Kamada Limited

Kamada Ltd (NASDAQ: KMDA) is Israel based company, focused on plasma-derived protein therapeutics with a commercial product portfolio and a late-stage product pipeline. The Company uses its proprietary platform technology and know-how for the extraction and purification of proteins from human plasma to produce Alpha-1 Antitrypsin (AAT) in a highly purified, liquid form, as well as other plasma-derived Immune globulins.

Key Business and Financial Updates:

- Strong Operational Momentum and Strategic Focus: Kamada reported robust performance for the third quarter and first nine months of 2025, supported by continued execution of its growth strategy and diversification across its specialty plasma-derived product portfolio. Management emphasized sustained profitability expansion, disciplined cost management, and positive commercial trends across key markets, which together underpin confidence in achieving full-year revenue guidance of USD 178–182 million and adjusted EBITDA of USD 40–44 million. The Company continues to prioritize long-term double-digit profitable growth, supported by investments in business development initiatives and clinical advancement programs.

- Financial Performance Highlights: Third-quarter revenue increased 13% year over year to USD 47.0 million, while adjusted EBITDA grew 34% to USD 11.7 million, driven by improved sales mix and increased demand for products such as GLASSIA®, VARIZIG®, and offerings in the Distribution segment. Gross margin expanded to 42%, reflecting higher commercial scale and favorable portfolio contributions, while operating expenses remained consistent with prior-year levels. Net income rose 37% to USD 5.3 million, and operating cash flow totaled USD 10.4 million. For the first nine months of 2025, revenue reached USD 135.8 million, up 11% year over year, with adjusted EBITDA rising 35% to USD 34.2 million and net income increasing 56% to USD 16.6 million. Cash generation remained positive at USD 17.9 million despite higher working-capital requirements.

- Advancement of Clinical and Post-Marketing Programs: Kamada continued progressing key clinical and post-marketing initiatives, including the launch of the SHIELD study for CYTOGAM®, designed to evaluate its efficacy in mitigating late-onset CMV infections in high-risk kidney transplant recipients. This research forms part of a broader post-marketing program aimed at generating real-world evidence to further support CYTOGAM’s therapeutic value. The Company also advanced its pivotal Phase 3 InnovAATe clinical trial for inhaled AAT therapy, with an interim futility analysis planned for completion by year-end.

- Expansion of Plasma Collection Capabilities: The Company continued strengthening its plasma collection infrastructure, highlighted by recent FDA approval of the Houston plasma collection center under its existing Biologics License Application. This facility, capable of handling 50 donor beds and producing approximately 50,000 liters annually, is positioned to become one of the largest specialty plasma centers in the United States. Kamada is also preparing to seek EMA approval for the site, while ramping up collections at its three operational centers and engaging potential customers for long-term supply agreements.

- Balance Sheet Position and Outlook: As of September 30, 2025, Kamada held USD 72.0 million in cash and cash equivalents, reflecting strong operating inflows offset by investment spending and the payment of a USD 11.5 million special dividend. The Company remains well-capitalized to support ongoing portfolio expansion, clinical development, and business development opportunities. Kamada reiterated its fiscal 2025 financial guidance, projecting continued double-digit top- and bottom-line growth, supported by scale expansion, diversified revenue streams, and a steady pipeline of clinical and commercial initiatives.

Technical Observation (on the daily chart):

- Price Structure and Moving Averages: KMDA has traded within a broad sideways range between USD 5.50 and USD 9.00 for most of the year, following a retracement after its early-2025 rally. The price is now slightly above both the 21-day and 50-day moving averages, and the recent crossover of the 21-day above the 50-day suggests early, modest improvement in short-term trend conditions.

- Momentum Indicators and RSI Behavior: The RSI is currently near 57, indicating neutral to mildly positive momentum. It has shifted between stronger readings during earlier rallies and more subdued levels during mid-year consolidation, with the latest uptick reflecting a gradual strengthening in buying interest without entering overbought territory.

- Volume Patterns and Participation: Volume has been relatively modest throughout the year, with occasional spikes during earlier rallies but quieter levels during the prolonged consolidation. Recent slight increases in volume accompanied by the latest price movement, though a more sustained rise would be needed to confirm a decisive shift in trend direction.

Kamada Ltd. (NASDAQ: KMDA), an Israel-based biopharmaceutical company specializing in plasma-derived protein therapeutics, reported strong Q3 and nine-month 2025 results supported by a diversified commercial portfolio, expanding profitability, and disciplined operational execution. The Company delivered double-digit revenue and EBITDA growth, strengthened cash generation, and maintained a solid cash position of USD 72 million while advancing key clinical programs, including the SHIELD study for CYTOGAM® and its pivotal Phase 3 InnovAATe trial for inhaled AAT therapy. Kamada also expanded its plasma collection infrastructure with FDA approval of its Houston facility and continued pursuing additional regulatory clearances and long-term supply agreements. Management reaffirmed its full-year guidance, reflecting confidence in sustained top- and bottom-line expansion. Technically, KMDA has been trading in a broad consolidation range with recent stabilization above key moving averages, a neutral-to-positive RSI near 57, and modest but improving volume activity indicating early signs of strengthening momentum.

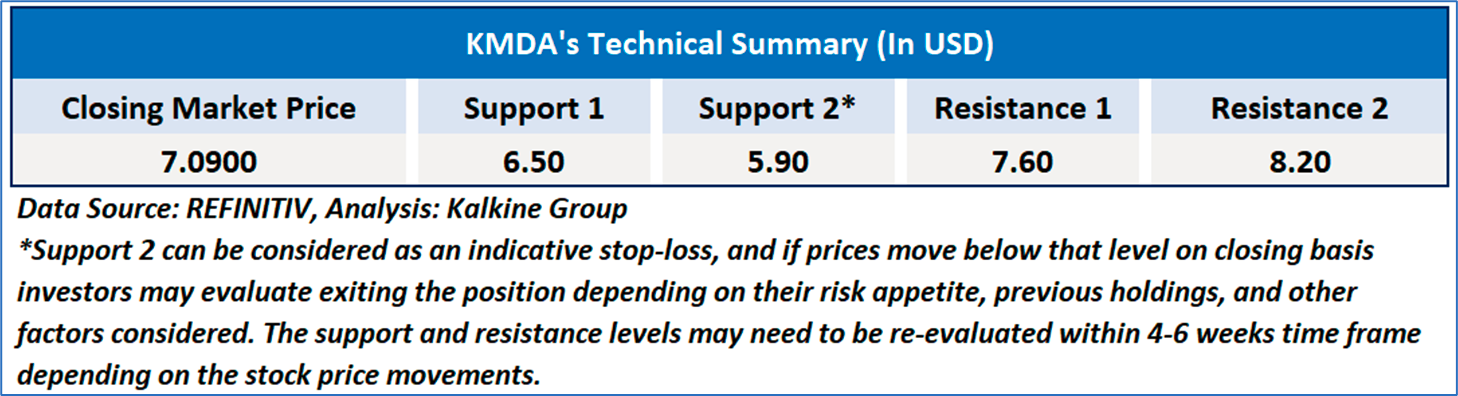

As per the above-mentioned price action, important support near USD 6.70-USD 7.00, momentum in the stock over the last month, and technical indicators analysis, a ‘Speculative Buy’ rating has been given for Kamada Ltd (NASDAQ: KMDA) at the closing price of USD 7.09, as of December 03, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective, and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 03, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...