If you were watching the TSX industrial sector on Friday, December 5, you likely saw Aecon Group Inc. (TSX: ARE) suddenly light up the boards. The stock surged 4.93% to close near CAD 29.82, breaking through key resistance levels and outpacing the broader market.

For retail investors, moves like this often beg the question: Is this a one-day wonder, or the start of a sustained rally? Here is the analytical breakdown of the surge, the business engine driving it, and what lies ahead for Canada’s construction titan.

- The Friday Surge: What Happened?

The 5% jump wasn't triggered by a single "breaking news" press release dropped on Friday morning. Instead, it was a perfect storm of technical validation and sector rotation.

- Technical Breakout: The stock had been consolidating. Friday's move pushed it past the psychological CAD 29.00 resistance. Technical analysts upgraded the stock as momentum indicators flipped positive.

- The "Execution" Premium: Investors are reacting to the successful delivery of major projects. On the heels of the surge, Aecon celebrated the opening of the Finch West LRT (Light Rail Transit) in Toronto. Successful delivery of complex transit projects de-risks the stock in the eyes of institutional money.

- Sector Tailwinds: Money is rotating out of volatile tech and into "real assets." With the global push for nuclear energy and data centre infrastructure, Aecon is being repriced not just as a construction firm, but as a critical energy transition play.

- The Engine: Business Model & Strategy

Aecon isn't just pouring concrete for driveways. They operate a sophisticated, dual-engine business model that is currently undergoing a massive strategic pivot.

The Old Model vs. The New Model

- Old Strategy (The "Risk" Era): Bidding low on massive "Fixed Price" contracts. If costs went up (inflation/delays), Aecon ate the loss. This plagued them for years.

- New Strategy (The "Alliance" Era): Focusing on Collaborative Contracts (Progressive Design-Build). In this model, risks are shared with the government or client. Inflation goes up? The contract value adjusts. This protects margins.

Source: Kalkine Group

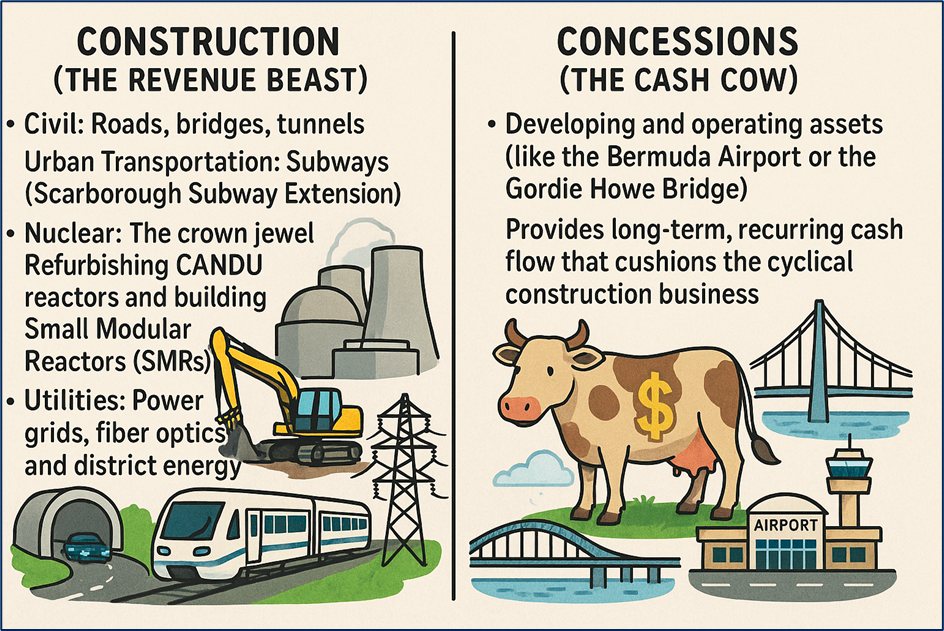

The Segments:

- Construction (The Revenue Beast):

- Civil: Roads, bridges, tunnels.

- Urban Transportation: Subways (Scarborough Subway Extension), LRTs.

- Nuclear: This is the crown jewel. Refurbishing CANDU reactors and building Small Modular Reactors (SMRs).

- Utilities: Power grids, fiber optics, and district energy.

- Concessions (The Cash Cow):

- Developing and operating assets (like the Bermuda Airport or the Gordie Howe Bridge). This provides long-term, recurring cash flow that cushions the cyclical construction business.

Source: Kalkine Group

- The Catalysts

- The "Nuclear" Supercycle Aecon is arguably the best way to play the nuclear renaissance in Canada.

- Fact: They are executing the massive Darlington Refurbishment (on time/budget).

- Growth: They are the deployment partner for the BWRX-300 Small Modular Reactor (SMR)—the first grid-scale SMR in the Western world. As the world demands clean baseload power for AI data centers, Aecon’s nuclear expertise is a wide moat.

- The Record Backlog

- Backlog: Hit a record $10.8 Billion in Q3 2025.

- Revenue Growth: Revenue was up 20% year-over-year.

- Implication: They have enough work secured to keep the lights on and dividends flowing for years, regardless of a short-term recession.

- The Valuation Gap Despite the Friday surge, Aecon trades at a valuation discount compared to U.S. peers (like Emcor or Quanta Services). As they prove they can shed the "risky construction" label, this multiple expansion could drive the stock price higher.

- Know the Risks

It’s not all blue skies. Construction is a notoriously difficult business.

- Legacy Projects: Aecon is still working through a few remaining "Fixed Price" legacy projects (like the Eglinton Crosstown LRT). These are profit-drains. Until these are fully off the books, they remain a drag on earnings.

- Labour Shortage: You can have $10B in contracts, but if you can't find skilled welders and engineers to build them, execution suffers.

- Interest Rates: While rates are stabilizing, high borrowing costs can slow down private clients (commercial developers) from greenlighting new projects.

- Outlook 2026: The "Infrastructure Supercycle"

The outlook remains Bullish.

- Pipeline: Management sees a $100 Billion pursuit pipeline of projects across Canada.

- Data Centres: The explosion of AI requires massive power infrastructure. Aecon’s acquisition of high-voltage contractors positions them to build the grid upgrades these data centres need.

- Guidance: Expect margins to slowly improve as the high-margin "Collaborative" work replaces the low-margin "Fixed Price" work in the backlog.

Conclusion: The Sleeping Giant Wakes Up

Friday’s 5% surge was a wake-up call. Investors are realizing that Aecon has successfully navigated its turnaround. It has transitioned from a risky bidder to a strategic partner in Canada’s energy and transit future.

With a 2.5%+ dividend yield, a record backlog, and a foothold in the explosive nuclear sector, Aecon is positioning itself as a "buy-and-hold" infrastructure staple rather than a speculative trade.

Source: Trading View, 5 December 2025

Please wait processing your request...

Please wait processing your request...