The Great Valuation Arb: Why Global Fund Managers are Pivoting to Canada

While the S&P 500 grapples with overextended "Mag 7" valuations and a 21x forward P/E, the smart money is crossing the border. Institutional heavyweights like J.P. Morgan, BlackRock, and BMO Capital Markets are flagging the TSX as a premier "Value Haven."

As of January 2026, the S&P/TSX Composite trades at a significant discount to its U.S. counterparts, offering a diversified hedge against AI-related tech volatility. Hedge funds are currently rotating into "Old Economy" sectors—energy infrastructure, materials, and undervalued financials—where stable cash flows and high dividend yields provide a safety net in a "higher-for-longer" interest rate environment.

Source: Kalkine Group

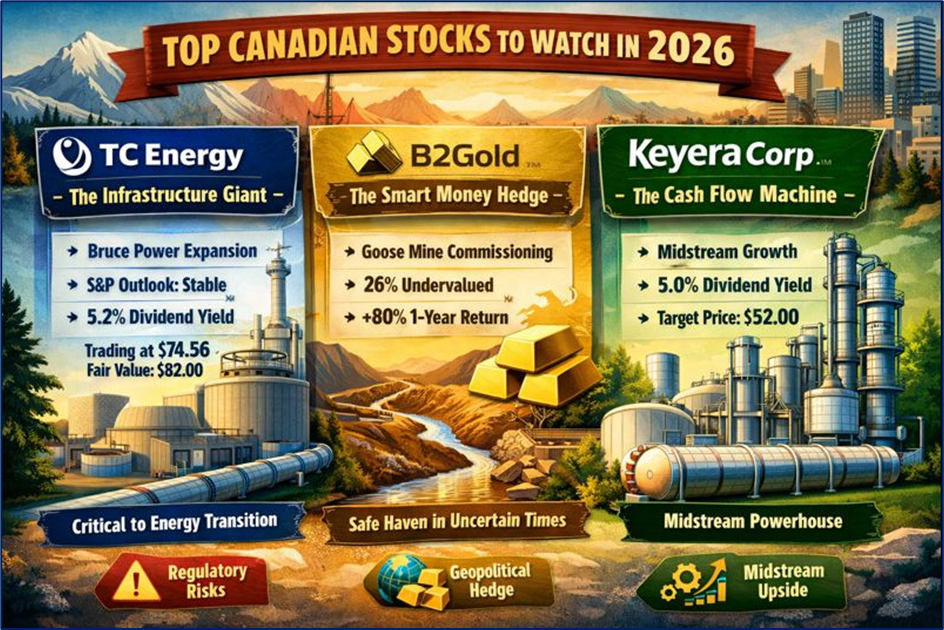

TC Energy (TSX: TRP) – The Infrastructure Giant Hiding in Plain Sight

Latest Business Model & Drivers: TC Energy has successfully pivoted to a "low-risk infrastructure" model, focusing on regulated assets that generate predictable, inflation-linked cash flows. The primary driver for 2026 is the Bruce Power nuclear expansion in Ontario, which analysts at BMO describe as "highly underappreciated." This shift toward clean, baseload power complements their massive natural gas footprint, positioning them as a critical player in the North American energy transition.

- Latest Valuation: Trading near $74.56, with institutional "Fair Value" estimates sitting closer to $79.00 - $82.00.

- Dividend & Yield: A robust 5.2% yield, backed by a 24-year streak of annual increases.

- Latest Financial Update: S&P Global recently upgraded their outlook to "Stable" from "Negative," citing superior capital discipline and a $21 billion secured growth program.

- Technical Analysis: The stock has established a "Golden Cross" on the daily charts, with the 50-day moving average trending firmly above the 200-day. Current RSI (Relative Strength Index) is at 58, suggesting there is still room for upward momentum before reaching overbought territory.

- Analysts Upgrade/Downgrade: Maintained as a "Top Pick" by BMO Capital Markets in January 2026; price targets recently nudged higher across the street due to the Bruce Power equity income projections (expected to hit $1.2B by 2030).

- Risks: Regulatory delays in new pipeline egress and sensitivity to sudden shifts in the Bank of Canada’s easing cycle.

B2Gold (TSX: BTO) – The "Smart Money" Hedge Against Geopolitical Chaos

Latest Business Model & Drivers: As gold surges as a safe-haven asset, B2Gold stands out for its high-margin production profile. The key driver for 2026 is the Goose Mine commissioning, which is set to significantly boost annual output and lower all-in sustaining costs (AISC). Unlike many junior miners, B2Gold operates with a fortress balance sheet, a rarity that has attracted significant "smart money" inflows this month.

- Latest Valuation: Simply Wall St and various hedge fund models tag BTO as 26% undervalued, with a fair value estimate of $8.60 vs. the current price of $6.36.

- Dividend & Yield: Offers one of the most attractive yields in the mining sector at approximately 4% (variable based on gold price).

- Latest Financial Update: Reported 1-year total shareholder returns of over 80%, yet still trades at a discount to its net asset value (NAV) due to its geographic exposure in Mali, which is now stabilizing.

- Technical Analysis: Volume surged on January 9, 2026, breaking a long-term resistance level at $6.10. The stock is currently consolidating above this new support, forming a "Bull Flag" pattern that often precedes a breakout.

- Analysts Upgrade/Downgrade: Re-iterated "Outperform" by multiple boutiques following fresh data on the Gramalote development study.

- Risks: Jurisdictional risk in West Africa and potential fluctuations in the spot price of gold.

Keyera Corp (TSX: KEY) – The Cash Flow Machine Analysts Are Obsessing Over

Latest Business Model & Drivers: Keyera is no longer just a "pipeline company." It has evolved into a fully integrated midstream powerhouse. The driver for 2026 is the full utilization of its fractionation capacity expansion, which has allowed the company to lock in long-term contracts for over 100,000 barrels per day. This provides a 7-8% EBITDA growth floor through 2027.

- Latest Valuation: Currently trading at $43.12, but institutional consensus points to a $52.00 target, representing 17% immediate upside.

- Dividend & Yield: A highly sustainable 5.0% yield with a low payout ratio relative to its fee-based cash flows.

- Latest Financial Update: Despite missing some revenue targets in Q3 2025, the company’s fee-based earnings (the most stable part of the business) reached record highs, attracting defensive-minded fund managers.

- Technical Analysis: The stock is currently trading in a well-defined ascending channel. It recently bounced off the lower support line at $42.50, and the MACD (Moving Average Convergence Divergence) has just flipped positive, indicating a new buying cycle.

- Analysts Upgrade/Downgrade: Raymond James recently signaled a "hold" for short-term traders after a 26% rally, but long-term value desks at RBC and BMO remain bullish, citing the "Plains NGL" acquisition as a game-changer.

- Risks: Integration risks with the recent Plains NGL acquisition and potential for a slowdown in Western Canadian production volumes.

Conclusion: The 2026 Value Rotation is Real

The era of "growth at any price" has stalled. In 2026, the biggest global fund managers are rewarding predictable cash flow, dividend sustainability, and tangible assets. The TSX offers a unique intersection of these factors, especially in companies like TC Energy, B2Gold, and Keyera. While the "Mag 7" remains the headline act in the U.S., the real "Alpha" for the coming year is being found in the undervalued, high-yielding corners of the Canadian market.

Please wait processing your request...

Please wait processing your request...