Celestica Inc. (TSX: CLS): AI Infrastructure Resilience and the 4.5% Surge

Celestica Inc. (TSX: CLS) continues to cement its status as a central nervous system for the artificial intelligence revolution, witnessing a robust 4.5% climb on January 27, 2026. This price action reflects a powerful "buy-the-dip" mentality as market participants brush off recent supply chain speculation and pivot their focus toward the company’s indispensable role in the $2.5 trillion AI infrastructure build-out.

As a dominant provider of high-speed networking switches and custom compute solutions for the world’s largest hyperscalers, Celestica is no longer viewed as a mere contract manufacturer but as a high-margin technology partner. With its Q4 2025 earnings release imminent, today’s surge underscores a market betting on continued operational excellence and a strategic shift that has fundamentally re-rated the company’s long-term earnings trajectory.

Latest Key Reasons and Drivers of the Surge

Source: Kalkine Group

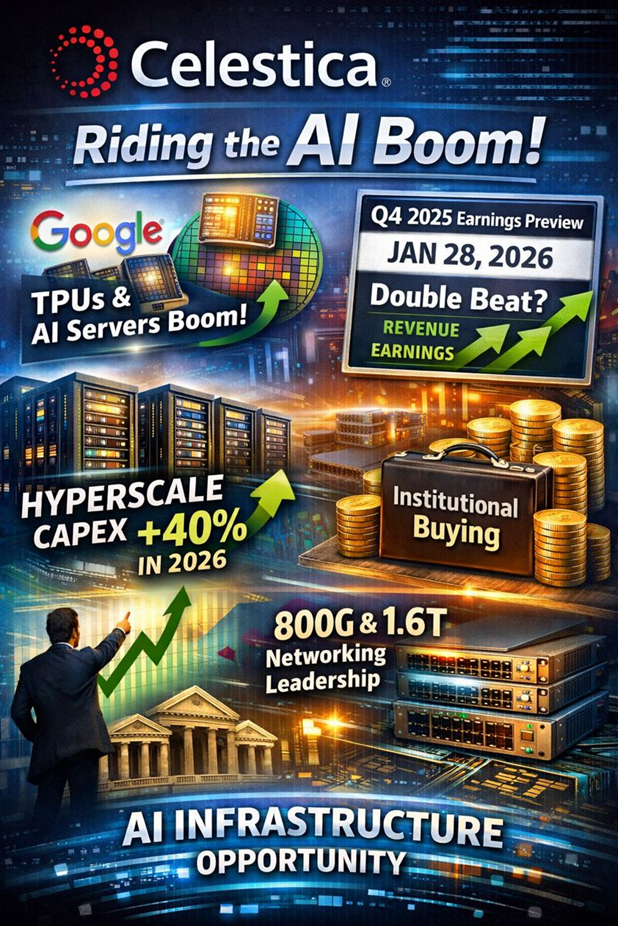

The primary catalyst for the 4.5% gain is a sharp reversal of sentiment following recent rumors regarding supply chain diversification by major clients like Google. Investors have largely concluded that the increasing global demand for Tensor Processing Units (TPUs) and AI servers is a "rising tide" that benefits multiple suppliers rather than a zero-sum game that threatens Celestica’s volume.

- Anticipation of the Q4 2025 financial results (scheduled for release on January 28, 2026) has led to significant "pre-earnings" positioning, with analysts forecasting another potential "double beat" in revenue and earnings per share.

- The continued expansion of global hyperscale capital expenditure, which is projected to grow by 40% in 2026, directly fuels Celestica’s Connectivity & Cloud Solutions (CCS) segment.

- Market enthusiasm for Celestica’s leading position in the 800G and 1.6T networking switch markets remains a massive driver, as these high-performance components carry significantly higher margins than traditional hardware.

- Strong institutional buying has been noted, with major asset managers increasing their stakes to gain exposure to AI infrastructure without the high-valuation premiums seen in the semiconductor sector.

Current Business Model and Operational Focus

Celestica has evolved into a vertically integrated hardware platform solutions provider, moving away from low-margin, high-volume electronics assembly toward complex, technology-intensive systems.

- The company operates through two main pillars: Connectivity & Cloud Solutions (CCS) and Advanced Technology Solutions (ATS).

- The CCS segment is the current growth engine, focusing on data centre infrastructure, high-speed networking, and custom AI/ML compute programs for cloud service providers.

- The ATS segment provides stability and diversification through long-lifecycle markets including Aerospace & Defense, HealthTech, and Industrial Capital Equipment.

- Celestica’s value proposition now centers on its internal design and engineering capabilities, allowing it to co-develop proprietary hardware (Hardware Platform Solutions) with its customers, which creates high switching costs and deeper integration.

Latest Financial and Operational Updates (Source: Celestica Inc.)

In recent official communications, Celestica has outlined a roadmap of aggressive growth and capital efficiency that has redefined its financial profile.

- Management has projected 2026 revenue of approximately $16.0 billion, representing a 31% increase over the 2025 outlook (Source: Celestica Q3 2025 Financial Results).

- Adjusted earnings per share (EPS) for 2026 are anticipated to reach $8.20, a projected 39% year-over-year increase, signaling significant operating leverage (Source: Celestica Q3 2025 Financial Results).

- Operational updates highlight the introduction of the SD6300 ultra-dense storage platform and the DS6000/DS6001 series of 1.6TbE data centre switches to support next-generation AI clusters (Source: Celestica Press Release, Nov 2025/Jan 2026).

- Regarding dividends, Celestica currently does not pay a regular cash dividend, opting instead to reinvest capital into high-growth R&D and its Normal Course Issuer Bid (NCIB) to repurchase shares (Source: Celestica Investor Relations).

Latest SWOT Analysis

Source: Kalkine Group

Strengths

- Dominant market share (over 50%) in custom Ethernet switches for AI data centres.

- Strong, multi-year relationships with "Big Tech" hyperscalers.

- Advanced engineering and design capabilities that differentiate it from traditional EMS competitors.

- Resilient balance sheet with significant free cash flow generation.

Weaknesses

- High customer concentration, with a small group of hyperscalers accounting for a large percentage of revenue.

- Operating margins, while expanding, remain lower than pure-play networking software or chip companies.

- Sensitivity to short-term changes in capital expenditure plans from top-tier cloud providers.

Opportunities

- The transition to 1.6T networking technology represents a significant hardware refresh cycle.

- Expansion of manufacturing capacity in North America and Mexico to meet "near-shoring" demand.

- Potential for M&A to further bolster its "Hardware Platform Solutions" portfolio.

- Accelerating demand for sovereign AI infrastructure as nations build independent data capabilities.

Threats

- Intense competition from other major manufacturing services firms like Jabil and Flex.

- Geopolitical tensions affecting global supply chains and raw material costs.

- Potential "AI exhaustion" where hyperscalers might temporarily slow their infrastructure spend to digest current capacity.

Outlook and Risks

The outlook for Celestica remains tied to the velocity of the AI infrastructure build-out. For 2026, the company is positioned to benefit from a "super-cycle" in data centre networking upgrades. Management’s confidence is reflected in their upwardly revised guidance, which suggests that the demand for high-performance computing is outstripping current supply capacity.

However, risks persist. The primary concern for the upcoming year is the "priced for perfection" valuation; any slight miss in earnings or a downward revision in guidance could lead to heightened volatility. Additionally, while the company’s vertical integration helps, it is not immune to global semiconductor shortages or logistics disruptions that could delay the delivery of high-value programs.

Conclusion

Celestica’s 4.5% surge on January 27, 2026, is a testament to the market's conviction in the long-term AI infrastructure narrative. By successfully pivoting from a traditional contract manufacturer to a sophisticated technology partner for the world’s cloud giants, Celestica has positioned itself at the epicenter of the most significant technological shift of the decade. While customer concentration and valuation remains points of scrutiny, the company’s consistent ability to exceed financial targets and innovate in the high-speed networking space makes it a cornerstone player in the evolving digital landscape.

Please wait processing your request...

Please wait processing your request...