DocuSign Inc (NASDAQ: DOCU)

DocuSign Inc (NASDAQ: DOCU) powers the transformation of agreements. Trusted by over 1.7 million customers and more than a billion users across more than 180 countries, Docusign solutions help streamline business processes and make everyday tasks simpler. Through intelligent agreement management, Docusign unlocks vital business data that would otherwise remain buried within documents.

Positive Growth Aspects

- Solid Financial Growth and Resilient Margins: Docusign demonstrated steady financial progress in the first quarter, with revenue rising 8% year-over-year to USD 763.7 million despite a 0.6% negative impact from foreign currency exchange rates. Subscription revenue, which makes up the majority of the business, grew by 8% to USD 746.2 million, showcasing the strength and stickiness of its core offering. Gross margins remained robust, with GAAP gross margin improving to 79.4% and non-GAAP gross margin increasing to 82.3%, reflecting efficient cost management. The company also reported a significant improvement in GAAP net income per diluted share, rising to USD 0.34 from USD 0.16 year-over-year, while non-GAAP net income per diluted share increased to USD 0.90 from USD 0.82.

- Expanding Platform with AI-Led Innovations: The company is aggressively investing in its Intelligent Agreement Management (IAM) platform, as highlighted during its Momentum25 NYC conference. Docusign introduced Iris, an AI engine that leverages decades of contract data to enhance agreement workflows. The launch of AI Contract Agents and new tools like Agreement Desk, AI-Assisted Review, and Workspaces illustrate Docusign’s ambition to automate and streamline the contract lifecycle. These innovations, coupled with integrations with popular platforms such as Salesforce and Coupa, position Docusign to drive greater value for its customers and deepen ecosystem ties.

- Strong Shareholder Returns and Buyback Flexibility: Docusign continues to return value to shareholders through its stock repurchase program. The company repurchased USD 183.4 million of its common stock during the quarter, up from USD 149.1 million in the prior year. In addition, the board authorized a significant increase to the stock repurchase program, adding up to USD 1.0 billion in potential future repurchases. This move reflects management’s confidence in Docusign’s long-term prospects and its commitment to enhancing shareholder value, while also giving the company flexibility to manage its capital allocation based on evolving market conditions.

Growth Challenges

- Slower Billing Growth and Professional Services Decline: While revenue and subscription income posted solid gains, billing growth slowed to 4% year-over-year, indicating potential softness in future revenue conversion. Additionally, professional services and other revenue declined by 4%, suggesting either reduced demand for ancillary services or pricing pressure. This underperformance in services revenue could impact customer adoption of higher-margin, value-added offerings that are critical for driving platform stickiness and differentiation in a competitive market.

- Cash Flow Moderation Amid High Investment: Docusign’s cash flow metrics showed slight year-over-year declines, with net cash provided by operating activities dropping from USD 254.8 million to USD 251.4 million and free cash flow decreasing from USD 232.1 million to USD 227.8 million. While these declines are modest, they may signal rising costs associated with the company's accelerated investment in AI capabilities and global platform enhancements. Sustained investments will likely be necessary to maintain leadership, but any prolonged cash flow pressure could limit flexibility for further buybacks or strategic acquisitions.

- Dilution Concerns and Increasing Share Count: Although earnings per share improved, the company’s diluted share count rose from 210 million to 213 million year-over-year. Furthermore, the guidance anticipates diluted weighted-average shares outstanding between 210 and 215 million for both the next quarter and fiscal year. This gradual increase in share count could dilute shareholder returns if not offset by continued strong earnings growth and margin expansion. Investors may watch this trend closely, particularly as the company ramps up equity-based compensation to attract and retain top AI and platform talent.

- Uncertain Execution Risks on New Product Rollouts: While Docusign’s AI-driven innovations represent exciting growth opportunities, many of these features, such as Iris, AI Contract Agents, and CLEAR Identity Verification, are slated for launch later this year. The success of these offerings hinges on seamless execution, customer adoption, and integration with existing enterprise workflows. Given the highly competitive and fast-evolving AI landscape, there remains some uncertainty regarding Docusign’s ability to translate these initiatives into meaningful revenue gains and long-term market differentiation. Execution missteps or slower-than-expected adoption could dampen the near-term impact of these strategic bets.

Technical Observation (on the daily chart):

DOCU is exhibiting a bullish momentum, with the price trading above both its 21-day and 50-day moving averages, supported by a recent bullish crossover. The RSI at 63 indicates moderately bullish sentiment without being overbought, and rising volume adds confidence to the upward move.

Docusign delivered a mixed set of first-quarter results, with solid revenue and subscription growth, improved margins, and strong shareholder returns through an expanded stock repurchase program, reflecting confidence in its long-term strategy. The company also showcased promising AI-driven innovations aimed at enhancing its Intelligent Agreement Management platform, which could strengthen its competitive positioning. However, slower billing growth, a decline in professional services revenue, and modest cash flow pressure suggest some near-term operational challenges. Additionally, rising share count and execution risks tied to upcoming AI product launches introduce uncertainty around the sustainability of growth momentum.

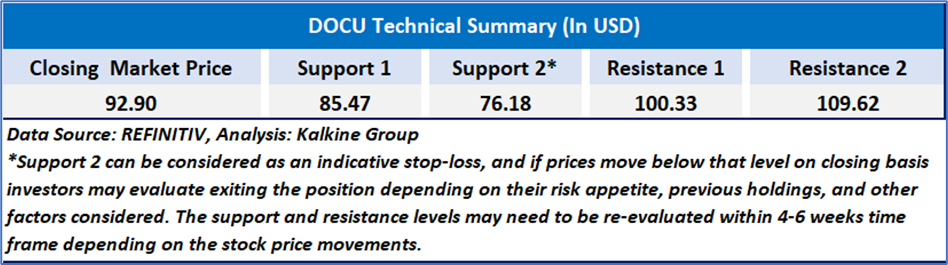

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to DocuSign Inc (NASDAQ: DOCU) at the closing market price of USD 92.90 as of June 05,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is June 05,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...