The Arctic is heating up, and it’s not just the climate. On December 23, 2025, Amaroq Minerals (TSXV: AMRQ) saw its stock climb approximately 7.8%, closing at CAD 1.92. For retail investors and institutional players alike, this isn't just a daily fluctuation—it's the culmination of a massive pivot from "explorer" to "producer" and "regional hub."

Here is the analytical breakdown of why Amaroq is dominating the TSXV and what the latest updates mean for your portfolio.

The Catalyst: Why the 7.8% Jump on Dec 23?

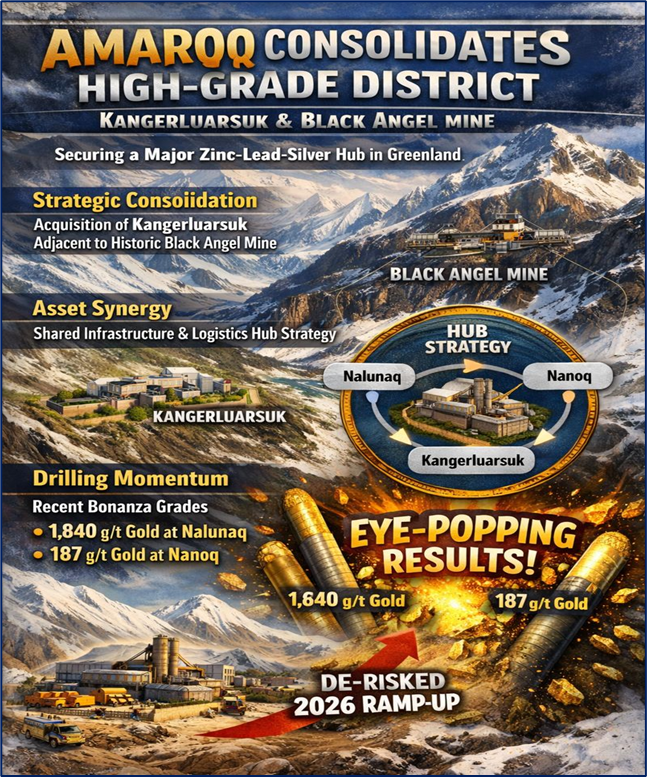

The primary driver for the Dec 23 surge was the official government approval of the Kangerluarsuk project acquisition from 80 Mile PLC. This regulatory green light officially completes the puzzle for Amaroq’s "West Greenland Hub."

Key Drivers:

Source: Kalkine Group

- Strategic Consolidation: By acquiring Kangerluarsuk, Amaroq now controls a massive, high-grade zinc-lead-silver district adjacent to the historic Black Angel mine.

- Asset Synergy: The market reacted positively to the "hub" strategy, which allows Amaroq to share infrastructure, logistics, and personnel across multiple high-potential sites.

- Drilling Momentum: Just weeks prior (Dec 4 & 10), Amaroq reported eye-popping grades, including 1,840 g/t gold at Nalunaq and 187 g/t gold at Nanoq. These "bonanza" grades have de-risked the 2026 production ramp-up.

Latest Business Model: More Than Just a Mine

Amaroq has evolved. In 2025, the company shifted from a pure-play gold explorer to a diversified Arctic mineral infrastructure company.

- The Dual-Hub Strategy:

- South Greenland Hub: Centered on the Nalunaq Gold Mine (currently producing) and the Nanoq project.

- West Greenland Hub: Focused on the Black Angel and Kangerluarsuk projects (zinc, lead, silver).

- The Owner-Operator Shift: On Oct 1, 2025, Amaroq officially transitioned to an owner-operated model. They stopped relying on expensive third-party contractors and bought their own mining fleet. This drastically improves margin control.

- Service Monetization: Through its subsidiary Suliaq ApS, Amaroq is now providing mining and logistics services to other companies in Greenland, turning their operational expertise into a secondary revenue stream.

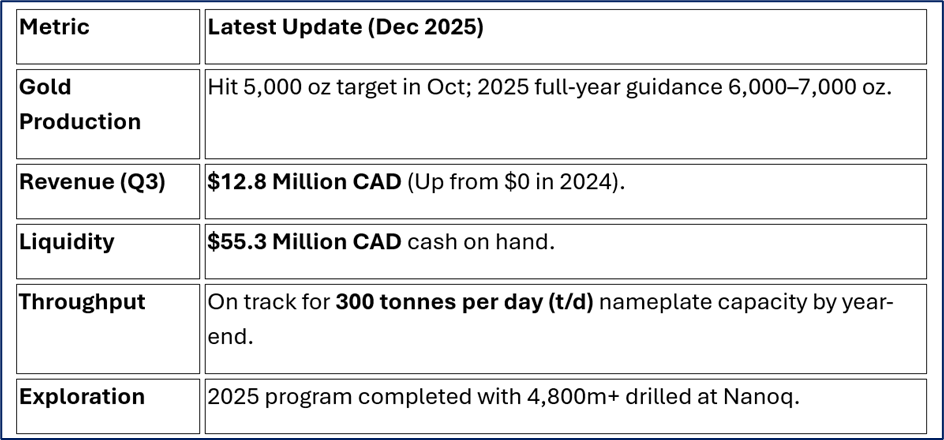

Operational & Financial Pulse Check (Q4 2025)

Source: Kalkine Group

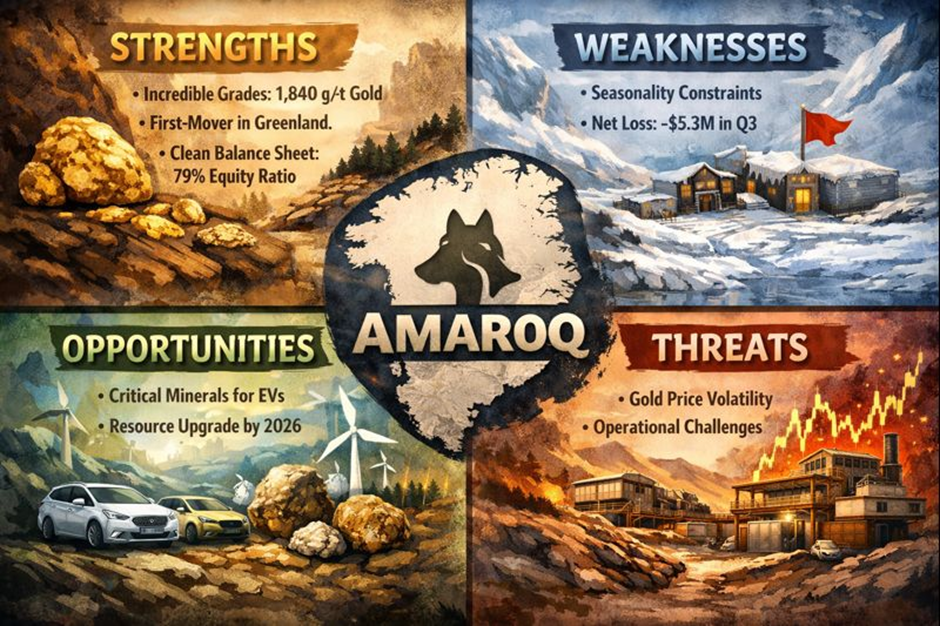

SWOT Analysis: The Hard Truth

Source: Kalkine Group

Strengths

- Incredible Grades: 1,840 g/t gold is among the highest-grade intersections globally.

- First-Mover Advantage: Amaroq is essentially "The Mining Company" of Greenland, with deep ties to the local government.

- Clean Balance Sheet: High equity ratio (~79%) and strong institutional backing (e.g., Landsbankinn).

Weaknesses

- Seasonality: Arctic operations are subject to extreme weather windows.

- Net Losses: Despite revenue growth, the company is still in a net loss position ($5.3M in Q3) due to massive exploration spending.

Opportunities

- Critical Minerals: Demand for zinc and rare earth elements (found at Nunarsuit) is skyrocketing for the EV sector.

- Resource Upgrade: An updated Mineral Resource Estimate (MRE) is expected in Q1 2026, which could significantly re-rate the stock.

Threats

- Gold Price Volatility: Profitability is sensitive to fluctuations in the $XAU$ price.

- Operational Execution: Bringing the processing plant to full 300 t/d capacity without technical hitches.

The Risk Factor

Investing in Greenland is not for the faint of heart. While the jurisdiction is stable, the operational risk of commissioning a mine in a remote Arctic environment is high. If the 300 t/d throughput target is missed, or if Phase 2 flotation circuit installation is delayed, the stock could see a pullback from its recent highs.

Conclusion: The 2026 Outlook

Amaroq Minerals has successfully navigated the "Valley of Death" between discovery and production. The 7.8% jump on Dec 23 is a signal that the market finally believes in the West Greenland Hub vision. With $55M in the bank and a resource update coming in Q1 2026, Amaroq is no longer a "penny stock gamble"—it is a legitimate mid-tier producer in the making.

Watch Item: Keep an eye on the Q1 2026 Mineral Resource Estimate. If they convert "Inferred" resources to "Indicated" at the grades seen in recent drilling, $2.00 CAD might just be the new floor.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...