million as of September 30, 2020.

Key Data (Source: Company Reports)

Recent Update

On 2 February 2021, the company announced that coalition of 11 companies have partnered to form Hydrogen Forward, an initiative focused on advancing hydrogen development in the United States.

Outlook:

The company’s management team as well as employees proved resilient in executing the business plan, delivering robust financial performance, solid operating results as well as significantly improving the balance sheet. For FY 2021, the company’s expects revenue between $950 million - $1 billion and non-GAAP gross margin to be ~25%. However, non-GAAP operating margin is expected to be ~3%.

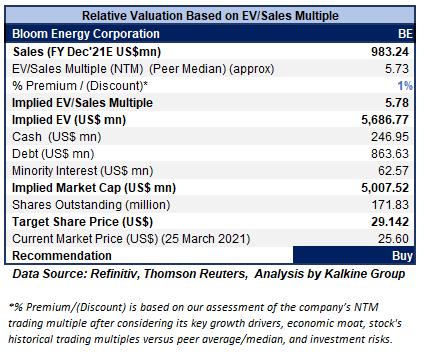

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Stock Recommendation:

The company has a strong business plan of delivering healthy financial performance amid significant improvement in the balance sheet. It is well positioned to meet future growth driven by technology road map and ability to build application energy servers that solve critical energy problems like resiliency, reducing carbon emissions and costs.

The stock has witnessed a fall of ~9.5% in 1 month and over the last 3 months, it has fallen by ~16.1%. However, the stock reported a triple digit growth of ~202.6% in 9 months and ~380.3% in 1 year. The stock has a 52-week low and high of US$4.43 and US$44.95, respectively and is currently trading close to the average 52-week high and low range.

Considering the aforesaid facts, we have valued the stock using an EV/Sales multiple-based illustrative relative valuation and have arrived at a target price which reflects a rise of low double-digit (in % terms). We believe that the stock might trade at a slight premium as compared to its peer median EV/Sales (NTM Trading multiple) given the commitment in clean energy with a focus in hydrogen and deployment of Carbon Capture, Utilization and Storage technology in 2021. The company is investing in fuel cells and electrolysers to transform into hydrogen platform with potential capacity of 1GW by 2025.

The first resistance has been marked at US$42.15 and first support has been marked at US$22.72.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of US$25.60 per share, up ~4.66% on 25th March 2021.

BE Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

The advice given by Kalkine Canada Advisory Services Inc. and provided on this website is general information only and it does not take into account your investment objectives, financial situation and the particular needs of any particular person. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. The website www.kalkine.ca is published by Kalkine Canada Advisory Services Inc. The link to our Terms & Conditions has been provided please go through them. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Please wait processing your request...

Please wait processing your request...