For an investor starting with a capital of CAD 25,000, targeting a consistent 6% annual yield generates approximately CAD 1,500 in annual passive income. On a monthly basis, this translates to roughly CAD 125. While this may seem modest, smart money managers emphasize that when these dividends are reinvested or held within tax-advantaged accounts like a TFSA, the compounding effect on a mid-to-high yield portfolio can significantly accelerate long-term wealth.

Source: Kalkine Group

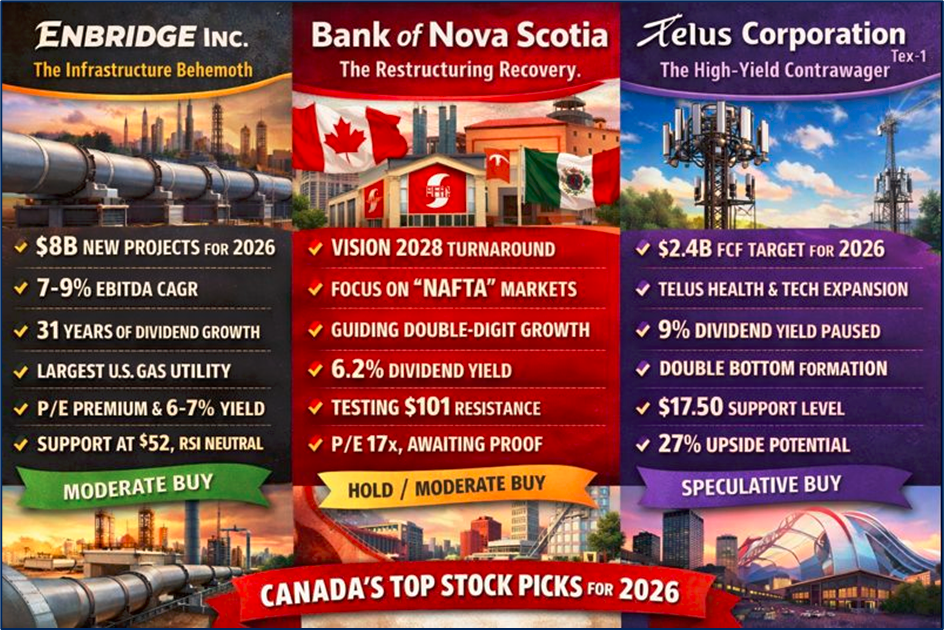

Enbridge Inc. (TSX: ENB): The Infrastructure Behemoth

- Latest Financial & Operational Updates: Enbridge entered 2026 with a massive $8 billion in new projects coming into service. The company recently reaffirmed its 2023–2026 compound annual growth rate (CAGR) of 7-9% for EBITDA. Management has successfully integrated recent U.S. gas utility acquisitions, making it the largest natural gas utility franchise in North America.

- Latest Business Model: Transitioning from a pure-play oil pipeline operator to a diversified energy infrastructure giant. Its cash flow is now 98% underpinned by long-term, cost-of-service, or take-or-pay contracts, insulating it from commodity price volatility.

- Latest Dividend & Valuation: Enbridge announced a 3% dividend increase for 2026, marking its 31st consecutive year of raises. The annualized dividend sits at $3.88 per share. Analysts view the current P/E ratio as trading at a slight premium to historical averages, but the 6% to 7% yield remains a primary draw for "smart money."

- Technical Analysis: The stock has shown strong support levels near $52.00. Throughout early 2026, it has trended above its 200-day moving average, signaling a bullish consolidation phase. Relative Strength Index (RSI) levels suggest the stock is neither overbought nor oversold, providing a stable entry point for income seekers.

- Latest Analyst Consensus: Moderate Buy. Recent upgrades from firms like CIBC and RBC Capital reflect confidence in the "low-risk" commercial framework.

- Risks: High debt-to-EBITDA levels (targeted at 4.5x–5.0x) and sensitivity to long-term interest rate fluctuations remain the primary concerns for institutional bears.

Bank of Nova Scotia (TSX: BNS): The Restructuring Recovery

- Latest Financial & Operational Updates: Scotiabank is currently undergoing a "Vision 2028" restructuring. For fiscal 2026, CEO Scott Thomson has guided for double-digit net income growth in the Canadian banking segment. The bank is pivoting away from high-risk Central American markets to focus on the "NAFTA corridor" (Canada, USA, Mexico).

- Latest Business Model: Shifting from geographic expansion to "capital velocity." The bank is prioritizing high-ROE (Return on Equity) activities, specifically focusing on its primary client base in Canada and increasing its presence in the U.S. wealth management sector.

- Latest Dividend & Valuation: Currently yielding approximately 6.2%. While the payout ratio is higher than its Big Five peers, the bank’s commitment to its dividend remains a core pillar of its "momentum" story. Valuation-wise, it trades at a P/E of roughly 17x, which some analysts consider "rich" compared to historical levels, but justified by the 2026 growth outlook.

- Technical Analysis: BNS has experienced a significant 90-day rally of nearly 14%. The stock is currently testing resistance at the $101.00 mark. A break above this level, supported by high volume, could signal a long-term trend reversal from its multi-year laggard status.

- Latest Analyst Consensus: Hold to Moderate Buy. Analysts are cautiously optimistic about the restructuring but wait for concrete evidence of improved credit loss provisions in the Mexican retail segment.

- Risks: Exposure to Latin American credit cycles and a potential slowdown in the Canadian mortgage market due to "higher-for-longer" mortgage resets.

Telus Corporation (TSX: T): The High-Yield Contrawager

- Latest Financial & Operational Updates: Telus is targeting a significant free cash flow (FCF) increase to $2.4 billion in 2026. After a period of heavy capital expenditure on its PureFibre network, the company is now entering a "harvesting" phase where spending decreases and cash generation rises.

- Latest Business Model: Beyond traditional telecom, Telus has diversified into Telus Health, Telus Agriculture, and AI-driven customer experience (Telus Digital). This "tech-co" approach distinguishes it from BCE or Rogers.

- Latest Dividend & Valuation: In a strategic move to strengthen the balance sheet, Telus recently paused its aggressive dividend growth, maintaining a quarterly payout of $0.4184. This has pushed the trailing yield to an eye-popping 9%, reflecting a significant share price drawdown. Analysts estimate a 27% upside to fair value if the company meets its 2026 debt reduction targets.

- Technical Analysis: The stock has been in a long-term downtrend, losing nearly 50% from all-time highs. However, early 2026 charts show a "double bottom" formation, a classic bullish reversal signal. If the stock holds above $17.50, technical analysts see a path back to the $22.00 range.

- Latest Analyst Consensus: Buy/Speculative Buy. Institutional brokers highlight that while the debt is high, the "dividend freeze" is a prudent move that paves the way for a multi-year recovery.

- Risks: Intense price competition in the Canadian wireless space and a leverage ratio currently sitting at 3.5x, which the company aims to trim to 3.3x by year-end.

Conclusion: Navigating the 6% Yield Landscape

Generating a 6% yield on the TSX in 2026 requires a balance between "Steady Eddies" like Enbridge and "Turnaround Plays" like Telus or Scotiabank. Fund managers are currently favoring companies with "contract-backed" cash flows that can withstand a potential 2026 economic slowdown. By diversifying $25,000 across these sectors—Energy Infrastructure, Financials, and Telecommunications—investors can build a resilient income stream. However, the recurring theme among "Smart Money" is a preference for quality over pure yield; a 9% yield like Telus’s carries higher volatility risk than a 6% yield from a stabilized utility.

Please wait processing your request...

Please wait processing your request...