Grand Canyon Education, Inc.

LOPE Details

Grand Canyon Education, Inc. (NASDAQ: LOPE) is a for-profit education services company and currently offers its services to 27 university partners in the US. It also provides various support services in the post-secondary education sector using its technological solutions, infrastructure, and operational processes. Its services assist students and staff/faculty of partner universities in marketing, enrollments, counseling, financial services, technology, tech-support, compliance, human resources, classroom operations, content development, training and recruitment, etc. As of November 01, 2021, LOPE’s market capitalization stood at USD 3.98 billion.

Latest News:

- Receipt of Partial Debt Re-Payment by GCU: On October 28, 2021, Grand Canyon University (GCU) informed LOPE of its intentions to repay USD 500.0 million of the outstanding amount under the secured note issued to LOPE as part of an Asset Purchase Agreement (APA) signed in 2018. LOPE further stated that it plans to use these proceeds to repay and subsequently terminate its term loan and revolving credit facilities under its GCE Credit Agreement, and for share repurchases and general corporate purposes.

Q3FY21 Results:

- Growth in Revenue: The company reported a slight uptick of 4.23% in its revenue to USD 206.77 million in Q3FY21 (ended September 30, 2021) from USD 198.38 million in Q3FY20, resulting primarily from an increase in university partner enrollments and revenue per student.

- Student Enrollments: At quarter-end, total partner enrollments were 118,832 vs. 117,772 at Q3FY20 end. University partner enrollments at off-campus classroom and laboratory sites increased 12.1% YoY to 5,652, while the GCU ground student numbers grew 9.5% YoY to 23,628.

- Decline in Net Income: Its Q3FY21 net income was USD 47.66 million vs. USD 52.05 million reported in Q3FY20.

- Strong Balance Sheet: LOPE exited the quarter with a cash balance of USD 61.00 million and a total debt of USD 82.92 million.

Key Risks:

- Revenue Concentration: GCU accounted for the majority of the company's revenue in FY20. As a result, any decrease in GCU enrollments or the termination of their contractual agreement could be harmful to the company.

- Regulatory Risk: The higher education industry is subject to extensive regulatory scrutiny. Any compliance failure on the part of the company or its university partners could result in financial penalties and restrictions and a negative impact on LOPE's brand reputation.

Outlook:

- Q4FY21 Estimate: In its Q3FY21 earnings release, LOPE stated that its Q4FY21 revenue is expected to range between USD 252.0 – 255.0 million, with an adjusted diluted EPS of USD 2.08 – 2.13.

- FY21 Guidance: The estimated range for FY21 revenue and EPS is USD 897.2 – 900.2 million and USD 6.05 – 6.10, respectively.

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

(Analysis by Kalkine Group)

* % Premium/(Discount) is based on our assessment of the company's NTM trading multiple after considering its key growth drivers, economic moat, stock's historical trading multiples versus peer average/median, and investment risks.

LOPE Daily Technical Chart (Source: REFINITIV)

Stock Recommendation:

LOPE's stock price has surged 13.51% in the past twelve months and is currently leaning towards the lower end of the 52-week range of USD 76.96 to USD 115.96. The stock is currently trading between its 50 and 200 DMA levels, and its RSI Index is 50.27. We have valued the stock using the EV/EBITDA-based relative valuation methodology and arrived at a target price of USD 82.13.

Considering the uptick in the stock price, we believe the decent fundamentals are sufficiently reflected at the current trading levels and hence, recommend a "Sell" rating on the stock at the closing price of USD 88.12, up 10.56% as of November 01, 2021.

* The reference data in this report has been partly sourced from REFINITIV.

* All forecasted figures and industry information have been taken from REFINITIV.

Desktop Metal, Inc.

DM Details

Desktop Metal, Inc. (NYSE: DM) uses additive manufacturing (AM) technology to create end-use parts (3D printing solutions) and offers comprehensive AM solutions, including hardware, software, materials, and services for diverse industrial and commercial end-users. It generates revenue by selling AM equipment and related parts and consumables, providing installation, training, post-installation hardware and software support, and other software solutions. As of November 01, 2021, DM's market capitalization stood at USD 1.82 billion.

Latest News:

- New Facility Opening: On November 01, 2021, DM announced the inauguration of a new in-house production facility, which triples the current final assembly space allocated to the Production SystemTM platform. The new facility aims to speed up manufacturing of the company's flagship Production System P-50 printer to cater to the strong demand for the world's fastest metal 3D printing technology, with shipments targeted for Q4FY21.

- 420 Qualification for High-Strength Manufacturing: On October 22, 2021, the company stated that Grade 420 stainless steel (420 SS) was qualified for use on its Production System platform, which uses the Single Pass Jetting (SPJ) technology to deliver the fastest build speed. Using this technology, manufacturers can mass-produce high-strength, end-use parts in 420 SS for various demanding applications in medical, aerospace, defense, and consumer products industries.

Q2FY21 Results:

- Significant Growth in Revenue: The company's revenue for Q2FY21 (ended June 30, 2021) amounted to USD 18.98 million, 7.67x more than USD 2.19 million reported in Q2FY20, resulting from higher product sales and related support and installation revenue.

- Increase in Net Loss: However, net loss for Q2FY21 increased to USD 43.18 million from USD 23.77 million in Q2FY20.

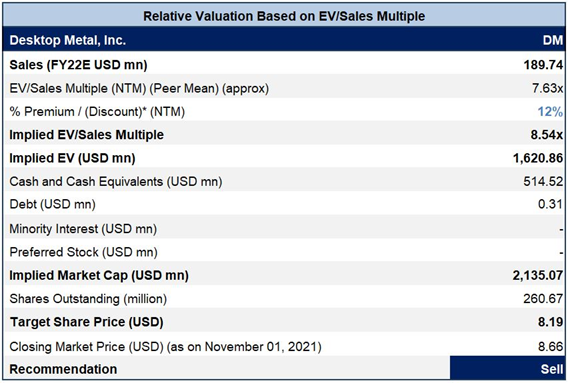

- Strong Balance Sheet: As of June 30, 2021, the company had cash and cash equivalents (including short-term investments) of USD 514.52 million and total debt of USD 0.31 million.

Key Risks:

- Stiff Competition: DM competes directly with big competitors who have more financial and operational resources at their disposal in the highly fragmented and competitive AM market. As a result, the creation of superior items or competitive pricing pressure could jeopardize its operations.

- Third-Party Dependence: The majority of the company's manufacturing operations are reliant on third-party manufacturers. Any breach of contract by third parties in buying components or performing subcontract engineering work could hurt the company's operations.

Outlook:

- Revenue Estimate: In FY21, DM expects to generate over USD 100 million in revenue, with an annualized revenue run rate of USD 160 million (excluding the adjustments relating to the ExOne acquisition announced on August 11, 2021).

- EBITDA Range: Its adjusted EBITDA is estimated to range between USD (80) – (70) million, excluding the ExOne acquisition.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

(Analysis by Kalkine Group)

* % Premium/(Discount) is based on our assessment of the company's NTM trading multiple after considering its key growth drivers, economic moat, stock's historical trading multiples versus peer average/median, and investment risks.

DM Daily Technical Chart (Source: REFINITIV)

Stock Recommendation:

DM's stock price has surged 21.46% in the past week and is currently leaning towards the lower band of its 52-week range of USD 6.70 to USD 34.94. The stock is currently trading between its 50 and 200 DMA levels, and its RSI Index is at 66.88, indicating an overbought zone. We have valued the stock using the EV/Sales-based relative valuation methodology and arrived at a target price of USD 8.19.

Considering the significant uptick in the stock price in a short span, the current valuation, and associated risks, we recommend a "Sell" rating on the stock at the closing price of USD 8.66, up 23.89% as of November 01, 2021.

* The reference data in this report has been partly sourced from REFINITIV.

* All forecasted figures and industry information have been taken from REFINITIV.

Disclaimer

The advice given by Kalkine Canada Advisory Services Inc. and provided on this website is general information only and it does not take into account your investment objectives, financial situation and the particular needs of any particular person. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. The website www.kalkine.ca is published by Kalkine Canada Advisory Services Inc. The link to our Terms & Conditions has been provided please go through them. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Please wait processing your request...

Please wait processing your request...