Rooftop Solar Fallout

The recent tax bill passed by the U.S. House under President Trump proposes eliminating the 30% federal tax credit for residential rooftop solar by the end of 2025, significantly impacting Sunrun and Enphase Energy. Sunrun, which relies heavily on leased solar systems benefiting from the credit, saw its stock drop nearly 41%, facing serious threats to its core business model. Enphase Energy's stock declined around 20%, with added concerns over potential tariff-related cost increases on imported battery components. The accelerated phase-out of solar incentives threatens to raise household electricity costs and cause job losses within the solar sector. Both companies are confronting increased financial uncertainty as analysts revise valuations downward. The bill now moves to the Senate, where its outcome will critically shape the future of rooftop solar adoption and the operational viability of these leading solar technology firms.

Enphase Energy, Inc

Enphase Energy, Inc (NASDAQ: ENPH) is a worldwide energy technology firm that provides microinverter-based solar and battery systems. These systems allow users to generate, use, store, and sell their own solar power, all managed through a smart mobile app. The company designs, develops, manufactures, and markets integrated home energy solutions that oversee power generation, storage, control, and communication through a unified intelligent platform.

Business Updates

- Enphase Launches AI-Driven IQ® Energy Management in France: ENPH has introduced its new IQ® Energy Management system in France. This innovative solution integrates with Enphase’s solar and battery systems to intelligently manage variable electricity rates and control third-party devices such as EV chargers, heat pumps, and electric water heaters. Powered by artificial intelligence, the system enables homeowners to optimize energy use and reduce costs, all managed through the Enphase® App.

- Enphase Energy Reports Q1 2025 Financial Performance: Enphase Energy reported revenue of USD 356.1 million for the first quarter of 2025, down from USD 382.7 million in Q4 2024, reflecting a 13% decrease in U.S. revenue due to seasonal trends and weaker domestic demand. This decline was partially offset by USD 54.3 million in safe harbor revenue. In contrast, European revenue increased by approximately 7% quarter-over-quarter, driven by stronger battery sales, particularly the IQ® Battery 5P with FlexPhase. The company shipped around 1.53 million microinverters (688.5 MW DC) and 170.1 MWh of IQ Batteries during the quarter.

- Profitability and Margins Reflect Market Conditions: Enphase achieved a GAAP gross margin of 47.2% and a non-GAAP gross margin of 48.9% in Q1 2025. Excluding the net benefit from the Inflation Reduction Act (IRA), the non-GAAP gross margin was 38.3%, compared to 39.7% in Q4 2024. The decline was largely attributed to changes in product mix and a reduction in bookings of 45X production tax credits. Operating income on a non-GAAP basis was USD 94.6 million, down from USD 120.4 million in the prior quarter, while GAAP operating income came in at USD 31.9 million. Net income reached USD 89.2 million on a non-GAAP basis, with diluted earnings per share at USD 0.68.

- Operational Strength and Cash Management: During Q1 2025, Enphase shipped approximately 1.21 million microinverters and 44.1 MWh of batteries from its U.S.-based manufacturing facilities, qualifying for the 45X production tax credits. The company ended the quarter with a strong cash position of USD 1.53 billion, supported by USD 48.4 million in operating cash flow and USD 33.8 million in free cash flow. Capital expenditures increased to USD 14.6 million from USD 8.1 million in Q4 2024. Enphase repaid USD 102.2 million in convertible senior notes and repurchased 1.59 million shares for roughly USD 100 million, while also reducing diluted shares through employee tax withholdings.

- Product Expansion and Market Penetration: Enphase made significant product advancements in Q1 2025, including the continued global rollout of the IQ Battery 5P with FlexPhase and the launch of the IQ EV Charger 2 in 14 European countries. These products, along with the IQ® PowerPack 1500 for portable energy needs, have expanded the company's market footprint. The IQ Battery 5P is now available in multiple European markets and praised for its reliability in both single- and three-phase installations. The EV Charger 2 supports up to 22 kW charging and can operate independently or as part of an integrated Enphase system.

- Ongoing Developments and Strategic Initiatives: Throughout Q1 2025, Enphase announced several milestones, including expanded support for virtual power plants in Puerto Rico, Colorado, and Nova Scotia, and the integration of its systems into new solar safety standards in Brazil. Over 10,900 installers are now certified to install IQ Batteries, up from 10,300 in Q4 2024. The company also welcomed over 2,500 former SunPower customers onto its monitoring platform following SunPower’s bankruptcy. Looking ahead, Enphase plans to launch new products in Q2 2025 such as the IQ Battery 10C, IQ Meter Collar, and IQ Combiner 6C in the U.S., and the IQ Balcony Solar Kit in Germany and Belgium.

- Second Quarter 2025 Outlook: For Q2 2025, Enphase anticipates revenue between USD 340 million and USD 380 million, including shipments of 160 to 180 MWh of IQ Batteries and around USD 40 million in safe harbor revenue. The company expects GAAP gross margin between 42% and 45%, and non-GAAP gross margin between 44% and 47%, or 35% to 38% excluding IRA benefits. The net benefit from the IRA is projected at USD 30 million to USD 33 million, based on one million units of U.S.-manufactured microinverters. Operating expenses are forecasted at USD 136 million to USD 140 million (GAAP) and USD 78 million to USD 82 million (non-GAAP).

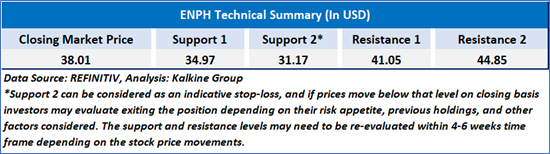

Technical Observation (on the daily chart):

Enphase Energy (ENPH) is exhibiting a strong bearish trend, with its price sharply declining by nearly 20% on high volume, closing at USD 38.01—well below its 21-day and 50-day moving averages. The RSI is nearing oversold territory at 32.25, suggesting potential for a short-term bounce, though overall momentum remains negative.

Sunrun Inc

Sunrun Inc (NASDAQ: RUN) offers clean energy through a subscription-based model. The company focuses on designing, developing, installing, selling, owning, and maintaining residential solar energy systems across the United States. It delivers solar power to homeowners, often at a lower cost than conventional utility energy, with residential homeowners as its main customer base.

Business Updates

- Sunrun Delivers Strong First Quarter Performance in 2025: Sunrun Inc, the nation's leading clean energy subscription provider, reported robust financial and operational results for the quarter ending March 31, 2025. Despite Q1 being a seasonally low period for solar installations, the company exceeded both its volume and cash generation targets. CEO Mary Powell emphasized the company's strategic focus on high-margin volumes, customer-centric innovation, and disciplined cost management, including AI integration to enhance operational efficiency. Powell noted Sunrun’s readiness to adapt to a dynamic policy environment surrounding tariffs and tax credits, reaffirming confidence in the company’s ability to sustain meaningful cash generation throughout the year.

- Continued Strength in Cash Generation and Debt Reduction: CFO Danny Abajian highlighted Sunrun’s fourth consecutive quarter of positive cash generation, with USD 56 million in Q1 2025. The company reiterated its full-year cash generation guidance of USD 200 to USD 500 million. Demonstrating prudent financial management, Sunrun reduced its recourse parent debt by USD 27 million during the quarter and by USD 214 million over the past year. Additionally, the company increased its unrestricted cash by USD 118 million and expanded its net earning assets by USD 1.6 billion. Sunrun confirmed it has no near-term corporate debt maturities, aside from USD 5.5 million of convertible notes due in 2026, and plans to further reduce recourse debt by at least USD 100 million in 2025.

- Surging Demand for Storage and Capital Market Activity: The first quarter saw a significant rise in storage adoption, with Sunrun reporting a 69% storage attachment rate — up from 50% a year earlier — and a 46% year-over-year increase in customer additions with storage. Storage capacity installed reached 334 megawatt hours, a 61% increase, while solar capacity installed rose 8% to 191 megawatts. In capital markets, Sunrun successfully executed two securitizations in Q1: a USD 369 million private placement in March and a USD 629 million oversubscribed public transaction in January. Both deals maintained advance rates above 80% after fees, underlining the market’s confidence in Sunrun’s subscriber portfolio.

- Innovation with Sunrun Flex and Virtual Power Plants: Sunrun launched a new subscription model, Sunrun Flex, in Q1 2025. Flex is tailored to evolving household energy needs, offering customers predictable minimum payments, usage-based charges for excess consumption, and the benefit of energy backup via battery storage. This innovation positions Sunrun to serve households adopting electric vehicles or expanding energy usage. Additionally, Sunrun expanded its CalReady virtual power plant, now comprising over 75,000 batteries capable of delivering 250 megawatts per event and peaking at 375 megawatts—enough to power all of Ventura County, California. This program supports grid stability and provides compensation to participating customers.

- Subscriber and Financial Metrics Reflect Robust Growth: Sunrun’s subscriber base grew 14% year-over-year to 912,878 as of March 31, 2025, with 23,692 new additions in Q1, a 7% increase from the previous year. Net Subscriber Value surged 66% to USD 10,390, while Contracted Net Subscriber Value grew 90% to USD 6,910. Aggregate Subscriber Value reached USD 1.2 billion, a 23% increase, and Contracted Net Value Creation doubled to USD 164 million. These figures reflect improved tax credit realization (43.6% average Investment Tax Credit), a slightly reduced discount rate, and continued strength in Sunrun’s customer value proposition despite a 7% increase in creation costs per subscriber.

- Positive Outlook for 2025 and Sustained Value Creation: Looking ahead, Sunrun expects continued growth in key metrics. For Q2 2025, Aggregate Subscriber Value is projected between USD 1.3 billion and USD 1.375 billion, with Contracted Net Value Creation between USD 125 million and USD 200 million. Expected cash generation for the quarter ranges from USD 50 million to USD 60 million. For full-year 2025, the company maintained its guidance, projecting Aggregate Subscriber Value between USD 5.7 billion and USD 6.0 billion and Contracted Net Value Creation of USD 650 million to USD 850 million. These targets underscore Sunrun’s confidence in its scalable model and its ability to deliver long-term shareholder value through disciplined execution and market leadership.

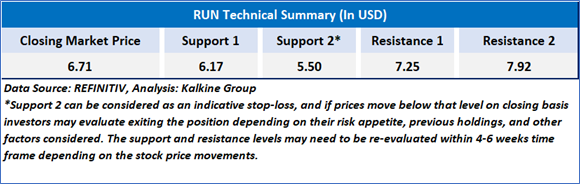

Technical Observation (on the daily chart):

Sunrun Inc experienced a sharp drop on heavy volume, breaking below key moving averages and signaling a failed breakout. The stock had recently rallied above its 50-day and 21-day moving averages, hinting at a reversal, but the latest selloff suggests renewed bearish momentum. The RSI has fallen to 38.5, nearing oversold territory, while the high volume indicates potential panic selling or a major negative catalyst.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is May 22,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...