Pony AI Inc

Pony AI Inc (NASDAQ: PONY) operates as a holding company focused on bringing autonomous driving technology to market. Its business is centered around three main service lines, including Robotaxi offerings that deliver ride-hailing services to individual customers using self-driving vehicles, as well as providing engineering solutions to support autonomous taxi operations.

Key Growth Aspects

- Strong Momentum in Commercialization and Fleet Expansion: ai is rapidly scaling its Robotaxi operations, supported by accelerated fleet deployment and meaningful topline growth. By late 2025, the company had already rolled out more than 900 Robotaxis and now expects its fleet to surpass 1,000 vehicles ahead of schedule, with a target of over 3,000 vehicles by 2026. This expansion is reinforced by a powerful “flywheel effect,” where higher fleet density improves user experience, increases adoption, and further boosts demand. This scaling momentum has also translated into robust financial performance, including 90% year-on-year Robotaxi revenue growth in Q3 2025 and fare-charging revenue growth exceeding 200% over the same period.

- Technology Leadership Anchored in Full-Stack Innovation: The company highlights a clear competitive edge through its fully integrated technology stack, centered on its proprietary “PonyWorld” world-model platform. This simulation-driven, reinforcement-learning environment enables self-improving, closed-loop training, supporting safer and more adaptive autonomous driving over time. Pony.ai believes this approach places it at the forefront of Level-4 autonomy development, reinforced by cost-efficient hardware innovation such as its fully automotive-grade autonomous driving kits, which have driven substantial reductions in bill-of-materials costs compared with prior generations.

- Clear Path Toward Improved Unit Economics: The business model has shown tangible progress toward financial sustainability. Pony.ai recently achieved city-wide unit economics breakeven in Guangzhou following the launch of its Gen-7 Robotaxi fleet. Daily net revenue per vehicle reached RMB 299, supported by strong order density and improved operational efficiency. In addition, gross margins improved materially year-on-year to 18.4% in Q3 2025, reflecting a more favorable revenue mix and greater Robotaxi contribution. These metrics provide confidence in the viability of the company’s asset-light expansion strategy, which relies on third-party partners to fund vehicle deployment.

- Strengthened Capital Position and International Expansion: ai’s dual-primary listing on the Hong Kong Stock Exchange in November 2025 raised over USD 800 million, marking the largest autonomous driving IPO globally that year. This capital injection significantly bolsters liquidity, supporting mass production, further commercialization, and deepened R&D investment. At the same time, the company continues to broaden its geographic footprint, now present in eight countries across Asia, the Middle East, Europe, and the United States, often in partnership with established regional transport operators and global ride-hailing platforms.

Growth Challenges

- Sustained Operating Losses and Heavy Cash Outflows: Despite strong revenue gains, the company continues to incur significant net losses. In Q3 2025, Pony.ai reported a GAAP net loss of USD 61.6 million, widening from the prior year period, with substantial non-GAAP losses also persisting. Free cash outflow reached USD 173.6 million in the first nine months of 2025, reflecting both operational burn and capital expenditures tied to scaling activities. This indicates that the business still requires meaningful external funding to sustain growth, heightening execution pressure as it pursues profitability at scale.

- High Cost Base Driven by R&D and Deployment Build-Out: While technology leadership remains a core strength, it also comes at a significant financial cost. Operating expenses rose sharply year-on-year, with non-GAAP operating expenses up 63.7% in Q3 2025. This increase was partly driven by one-off customization expenses tied to Gen-7 development, alongside ongoing expansion of the R&D workforce. The company signals its intent to continue investing heavily to maintain differentiation, which may delay operating leverage and pressure margins in the near term.

- Execution and Regulatory Complexity Across Markets: Scaling Level-4 autonomous services across multiple regions introduces operational and regulatory challenges. Deployment requires proving safety standards, securing appropriate licenses, adapting systems to local driving conditions, and coordinating with municipal authorities and OEM partners. Management acknowledges that rollout pace must be aligned with fleet density, infrastructure readiness, and regulatory approvals, meaning expansion is not only capital intensive but also operationally complex and dependent on external stakeholders.

- Reliance on Partnerships and Evolving Business Model: ai’s asset-light strategy—where third-party partners purchase and operate Robotaxi fleets—aims to improve capital efficiency. However, this approach also increases its reliance on external operators, technology licensing arrangements, and OEM collaborations. The long-term economics of these relationships are still evolving, and any disruption or misalignment could affect deployment momentum and revenue mix. Furthermore, the broader robotaxi industry remains competitive and nascent, meaning long-term demand patterns and pricing power are still being tested in real-world conditions.

Key Risks

- High R&D and deployment costs linked to maintaining technology leadership, which may delay operating leverage and profitability.

- Regulatory and operational execution risk, as large-scale driverless deployment depends on city-by-city approvals, infrastructure readiness, and proven safety records.

- Reliance on strategic partners and evolving business models (OEMs, fleet operators, ride-hailing platforms), which may introduce dependency and coordination risk.

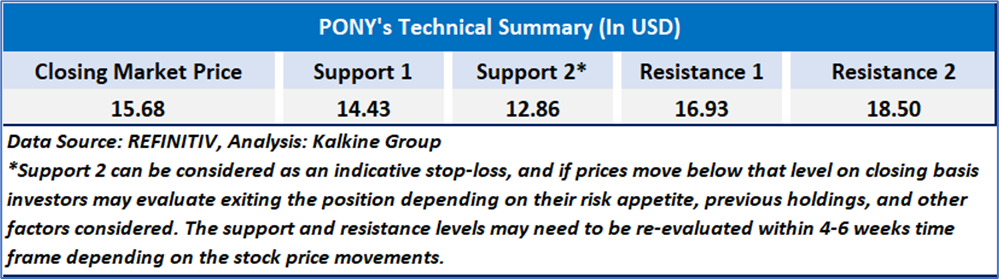

Technical Observation (on the daily chart):

The stock appears to be stabilizing after a recent decline, with price recovering above the 20-day moving average and testing the 50-day moving average, indicating early but tentative signs of improving momentum. The RSI around 60 supports a mildly bullish bias, though resistance remains in the USD 17–18 range and again near USD 20. Support has formed around USD 13–14, and a sustained break above the 50-day MA with stronger volume would be needed to confirm a clearer trend reversal.

Pony.ai presents a mixed investment case. On the positive side, the company is rapidly scaling its Robotaxi fleet, delivering strong revenue growth (including over 200% growth in fare-charging revenue) and has even achieved city-wide unit-economics breakeven in Guangzhou following the launch of its Gen-7 vehicles. Its fully integrated technology stack and significant cost reductions in autonomous hardware further strengthen its competitive positioning. However, this expansion remains capital-intensive, with the company still reporting sizeable operating losses and material cash outflows, alongside rising R&D spending to sustain innovation. Moreover, large-scale rollout across multiple regions continues to involve regulatory, operational, and partnership-execution risks. As a result, Pony.ai combines compelling growth momentum and technological leadership with meaningful financial and execution uncertainties.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given Pony AI Inc (NASDAQ: PONY) at the closing market price of USD 15.68 as of Dec 24,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 24,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...