Oracle Corporation

Oracle Corporation (NYSE: ORCL) offers integrated suites of applications plus secure, autonomous infrastructure in the Oracle Cloud. The Company operates through three businesses: cloud and license, hardware and service.

Key Business and Financial Updates:

- Strong Top-Line Performance and Exceptional RPO Growth: Oracle delivered a robust fiscal Q2 FY2026, reporting total revenue of USD 16.1 billion, up 14% year-over-year in USD, supported by continued expansion in cloud services. The standout metric was Remaining Performance Obligations (RPO), which rose 438% year-over-year to USD 523 billion and grew 15% sequentially, driven by major new commitments from customers such as Meta and NVIDIA. This unprecedented RPO scale signals exceptionally strong multi-year demand visibility across Oracle’s cloud portfolio.

- Cloud Momentum Led by IaaS and Multicloud Adoption: Cloud revenue reached USD 8.0 billion, up 34% year-over-year, with Cloud Infrastructure (IaaS) posting an accelerated 68% growth to USD 4.1 billion as enterprises increasingly use Oracle Cloud for high-performance computing and AI workloads. SaaS revenues also remained solid, with Fusion Cloud ERP up 18% and NetSuite ERP up 13%. Oracle highlighted rapid progress in its multicloud strategy, reporting that its multicloud database business grew 817% as the company integrates 72 Oracle datacenters directly into AWS, Google Cloud and Microsoft Azure environments.

- Profitability Expansion Supported by Ampere Stake Sale: Profitability strengthened sharply, with GAAP EPS up 91% to USD 2.10 and Non-GAAP EPS up 54% to USD 2.26, uplifted by a USD 2.7 billion pre-tax gain from Oracle’s divestiture of its Ampere chip interest. GAAP net income reached USD 6.1 billion, while Non-GAAP net income rose 57% to USD 6.6 billion. Management emphasized that the Ampere sale aligns with Oracle’s shift toward “chip neutrality,” enabling the company to leverage diverse CPU and GPU architectures aligned with fast-changing AI requirements.

- Strategic Shift Toward Cloud Neutrality and AI-Embedded Software: Leadership reiterated Oracle’s commitment to cloud neutrality, allowing customers to deploy Oracle databases in any cloud environment. With more than 211 live and planned regions, Oracle positioned itself as a scale leader in automated, cost-efficient datacenter operations. Executives also underscored Oracle’s advantage in embedding AI across its datacenter software, autonomous database technologies, and application suites, enabling automation of complex workflows in sectors such as banking and healthcare. The presence of all top five AI models on Oracle Cloud reinforces its ambition to become a central platform for AI-driven enterprise operations.

- Cash Flow Strength and Continued Shareholder Returns: Oracle generated USD 22.3 billion in operating cash flow over the last twelve months, reflecting strong business fundamentals and sustained cloud adoption. Short-term deferred revenue stood at USD 9.9 billion, reinforcing visibility into future billing cycles. The board declared a quarterly cash dividend of USD 0.50 per share, payable January 23, 2026, underscoring the company’s continued commitment to disciplined capital returns alongside investment in its rapidly scaling cloud and AI initiatives.

Key Risks for Oracle Corporation (NYSE: ORCL):

- Dependence on Large Enterprise and Hyperscaler Partnerships: Oracle’s accelerating cloud and multicloud strategy relies heavily on sustained adoption by major enterprises and hyperscalers. Any slowdown, renegotiation, or loss of major cloud infrastructure or database clients could materially impact revenue visibility, especially given the outsized contribution from large RPO commitments.

- Execution Risk in Scaling Cloud Infrastructure and AI Integration: Oracle is undertaking rapid global datacenter expansion—over 211 regions live or planned—and embedding AI across all software layers. These initiatives require flawless execution, significant capital investment, and competitive pricing; delays, cost overruns, or performance issues could hinder Oracle’s ability to capture market share from more established cloud providers.

- Margin Pressure from Competitive Dynamics and Strategic Transition: As Oracle deepens its shift toward cloud neutrality and relies on third-party chips rather than proprietary designs, it faces rising procurement costs and competitive pressure from AWS, Microsoft, and Google. Increased reliance on GPU suppliers, ongoing price competition in cloud workloads, and the cannibalization of legacy software revenue may constrain margins during the transition phase.

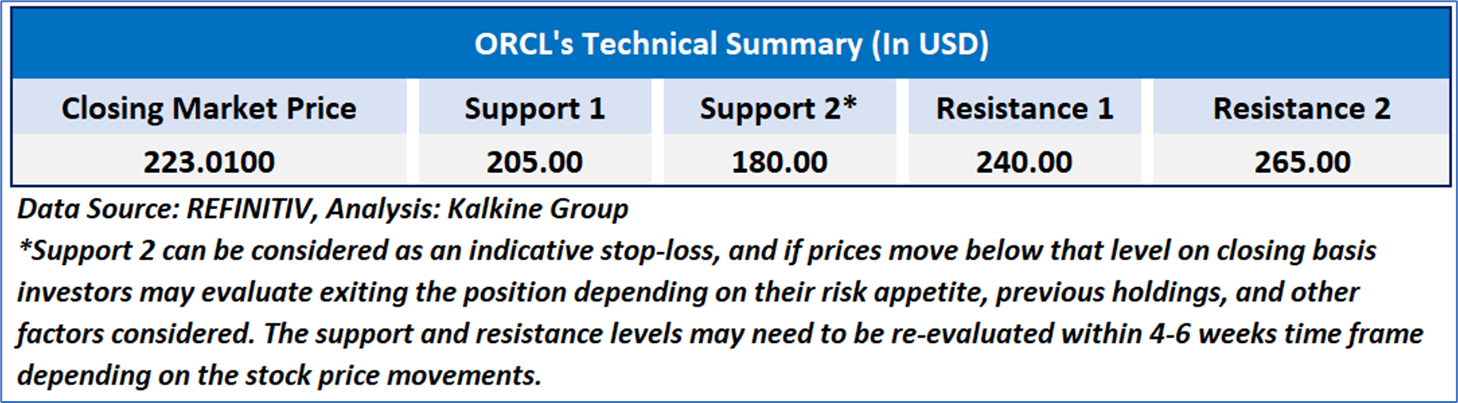

Technical Observation (on the daily chart):

- Trend Structure and Moving Averages: Oracle’s price has begun to stabilize after a prolonged decline, moving back above the 21-day moving average but still trading below the downward-sloping 50-day average. This indicates easing selling pressure but an overall trend that remains corrective, with a decisive close above the 50-day level needed to confirm a stronger recovery.

- Momentum and RSI Assessment: The RSI near 48 shows momentum shifting from bearish to neutral, suggesting downside exhaustion but not yet strong bullish momentum. The gradual improvement is constructive, though a breakout above the 55–60 range would be needed to signal more meaningful buying strength.

- Volume Dynamics and Market Participation: Buying volume has improved during the recent rebound, pointing to growing interest, but sustained accumulation has not yet emerged. A clear increase in volume on moves above key resistance levels would reinforce the recovery, while weak volume on rallies may signal limited conviction and the risk of revisiting support.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective, and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 10, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...