While the broader market remains fixated on the cooling AI narrative in the United States, the world's most sophisticated institutional players—from BlackRock to Franklin Templeton—are quietly shifting their gaze northward. For the first time in years, the TSX is being framed not as a stagnant commodity play, but as a "strategic hedge" offering massive intrinsic discounts.

Top-tier investment banks like Desjardins Capital Markets and Scotiabank are signaling that the Canadian market enters 2026 with a more balanced foundation than its Southern counterparts. "Smart money" is currently rotating out of overextended U.S. mega-caps and into high-conviction Canadian growth names that are trading at steep discounts to their fair value.

As we move further into the 2026 easing cycle, these three specific stocks stand out for their explosive combination of institutional backing, operational momentum, and significant valuation upside.

Source: Kalkine Group

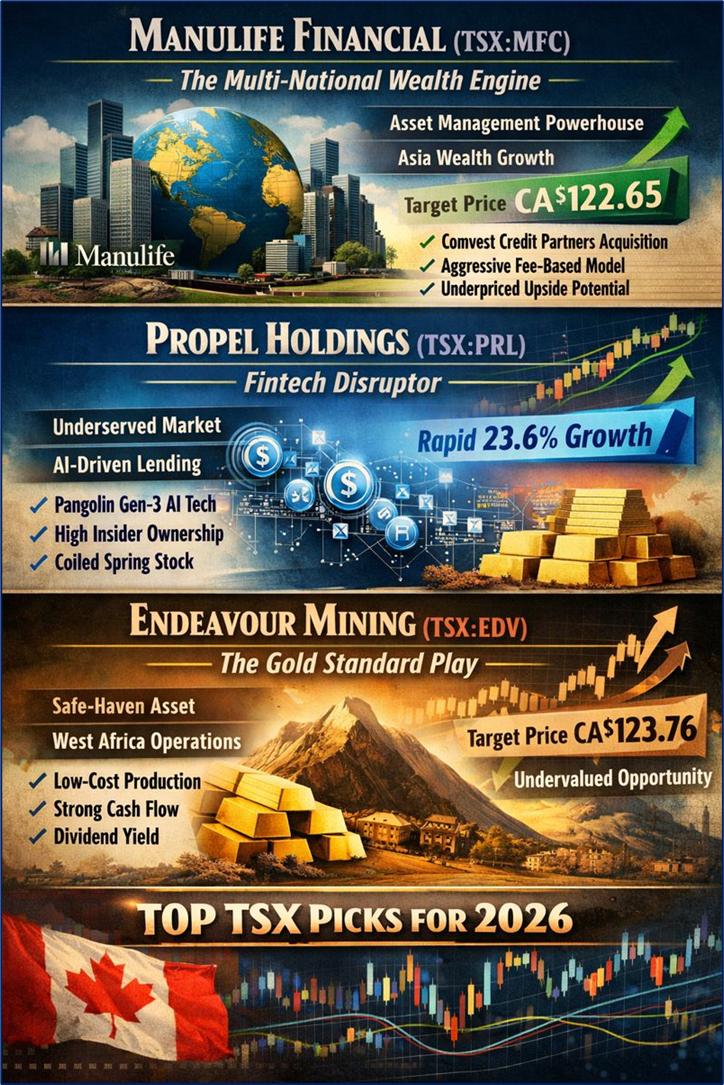

Manulife Financial (TSX:MFC) | The Multi-National Wealth Engine

The narrative surrounding Manulife Financial has undergone a radical transformation in early 2026. Long viewed as a traditional insurer, "smart money" managers now view it as a high-growth wealth and asset management powerhouse. Recent data shows a surge in institutional interest following a high-profile analyst upgrade that highlighted the company's aggressive pivot toward capital-light, fee-based revenue streams.

Key Drivers and Business Model The catalyst for the latest rerating is the successful integration of Comvest Credit Partners, which has significantly scaled Manulife’s private markets platform. This move allows the company to leverage its massive global distribution network—particularly in Asia's rapidly expanding wealth pools—to drive stable, high-margin income. Unlike the capital-intensive insurance models of the past, this "new" Manulife is built on recurring fees and private credit capabilities.

Technical Analysis and Analysts' Take Technically, MFC has displayed a "golden cross" on the weekly charts, supported by a 13.52% return over the last 90 days. Analysts at Simply Wall St and major Canadian brokerages note that despite the recent run, the stock remains fundamentally undervalued. Current consensus points to an intrinsic value near CA$122.65, representing a staggering potential upside from its current trading range around the CA$51 mark.

Financial Updates and Dividend Manulife continues to be a favorite for income-growth seekers, maintaining its reputation for aggressive capital returns. The latest financial updates show a strengthening of its core Asia division, which now contributes a larger share of core earnings than ever before. With a healthy dividend yield that remains well-covered by growing cash flows, it serves as both a growth play and a defensive anchor.

Outlook and Risks The 2026 outlook is bullish, predicated on continued wealth expansion in emerging markets. However, the primary risks include geopolitical volatility in the Asian corridors and potential regulatory shifts in private credit markets. Despite these, the "smart money" consensus is that the market has yet to fully price in the company's shift toward becoming a global asset management titan.

Propel Holdings (TSX:PRL) | The Fintech Disruptor Winning the "Underserved" Market

In the high-stakes world of Canadian fintech, Propel Holdings has emerged as a top pick for hedge funds looking for high-alpha growth. Unlike traditional lenders, Propel utilizes a proprietary AI-powered platform to serve consumers who are often overlooked by the "Big Five" banks. This specialized focus has allowed them to maintain rapid growth without the typical overhead of legacy institutions.

Key Drivers and Strategic Growth The primary driver for Propel in 2026 is its aggressive expansion into underserved markets through strategic partnerships. Institutional investors are particularly attracted to the company’s high insider ownership (nearly 30%), which aligns management's interests directly with shareholders. The company is currently forecasted to grow its revenue by 23.6% annually, significantly outperforming the broader Canadian financial sector.

Current Valuation and Technicals Propel is currently flagged by quantitative analysts as one of the most undervalued stocks based on future cash flows. With a market cap hovering around CA$967 million, it is seen as a "coiled spring." Technical indicators show a steady accumulation phase, with price action consolidating above key moving averages as the market prepares for the next leg of its growth cycle.

Latest Operational Updates and Dividend Recent earnings reports highlight a record-breaking loan origination volume, fueled by the Pangolin Gen-3 AI enhancements in their underwriting process. While growth is the priority, Propel has managed to maintain a sustainable dividend policy, a rarity for fintechs in this growth stage. This "growth-plus-yield" profile is a key reason why it's appearing on more institutional "Buy" lists this month.

Outlook and Risks The outlook for 2026 remains highly optimistic as the company scales its U.S. and Canadian operations. The main risk involves a potential spike in consumer default rates if the macroeconomic environment sours; however, Propel’s AI models have so far proven resilient in predicting and mitigating credit risk better than traditional competitors.

Endeavour Mining (TSX:EDV) | The "Gold Standard" Growth Play

As geopolitical tensions in 2026 continue to drive investors toward safe-haven assets, Endeavour Mining has become the preferred choice for global fund managers seeking exposure to the gold rally. Analysts from Vanguard and Morningstar have highlighted the materials sector as a primary driver for the TSX this year, with Endeavour sitting at the top of the "undervalued" list.

Key Drivers and Valuation Endeavour is currently trading at a significant discount to its estimated fair value of CA$123.76. The "smart money" thesis is simple: the market is currently pricing in the risks of operating in West Africa while ignoring the company’s world-class production costs and massive cash flow generation. Its earnings are expected to grow by over 35% annually, a rate that dwarfs the average Canadian market growth of 11.6%.

Technical Analysis and Institutional Stance Technically, the stock is testing major resistance levels as gold prices hover near record highs. Institutional ownership remains high, with "big guns" like BlackRock maintaining sizable positions. Analysts note that any breakout in the gold price could trigger a rapid rerating of EDV shares, as it remains one of the few high-growth miners with a disciplined capital allocation strategy.

Financial and Operational Updates The latest operational updates confirm that Endeavour is on track to hit the upper end of its production guidance while simultaneously reducing its debt. The company’s latest dividend update remains attractive, providing a yield that serves as a "paid-to-wait" incentive for investors while the valuation gap closes.

Conclusion and Outlook The conclusion among elite analysts is that the TSX is currently a "mispriced" market full of opportunities for those willing to look past the U.S. tech bubble. Whether it’s the wealth management pivot of Manulife, the AI-driven lending of Propel, or the undervalued gold production of Endeavour, these stocks represent the pinnacle of current Canadian growth opportunities.

Please wait processing your request...

Please wait processing your request...