Key Reasons & Drivers Behind the Surge

The recent 9% jump in Almonty Industries' stock price on the TSX is primarily driven by major capital raises and significant project advancements, positioning the company as a leader in the non-China tungsten supply chain.

Strategic Financing Success

The most immediate driver is the successful closing of a large public offering of common shares in the United States:

- Upsized Offering: Almonty successfully closed an upsized underwritten public offering, generating gross proceeds of US$129.375 million.

- Capitalization: This capital infusion significantly strengthens the balance sheet and fully capitalizes the company to execute its key development and expansion projects.

- Signal of Confidence: The success and upsized nature of the offering indicate strong investor confidence in the company's long-term strategy and asset base. The voluntary withdrawal of its base shelf prospectus following the offering suggests no further immediate capital raises are planned under that facility, reducing future dilution uncertainty.

Flagship Mine Progress

Positive news surrounding their key asset:

- Sangdong Mine Commissioning: The flagship Sangdong Tungsten Mine in South Korea is on track for initial production in the second half of 2025. This project is historically one of the world's largest and highest-grade tungsten deposits and is expected to eventually supply over 80% of global non-China tungsten production upon reaching full capacity.

- Critical Mineral Status: Progress at Sangdong directly addresses critical supply vulnerabilities for Western allies, making it a strategically important project amidst geopolitical tensions.

US Expansion and Defense Ties

- New US Project: The recent acquisition and advancement of the Gentung Browns Lake Tungsten Project in Montana is a significant step toward Almonty's goal of becoming a leading integrated U.S. tungsten producer.

- Defense Supply Chain: The company has highlighted its strategic alignment with Western allies' need for secure, non-Chinese tungsten sources, a critical metal for defense (armor, munitions) and advanced technology (electronics, semiconductors). This alignment is underscored by an offtake agreement to supply tungsten oxide for U.S. defense applications and participation in a U.S. Defense Department-backed critical minerals forum.

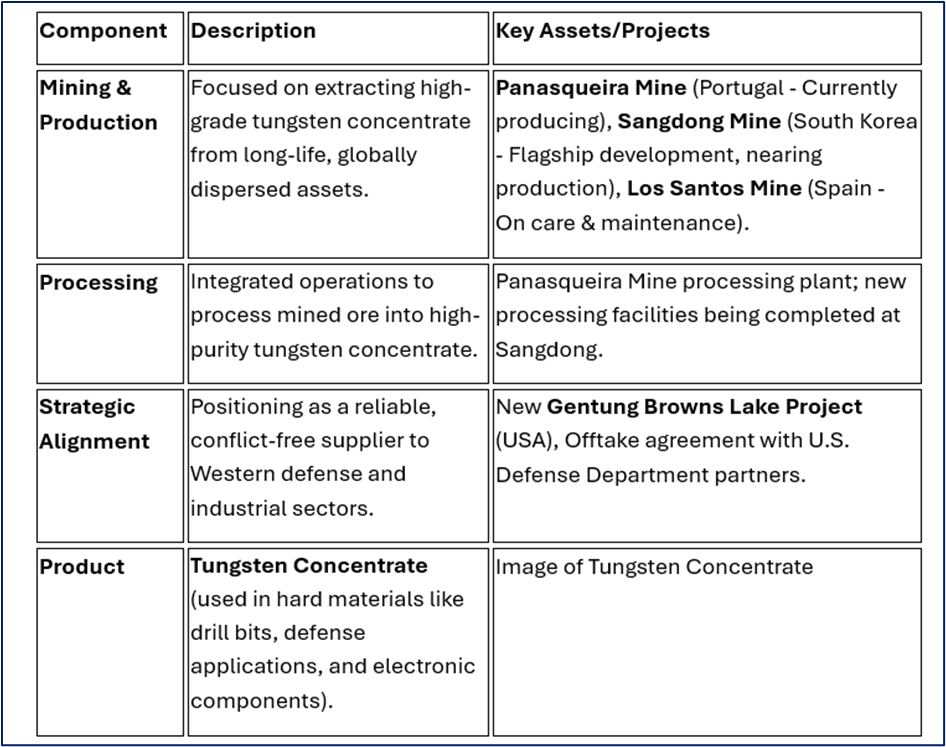

Business Model: The Non-China Tungsten Powerhouse

Almonty Industries is a vertically integrated tungsten concentrate producer focused on becoming the largest non-China source of the strategic mineral.

Source: Company Data

Latest Business Updates (Dec 2025)

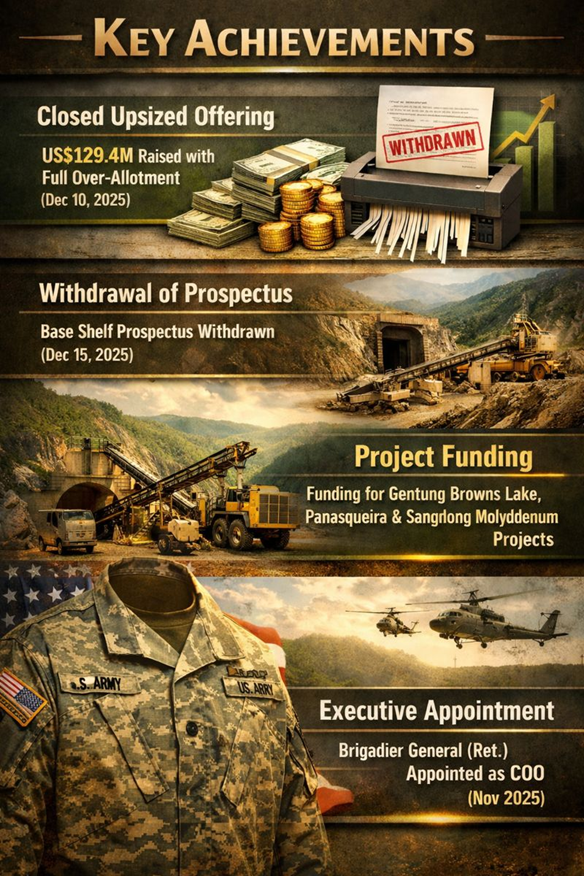

- Closed Upsized Offering: Successfully closed the US$129.4 million offering, including the full exercise of the over-allotment option (Dec 10, 2025).

- Withdrawal of Prospectus: Voluntarily withdrew the base shelf prospectus, indicating the company is fully capitalized for its immediate project pipeline (Dec 15, 2025).

- Project Funding: Net proceeds from the offering are explicitly earmarked for Gentung Browns Lake development, Panasqueira expansion, and Sangdong Molybdenum project work.

- Executive Appointment: Appointed a decorated U.S. Army Brigadier General (Retired) as Chief Operating Officer, further strengthening the focus on U.S. defense supply chain security (Nov 2025).

Source: Kalkine Group

Key Risks

- Project Execution Risk: The successful and timely commissioning of the flagship Sangdong Mine (expected H2 2025) is crucial. Delays or cost overruns could negatively impact the stock.

- Capital Intensive: Mining operations, especially development-stage assets, require significant ongoing capital. While the recent raise helps, future funding needs remain a potential risk.

- Tungsten Price Volatility: The company's revenues are sensitive to the global commodity price of tungsten, which can be volatile due to supply/demand dynamics and macroeconomic factors.

- Liquidity/Debt: Financial metrics have shown weaker liquidity (current ratio below 1) and a high debt-to-equity ratio, indicating significant financial leverage.

- Operational Risk: Relying on one operational mine (Panasqueira) for current revenue until Sangdong is fully commissioned poses concentration risk.

Conclusion

Almonty Industries' recent 9% move is a strong reflection of the market pricing in the successful capital raise and the de-risking of its core projects. The company is making significant strides in its strategic goal to become the world's leading non-China tungsten supplier, a narrative powerfully supported by the geopolitical need for secure critical mineral supply chains.

The immediate-term outlook is positive due to the fresh cash injection and clear project timelines. The long-term success hinges on the on-time, on-budget commencement of production at the Sangdong Mine and the effective integration of its new U.S. asset. It is a high-growth, high-risk play tied directly to the future of Western critical mineral security.

Source: Trading View, 15 December 2025

Please wait processing your request...

Please wait processing your request...