Zevra Therapeutics Inc

Zevra Therapeutics, Inc. (NASDAQ: ZVRA) is a commercial-stage rare disease company combining science, data, and patient need to create transformational therapies for diseases with limited or no treatment options. It has a diverse portfolio of products and product candidates, which includes pre-clinical, clinical, and commercial stage assets.

Key Business and Financial Updates:

- Commercial Performance: The commercial landscape for Zevra showcased promising progress, particularly with MIPLYFFA®, which recorded seven prescription enrollment forms in Q2 2025, accumulating a total of 129 since its launch, and achieved market access for 52% of covered lives, aligning with early-stage launch expectations. In contrast, OLPRUVA saw modest activity with one prescription enrollment form, bringing its total to 29, while improving market access to 79% of covered lives, reflecting a steady expansion in its therapeutic reach. These developments underscore Zevra’s commitment to delivering MIPLYFFA®—the only treatment demonstrated to halt NPC progression by targeting its underlying pathology—as a transformative option, while the recent MAA submission aims to extend these benefits to European patients, potentially broadening its global footprint.

- Pipeline and Innovation: Zevra’s pipeline continues to demonstrate significant potential, highlighted by the timely submission of the arimoclomol MAA to the EMA in the second half of 2025, reinforced by its Orphan Medicinal Product designation, with the drug already marketed as MIPLYFFA® in the U.S. The Phase 3 DiSCOVER trial for celiprolol in treating Vascular Ehlers-Danlos Syndrome progressed with the enrollment of seven additional patients in Q2 2025, increasing the total to 39, indicating steady advancement toward addressing unmet medical needs. These innovations position Zevra as a leader in rare disease therapeutics, leveraging its existing approvals and ongoing clinical trials to enhance its product portfolio and market presence.

- Financial Highlights: Financially, Zevra reported a Q2 2025 net revenue of USD 25.9 million, comprising USD 21.5 million from MIPLYFFA, USD 0.3 million from OLPRUVA, USD 2.6 million in French Early Access Program reimbursements for arimoclomol, USD 1.2 million in royalties from the AZSTARYS® license, and a USD 0.3 million upfront payment from a dextrorphan prodrug out-license. Despite a cost of product revenue of USD 14.0 million, including a USD 11.7 million inventory obsolescence expense and a USD 58.7 million non-cash intangible asset impairment charge, the company achieved a net income of USD 74.7 million, or USD 1.24 per basic share, a stark improvement from a USD 19.9 million loss in Q2 2024, bolstered by USD 148.3 million in PRV sale proceeds. With cash, cash equivalents, and securities totaling USD 217.7 million as of June 30, 2025, Zevra maintains sufficient liquidity to pursue its strategic priorities without immediate reliance on capital markets.

- Strategic Outlook: Led by President and Chief Executive Officer Neil F. McFarlane, Zevra is at an exhilarating juncture of growth, capitalizing on the successful U.S. launch of MIPLYFFA® and the financial bolster from the PRV sale to fuel its commercial and developmental endeavors. The company’s strategic focus on expanding arimoclomol’s reach through the EMA submission and advancing the celiprolol trial reflects a commitment to addressing rare disease challenges globally. With a fortified balance sheet and a projected operational runway, Zevra is well-positioned to enhance patient access, innovate its pipeline, and deliver sustained value, despite challenges such as inventory obsolescence and impairment charges, which are viewed as one-time adjustments in its growth trajectory.

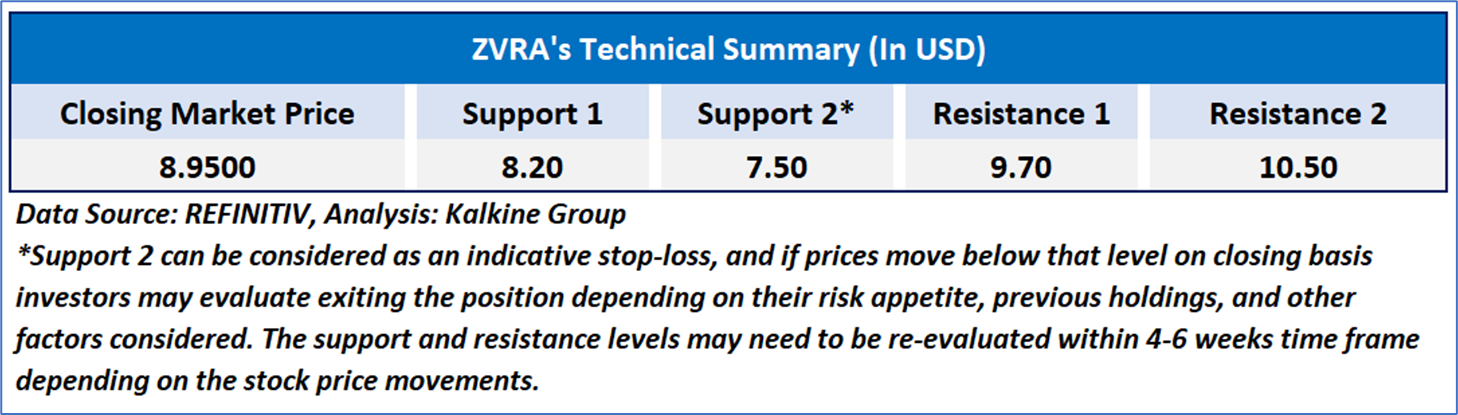

Technical Observation (on the daily chart):

- Price Trend and Momentum: ZVRA closed at USD 8.95, registering a robust +10.36% daily gain, which reflects renewed bullish momentum. The stock has rebounded strongly from its local low of USD 7.16 recorded on 16th September 2025, indicating solid buying interest at lower levels. Although it continues to trade below the 50-day moving average (USD 9.82), which poses near-term resistance, it has reclaimed levels above the 200-day moving average (USD 8.69), suggesting that the longer-term trend remains intact and that the counter is showing signs of recovery.

- Support, Resistance, and Technical Indicators: Key support is placed at USD 8.69 (200-day MA) and USD 8.00, with strong support at USD 6.20, the 52-week low. On the upside, immediate resistance lies at USD 9.82 (50-day MA), followed by a broader resistance zone between USD 11.50 and USD 12.00, with a major ceiling at USD 13.16 (52-week high). The Relative Strength Index (RSI) stands at 54.38, rebounding sharply from oversold levels near 30, highlighting the return of buying momentum. The stock is currently in a neutral RSI zone, leaving scope for further upside before approaching overbought territory.

- Outlook and Scenarios: The 50-day MA is trending downward, reflecting lingering short-term weakness, while the 200-day MA is flattening, signaling longer-term stabilization. The current price positioning between these moving averages indicates a potential consolidation phase before a clearer breakout. Overall, ZVRA exhibits early signs of recovery, and sustaining above the 200-day MA will be critical in confirming a bullish reversal trajectory.

As per the above-mentioned price action, important support near USD 7.50-USD 8.00, momentum in the stock over the last month, and technical indicators analysis, a ‘Speculative Buy’ rating has been given for Zevra Therapeutics, Inc. (NASDAQ: ZVRA) at the closing price of USD 8.95, as of September 24, 2025.

Taysha Gene Therapies Inc

Taysha Gene Therapies Inc (NASDAQ: TSHA) is a clinical-stage biotechnology company, which is focused on advancing adeno-associated virus (AAV)-based gene therapies for severe monogenic diseases of the central nervous system. The Company’s lead clinical program, TSHA-102, is in development for the treatment of Rett syndrome, a rare neurodevelopmental disorder.

Key Business and Financial Updates:

- Clinical and Therapeutic Advancements: Taysha has achieved notable progress with its TSHA-102 program, targeting Rett syndrome in females aged two years and older, with both high and low doses demonstrating favorable tolerability and the absence of treatment-related serious adverse events (SAEs) or dose-limiting toxicities (DLTs) across the 12 patients treated in Part A of the REVEAL Phase 1/2 trials as of the August 2025 data cutoff. Data from Part A, presented at the International Rett Syndrome Foundation (IRSF) Scientific Meeting, indicated a 100% response rate for the pivotal trial’s primary endpoint of achieving or regaining at least one developmental milestone, supported by positive trends in secondary endpoints. The company anticipates releasing additional supplemental Part A clinical data in Q4 2025 to further substantiate TSHA-102’s therapeutic efficacy, while the FDA’s approval of an extrapolation approach for a safety-focused study in the pre-developmental plateau population (aged 2 to <6 years) aims to expand treatment accessibility.

- Program and Regulatory Milestones: The REVEAL pivotal trial, structured as a single-arm, open-label study where each patient serves as their own control, has begun site activation following regulatory concurrence on critical design parameters, including a single high-dose administration (1x10¹⁵ total vector genomes) via lumbar intrathecal injection. This trial will enroll 15 females aged 6 to <22 years from the developmental plateau population of Rett syndrome, a group with a minimal likelihood (0% to <6.7%) of spontaneously regaining lost developmental milestones, based on Taysha’s extensive natural history data. The primary endpoint will evaluate the response rate based on a curated list of 28 milestones across communication, fine motor, and gross motor domains, assessed via standardized video recordings by independent, blinded central raters, with planned interim and 12-month primary analyses, leveraging the trial’s robust power as evidenced by prior Part A results.

- Financial Performance: For the second quarter ended June 30, 2025, Taysha recorded research and development expenses of USD 20.1 million, a USD 5.0 million increase from USD 15.1 million in Q2 2024, attributable to BLA-enabling manufacturing efforts, REVEAL trial activities, and elevated compensation costs due to increased headcount. General and administrative expenses rose to USD 8.6 million from USD 7.3 million, primarily due to higher legal and professional fees, resulting in a net loss of USD 26.9 million, or USD 0.09 per share, compared to a USD 20.9 million loss, or USD 0.09 per share, in Q2 2024. Nevertheless, the company’s cash and cash equivalents reached USD 312.8 million as of June 30, 2025, significantly bolstered by the USD 230 million follow-on offering, providing a solid financial base to sustain operational and capital needs through 2028.

- Strategic Outlook: Guided by Chairman and Chief Executive Officer Sean P. Nolan, Taysha is strategically positioned to advance TSHA-102 toward potential registration, benefiting from ongoing and productive engagements with the FDA through the Regenerative Medicine Advanced Therapy (RMAT) mechanism to navigate this innovative regulatory framework. The reinforced financial position, underpinned by the recent capital infusion, supports the progression of the pivotal trial and the planned safety-focused study, addressing the significant unmet needs of Rett syndrome patients. The encouraging clinical data and trial design, combined with a cash runway extending into 2028, position Taysha to deliver groundbreaking therapies, despite the current net loss reflecting substantial R&D investment, with anticipated milestones in Q4 2025 poised to strengthen its growth trajectory.

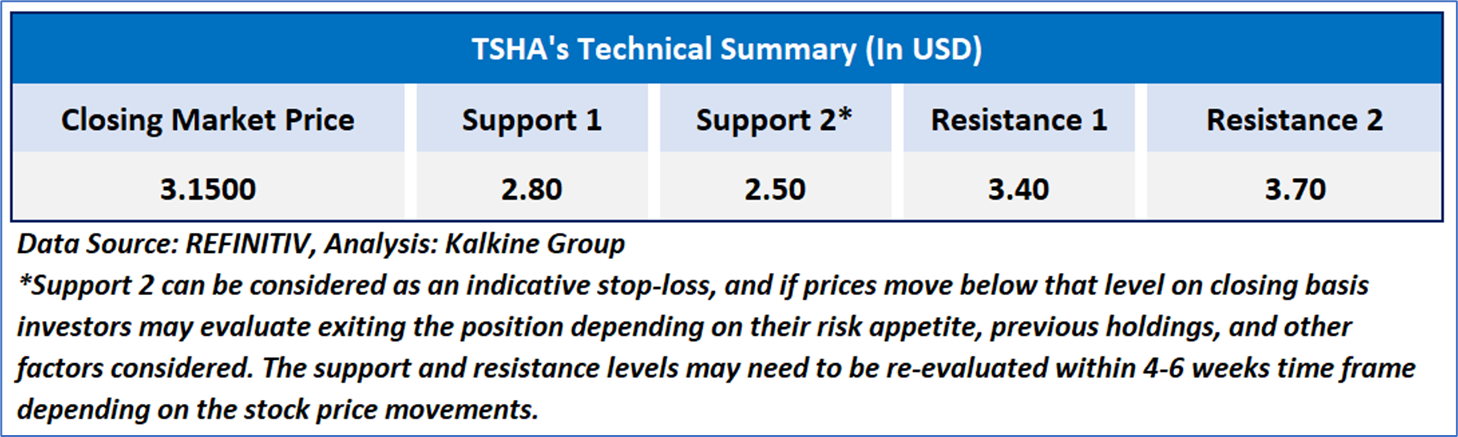

Technical Observation (on the daily chart):

- Trend and Price Action: TSHA closed at USD 3.15, gaining 7.88% in the latest session, reflecting strong bullish sentiment. The stock market has rebounded from its 50-day moving average (USD 2.87), which acted as immediate support, and remains firmly above the 200-day moving average (USD 2.20), confirming the continuation of its longer-term uptrend. With the recent bounce, the stock is approaching its near-term high of USD 3.40, a critical level that may determine the strength of further momentum.

- Support and Resistance Levels: Key support levels are placed at USD 2.87 (50-day MA) and USD 2.20 (200-day MA), providing a safety cushion against potential pullbacks. On the upside, the immediate resistance lies at USD 3.40, with the next resistance zone positioned around USD 3.80–4.00, where selling pressure could reappear. The RSI at 57.11 remains in neutral-to-bullish territory, suggesting room for further upward movement before entering overbought conditions.

- Technical Outlook: The overall setup favors a bullish bias if the stock sustains above its 50-day MA. A confirmed breakout above USD 3.40 could trigger upside toward the USD 3.80–4.00 range, strengthening the case for trend continuation. However, failure to hold above USD 2.87 may lead to consolidation, with USD 2.20 serving as a strong support base. Overall, TSHA is showing early bullish signals, supported by stabilizing moving averages and improving momentum, pointing toward further potential upside.

As per the above-mentioned price action, important support near USD 2.80-USD 3.00, momentum in the stock over the last month, and technical indicators analysis, a ‘Speculative Buy’ rating has been given for Taysha Gene Therapies Inc (NASDAQ: TSHA) at the closing price of USD 3.15, as of September 24, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is September 24, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

_09_25_2025_13_10_57_908723.jpg)

Please wait processing your request...

Please wait processing your request...