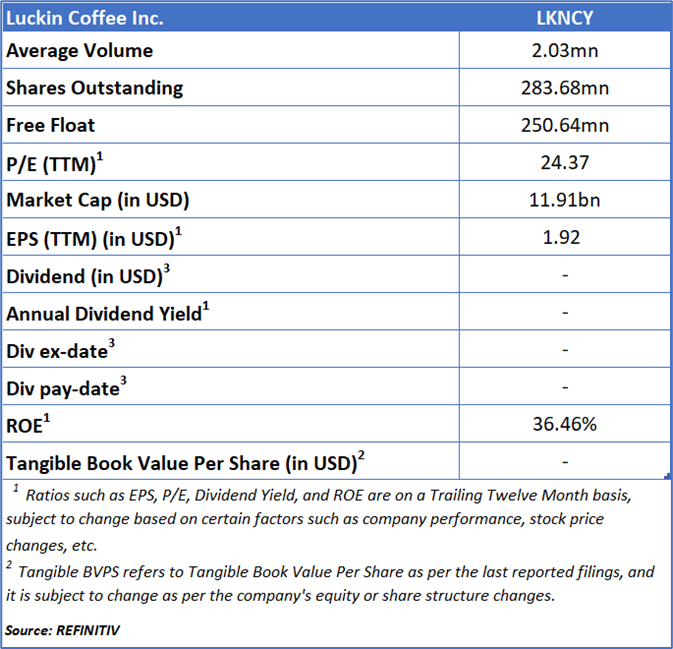

Luckin Coffee Inc.

Luckin Coffee Inc. (OTC: LKNCY) is a China-based holding company engaged in the coffee retail business. It leverages a new retail model that integrates technology into coffee sales and services. The company primarily operates through mobile applications and pick-up stores, offering a range of products such as freshly brewed beverages, juices, and light meals under its flagship brand, Luckin Coffee.

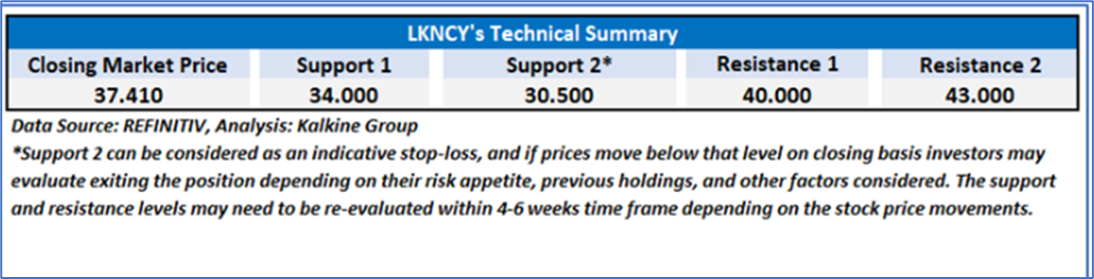

As per our previous Kalkine’s Inflation Report published on ‘LKNCY’ on Jul 24, 2025, Kalkine provided an ‘Buy’ stance on the stock at USD 37.41 based on fundamental analysis and the stock price has now moved up by ~ 12.83% since then.

Noted below are the details of support and resistance levels provided in our previous report:

Rationale:

- Margin Pressure Despite Strong Revenue Growth: While Luckin Coffee delivered impressive top-line expansion, profitability indicators revealed underlying margin pressure. The company’s store-level operating margin for self-operated stores declined slightly to 21.0%, compared to 21.5% in the prior year. Similarly, the GAAP operating margin, though higher year-over-year at 13.8%, was constrained by the rapid rise in operating expenses. These figures suggest that while Luckin’s aggressive expansion strategy continues to drive revenue, the cost intensity associated with scaling operations and maintaining quality standards remains a structural challenge.

- Escalating Operating Costs Impact Efficiency: Luckin Coffee’s total operating expenses surged 45.0% year-over-year to RMB10.7 billion, nearly in line with its revenue growth, indicating persistent cost pressures. The largest contributors were delivery expenses, which skyrocketed 175.1%, and store rental and other operating costs, which rose 30.0%. Increased labor, rental, and logistics costs reflect both the burden of a fast-growing store network and higher operational complexity. Although cost of materials as a percentage of revenue decreased slightly, the continued escalation of other expense categories poses risks to future operating efficiency if not managed effectively.

- Declining Net Margin and Profitability Ratios: Despite a significant jump in net income, Luckin’s net margin slipped to 10.1%, compared to 10.4% a year earlier. The non-GAAP net margin also edged down to 11.3% from 11.6%, reflecting an inability to fully translate strong revenue momentum into proportional earnings growth. This compression highlights the potential strain of rising input costs, marketing expenditures, and administrative spending on overall profitability. The widening gap between revenue and margin growth may indicate that the company’s current growth phase is still heavily investment-driven rather than efficiency-led.

- Intensifying Expansion Risks and Market Saturation: Luckin Coffee’s continued aggressive expansion — with 2,109 new stores opened during the quarter, bringing the total to 26,206 — introduces both operational and market saturation risks. While scale has been a competitive advantage, such rapid growth heightens the risk of cannibalization between self-operated and partnership stores, especially in urban markets with dense store concentration. Additionally, managing quality control, supply chain coordination, and franchise oversight across multiple geographies (including newer markets like Singapore, Malaysia, and the U.S.) adds strategic and operational complexity. If not carefully balanced, this expansion-driven model could erode efficiency and weaken brand cohesion over time.

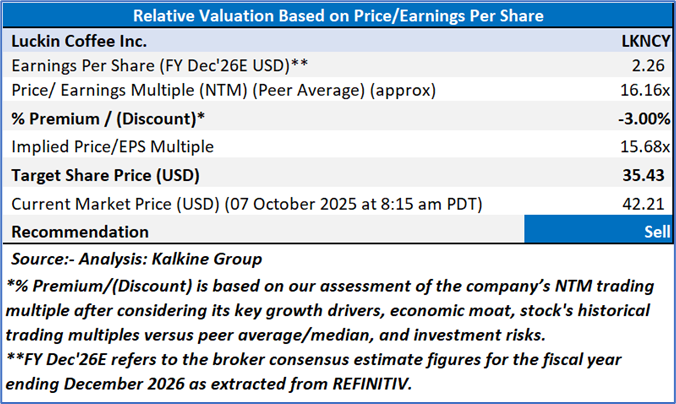

Valuation (Using P/E Value Multiple)

Share Price Chart

Conclusion

Despite strong revenue and store growth, Luckin Coffee faces mounting cost pressures and declining profitability ratios. Operating expenses surged nearly in line with revenues, driven by higher delivery, rental, and labor costs, which slightly compressed margins. The company’s net margin fell year-over-year, reflecting limited efficiency gains despite scale expansion. Moreover, its aggressive store rollout heightens operational risks and potential market saturation, suggesting that Luckin’s growth remains heavily reliant on expansion rather than sustainable margin improvement.

Based on the notional gains, potential downside and price action stance, a "Sell" recommendation on Luckin Coffee Inc. (OTC: LKNCY) has been given at the current market price of USD 42.21 as on 07 October 2025 at 8:15 am PDT.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 07 October 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...