The Toronto Stock Exchange (TSX) saw a late-year spark on December 30, 2025, as Aya Gold & Silver Inc. (TSX: AYA) closed up 5.52%, reaching CAD 20.25. While the broader S&P/TSX Composite remained relatively flat, Aya outpaced the sector, driven by a "perfect storm" of record-breaking silver prices and massive operational de-risking at its flagship Moroccan assets.

Key Drivers: Why AYA is Winning the Tape

The 5.5% jump on December 30 was not an isolated event but a culmination of several bullish catalysts:

Source: Kalkine Group

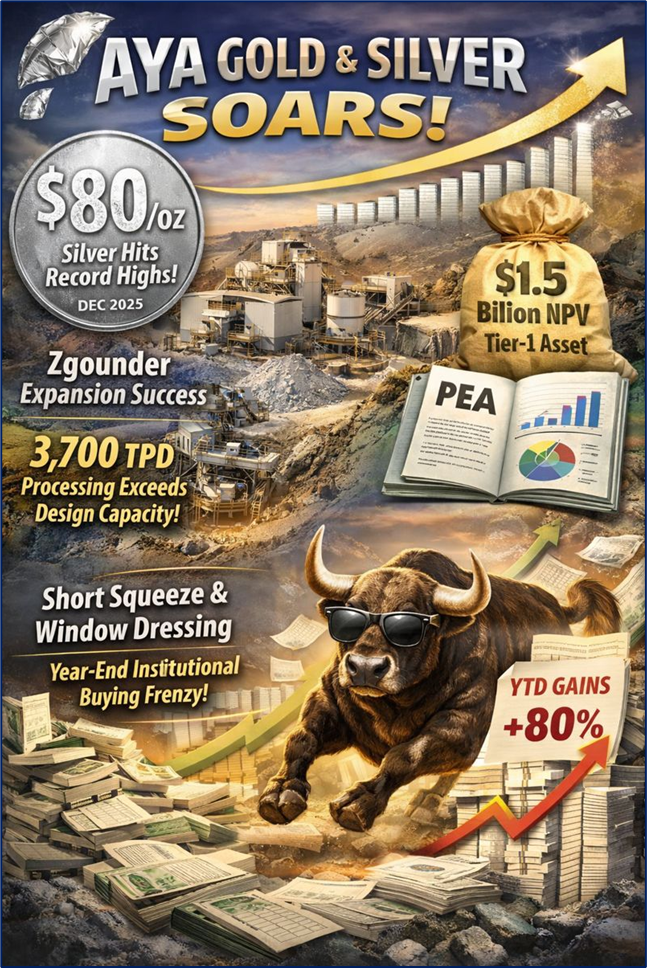

- Silver’s Historic Breakout: Silver hit record highs above $80/oz in late December 2025. As a "pure-play" silver producer, Aya has the highest operating leverage to the metal's price among its peers.

- Zgounder Expansion Success: The Zgounder mine in Morocco has successfully ramped up to a processing rate of 3,700 tonnes per day (tpd), significantly exceeding its initial design capacity of 2,700 tpd.

- Boumadine PEA Hype: The recently filed Preliminary Economic Assessment (PEA) for the Boumadine project revealed an eye-popping Post-tax NPV of $1.5 Billion, positioning it as a "Tier-1" asset that could sextuple Aya's current production.

- Short-Squeeze & Year-End Window Dressing: After a brief dip in mid-December, institutional investors likely re-entered positions to capture the 80%+ year-to-date gains for their year-end portfolios.

Latest Business Model: From Junior to Mid-Tier Major

Aya Gold & Silver has transitioned from a high-risk explorer into a high-margin producer. Its business model is built on three pillars:

- Low-Cost Production: Leveraging Moroccan infrastructure to maintain cash costs near $20/oz while selling at $50-$70/oz.

- Organic Growth: Reinvesting record Q3/Q4 cash flows ($22M+ per quarter) into drilling rather than debt.

- Safe-Haven Jurisdiction: Morocco has emerged as a premier mining destination, offering Aya a stable environment compared to traditional silver hubs in Latin America.

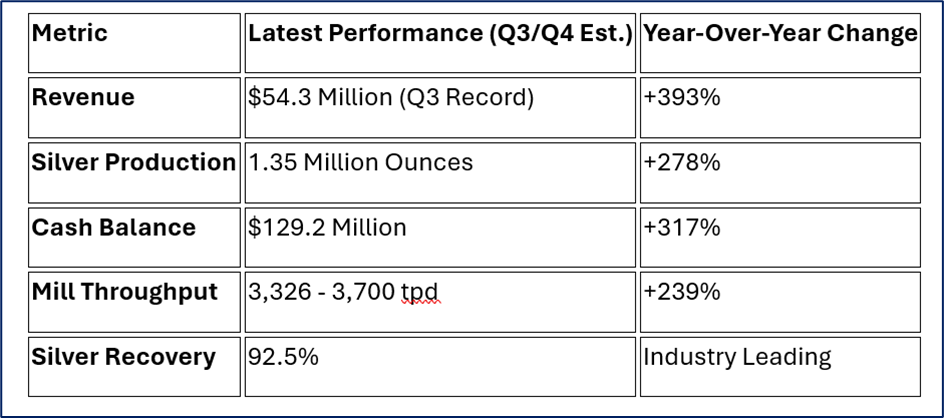

Financial & Operational Health Check (Q3/Q4 2025)

Source: Company Data

SWOT Analysis: The "Bull vs Bear" Breakdown

Source: Kalkine Group

Strengths

- Pure-Play Exposure: Generates 100% of revenue from silver.

- Operating Leverage: Profit margins expanded by over $30/oz in Q4 2025.

- Balance Sheet: Debt-free with nearly $130M in cash.

Weaknesses

- Geographic Concentration: Primary revenue is tied solely to Morocco.

- Grade Volatility: Underground grades fluctuate (138 g/t to 160 g/t), impacting short-term output.

Opportunities

- Boumadine Project: Potential to produce 30M+ oz of silver equivalent annually.

- Exploration Blue Sky: 452 km² land package with multiple untested targets.

Threats

- Silver Price Correction: A "blow-off top" in silver prices could lead to a sharp pullback.

- Inflationary Pressures: Rising costs for cyanide, steel, and energy in North Africa.

The Risks: What Could Trip the Rally?

Despite the 5.5% jump, investors are watching two major "red flags":

- Market Overheating: Analysts warn that silver is in "overbought" territory after its 155% annual gain.

- Development Timelines: The Boumadine project requires $446 million in initial capital. While the NPV is high, the construction phase (2027–2029) carries significant execution risk.

Conclusion: The Silver King of 2025?

Aya Gold & Silver enters 2026 as one of the best-performing stocks on the TSX. By delivering record production exactly as silver prices went parabolic, the company has proven its "growth-at-any-cost" phase is over, replaced by a "cash-cow" reality. The December 30 surge reflects a market that is finally pricing in Aya’s transition from a single-mine operator to a multi-asset silver powerhouse.

Please wait processing your request...

Please wait processing your request...