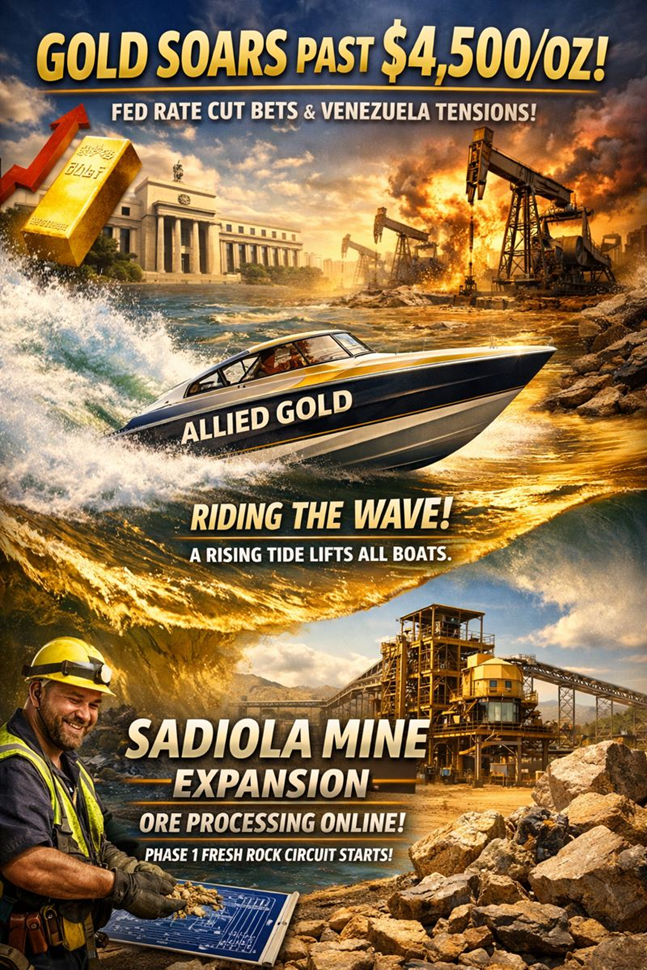

1. The Catalyst: Why Allied Gold Popped ~6% on Dec 22, 2025

On December 22, 2025, Allied Gold Corp (TSX: AAUC) surged approximately 6%, hitting an all-time high of roughly CAD 34.36. This move wasn't random volatility; it was a textbook "double-engine" breakout fueled by macro tailwinds and company-specific execution.

Source: Kalkine Group

- Macro Driver (The Tide): Gold prices shattered records, crossing $4,500 per ounce on Dec 22, driven by aggressive Federal Reserve rate cut bets and escalating geopolitical tensions (specifically focusing on Venezuela). A rising tide lifts all boats, but Allied’s leverage to the gold price made it a speedboat in this rally.

- Micro Driver (The Engine): Crucially, the company announced the start of ore processing at its Sadiola Mine’s Phase 1 expansion in Mali. This de-risks their biggest asset, confirming that the new "fresh rock" processing circuit is online.

2. Deep Dive: The "Fresh Rock" Game Changer at Sadiola

The market loves execution, and Allied delivered. The Sadiola news is the primary fundamental driver for the stock's re-rating.

- The Problem: Previously, Sadiola was processing mostly oxide ore (softer, lower grade) and limited amounts of hard fresh rock.

- The Fix: The newly commissioned comminution circuit allows the mine to increase the fresh ore feed from ~20% to ~60%.

- The Impact: This shift unlocks higher-grade material, targeting annual production of 200,000–230,000 ounces starting in 2026. This transforms Sadiola from a steady producer into a growth engine.

3. SWOT Analysis (Deconstructed)

Forget the standard spreadsheet. Here is the strategic reality of Allied Gold right now.

Source: Kalkine Group

Strengths (The Moat)

- Execution Credibility: Delivering Sadiola Phase 1 on time is a massive confidence booster for management.

- Cash Cow Operations: Adjusted EBITDA of nearly $110 million in Q3 2025 proves the assets (Bonikro, Agbaou, Sadiola) are generating serious cash even before the full expansion kicks in.

- Leverage: With unhedged exposure, every $100 rise in gold price flows almost directly to their bottom line.

Weaknesses (The Drag)

- Geographic Concentration: 100% of production comes from Africa (Mali, Côte d'Ivoire, Ethiopia). This creates a "jurisdictional discount" compared to North American peers.

- High AISC (Historically): Costs have been elevated ($2,092/oz in Q3), though they are trending down as production ramps up.

Opportunities (The Upside)

- The Kurmuk Wildcard: The Kurmuk project in Ethiopia is on track for mid-2026 first gold. This is a Tier-1 asset in the making that could push total production toward 800,000 oz/year.

- Margin Expansion: As Sadiola processes higher-grade fresh ore, the cost per ounce should drop, widening margins significantly—especially with gold at $4,400+.

Threats (The Risks)

- The "Mali Factor": Political instability in Mali remains the single biggest overhang. While operations have been unaffected so far, headline risk is constant.

- Cost Inflation: Rising oil prices and input costs could eat into the windfall from record gold prices.

4. Latest Financial & Operational Pulse (Q4 2025)

- Q4 Production Guidance: Allied expects a monster Q4, forecasting over 113,000 ounces (a ~30% jump vs. previous quarters).

- Full Year 2025: On track to exceed guidance of 375,000 ounces.

- Cash Position: Ended Q3 with ~$262 million in cash. With the recent equity raise and surging gold prices, their balance sheet is fortified to fund the Kurmuk build without excessive dilution.

5. The Business Model: "The African Optimizer"

Allied Gold isn’t just an explorer; it’s an optimizer. Their model relies on acquiring under-capitalized assets (like Sadiola from IAMGOLD/AngloGold) and injecting capital to extend mine life and boost efficiency.

- Phase 1 (Current): Optimize current cash flows (Bonikro/Agbaou) and fix Sadiola.

- Phase 2 (2026+): Bring Kurmuk online to become a senior producer.

- Phase 3 (Long-term): Sadiola Phase 2 expansion for massive scale.

6. Critical Risks to Watch

- Jurisdictional Volatility: Investors must be comfortable with West/East African political risk.

- Project Delays: Any slip in the Kurmuk timeline (mid-2026) would be punished severely by the market.

- Gold Price Correction: The stock is currently priced for perfection in gold. A sharp drop below $3,500 would trigger a sell-off.

Conclusion: A Breakout Year Ahead?

Allied Gold’s ~6% rise on December 22, 2025, signals that the market is finally giving them credit for their turnaround strategy. They are successfully transitioning from "fixer-upper" to "growth issuer." With gold at historic highs and their biggest operational bottleneck (Sadiola fresh rock) solved, Allied is positioned for a potentially explosive 2026—provided the geopolitical landscape in their host countries remains stable.

Source: Trading View, 22 December 2025

Please wait processing your request...

Please wait processing your request...