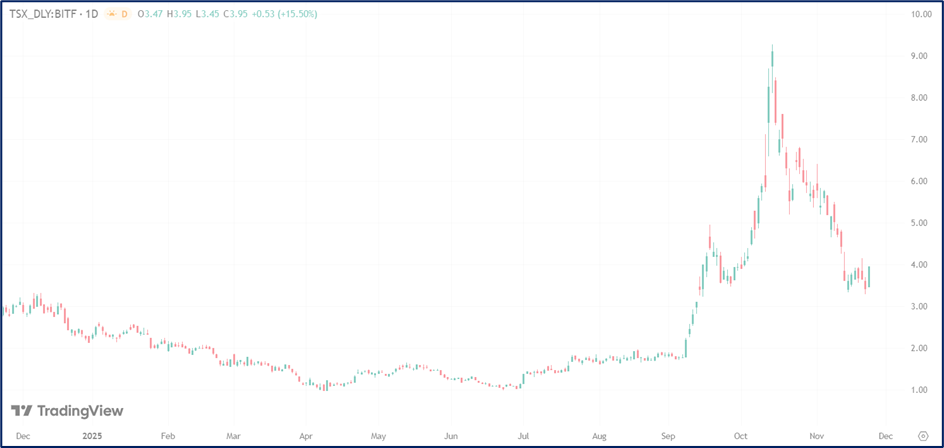

1. The Surge: Why Did Bitfarms Stock Jump Yesterday?

Bitfarms (TSX: BITF / NASDAQ: BITF) surged approximately 15.50% yesterday. This rally wasn't driven by a single press release from the company but rather a "perfect storm" of macroeconomic and sector-wide tailwinds:

- Fed Rate Cut Optimism: The primary catalyst was renewed investor confidence that the U.S. Federal Reserve will cut interest rates in December. Lower rates typically boost risk assets like cryptocurrency stocks by reducing borrowing costs and weakening the dollar (which often inversely correlates with Bitcoin).

- Sector-Wide Rally: The broader Canadian IT and crypto sectors surged, with the TSX gaining nearly 1.5%. Bitfarms acted as a high-beta play, amplifying the gains of the underlying Bitcoin market.

- AI Pivot Momentum: Investors are continuing to price in the long-term value of Bitfarms’ strategic shift from pure-play Bitcoin mining to HPC (High-Performance Computing) and AI infrastructure, a narrative that has gained traction since their Q3 earnings report earlier this month.

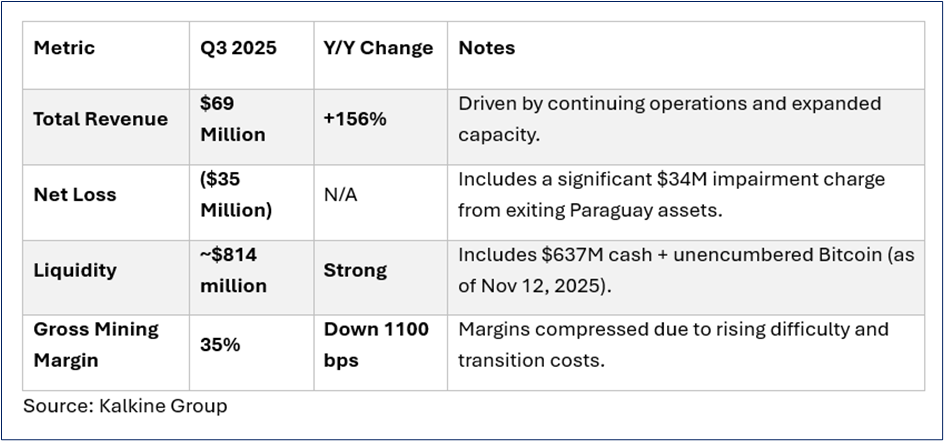

2. Financial Pulse: Q3 2025 Earnings Recap

Bitfarms' latest financial report highlights a company in transition. While top-line growth is explosive, profitability remains under pressure due to heavy investment in their new direction.

Key Takeaway: The company is "spending money to make money," sacrificing short-term margins to build massive infrastructure for the future.

3. Operational Updates: The "HPC" Transformation

Bitfarms is no longer just a Bitcoin miner; it is rebranding as a "North American Energy and Digital Infrastructure Company."

- The Great US Pivot:

- Exiting South America: Bitfarms has discontinued operations in Argentina and sold assets in Paraguay.

- Entering the US: They completed the acquisition of Stronghold Digital Mining, securing a massive footprint in Pennsylvania (PJM market). This move reduces political risk and secures regulated power.

- Infrastructure Upgrade:

- Washington Site Conversion: A key site in Washington is being retrofitted with advanced liquid cooling to support NVIDIA’s GB200/GB300 GPUs.

- AI Readiness: The company claims its new sites are being built to support next-gen AI hardware (NVIDIA Vera Rubin GPUs) due in late 2026, positioning them ahead of competitors focused only on current-gen tech.

4. Evolving Business Model

The company is moving from a Single-Revenue Stream to a Hybrid Model.

- Old Model (100% Bitcoin Mining):

- Revenue depends entirely on Bitcoin price and network difficulty.

- Highly volatile; cash flow is unpredictable.

- New Model (Mining + HPC/AI):

- Base Layer (Mining): Uses fluctuating/excess power to mine Bitcoin. Acts as a flexible load to monetize energy instantly.

- Growth Layer (HPC/AI): Hosting high-performance computing for AI clients. This offers stable, fixed-rate contracts, higher margins, and significantly less volatility than crypto mining.

5. Growth Drivers & Catalysts

- The AI Infrastructure Shortage: The world is running out of data center capacity with power access. Bitfarms controls nearly 1 GW of power (active + pipeline), making their "plug-in ready" sites extremely valuable real estate for AI companies.

- Bitcoin Cycle: If Bitcoin enters a parabolic phase in late 2025/2026, Bitfarms' mining segment will generate massive free cash flow to fund their expensive AI build-out without dilution.

- Merger Synergies: The full integration of Stronghold Digital Mining is expected to improve operational efficiency and expand their power portfolio in the US PJM grid.

6. Critical Risks to Watch

- Execution Risk: Pivoting to HPC is difficult. It requires different cooling, higher uptime guarantees (99.99%), and different client relationships than Bitcoin mining. Delays could be costly.

- Dilution: The company recently closed a $588 million convertible note offering. While this raised cash, it creates potential future dilution for shareholders.

- Margin Compression: Transition costs (shutting down old sites, building new ones) will likely keep profitability low throughout 2025.

7. Future Guidance (2025-2026)

- Revenue: Analysts project 2025 full-year revenue at roughly $314.5 million.

- Capacity: Targeting massive power capacity growth to over 648 MW by end of 2025.

- Tech Target: Explicit focus on being ready for NVIDIA Vera Rubin (2026), skipping the immediate "Blackwell" cycle to capture the next wave of demand.

Source: Trading View, 24 Nov 2025

Please wait processing your request...

Please wait processing your request...