On December 31, 2025, Black Mammoth Metals (TSXV: BMM) posted a sharp ~9% gain, capping off a volatile but heavily bullish fourth quarter. While the broader junior mining sector has been heating up, BMM’s outsized move wasn't just random noise. It was the market digesting a flurry of high-impact news released in the final weeks of December—specifically centering on aggressive land acquisitions and geophysical breakthroughs in Nevada’s prolific Walker Lane trend.

With Gold hovering near record highs of $4,500/oz and Silver testing $80/oz, the macro tailwinds are undeniable. But for BMM, the specific catalyst is a classic "discovery potential" play. Below is the analytical deep dive into why this stock is moving, the risks involved, and what the latest data says about their chances in 2026.

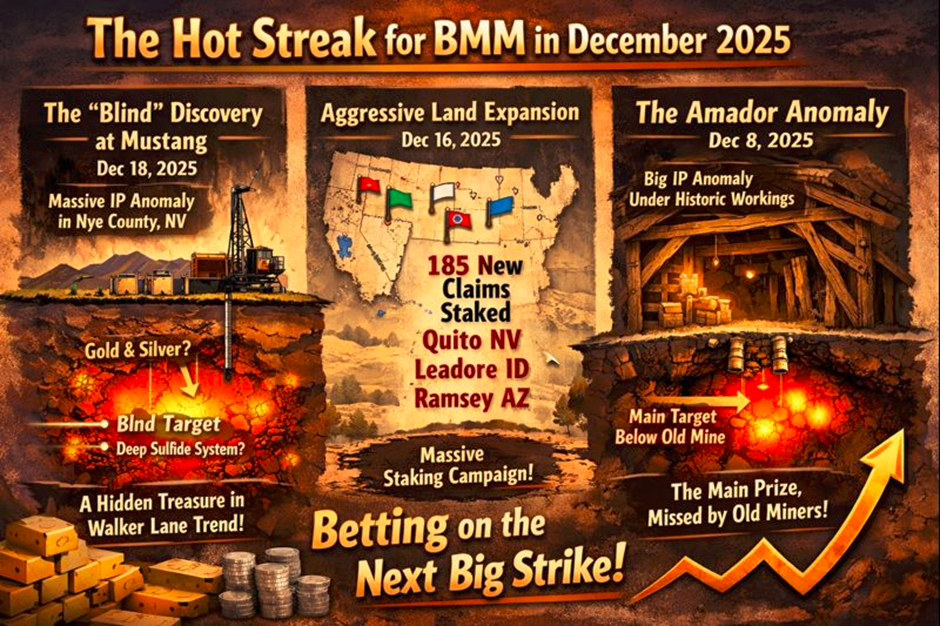

Key Drivers: The "Mustang" Catalyst & The Staking Spree

Source: Kalkine Group

The 9% surge is primarily a delayed reaction to three compounding factors that solidified in late December:

- The "Blind" Discovery Potential at Mustang (Dec 18, 2025) The biggest driver is the acquisition of the Mustang Gold and Silver Property in Nye County, Nevada.

- The News: BMM didn’t just buy land; they released IP (Induced Polarization) survey results showing a "massive" chargeability anomaly.

- Why it Matters: The anomaly is "blind," meaning it has no surface expression (you can't see it from above). This is the geological signature of many major hidden deposits in the Walker Lane trend. The market loves "blind" targets because they haven't been picked over by old-timers.

- Retail Angle: Investors are betting that this anomaly is a large sulfide system loaded with gold/silver, akin to recent major discoveries in the region.

- Aggressive Land Expansion (Dec 16, 2025) Just days before the Mustang news, BMM announced a massive staking campaign:

- 185 New Claims: Added across the Quito (NV), Leadore (ID), and Ramsey (AZ) properties.

- Strategic Signal: Staking claims (instead of buying them) is the cheapest way to acquire assets. This tells the market that management is confident enough to spend their limited cash on expanding their footprint rather than just sitting on existing assets.

- The Amador Anomaly (Dec 8, 2025) Earlier in the month, BMM identified a large chargeability anomaly directly underneath historic mine workings at their Amador Silver Property. This confirmed that the old miners likely missed the "main event" deeper underground—a classic exploration thesis that generates high leverage speculation.

SWOT Analysis

Source: Kalkine Group

Strengths (Internal)

- Tier-1 Jurisdiction Focus: 100% of assets are in the Western USA (Nevada, Arizona, Idaho). No geopolitical risk from unstable governments.

- Low-Cost Acquisition Model: Management excels at "staking" rather than overpaying for leased properties, keeping royalty burdens low (e.g., Mustang is 100% owned with no royalties).

- Technical Team: Proven ability to use modern geophysics (IP surveys) to find targets that previous operators missed.

Weaknesses (Internal)

- Cash Burn: As a pre-revenue junior explorer, BMM burns cash every day. The aggressive staking and surveying in Q4 2025 likely depleted reserves, raising the specter of a near-term capital raise.

- Early Stage: These are anomalies, not defined resources. There is no NI 43-101 compliant resource estimate yet. They are drilling "targets," not "deposits" at this stage.

Opportunities (External)

- The $4,400 Gold Environment: At these prices, even lower-grade deposits become economically viable. If BMM hits anything significant, the leverage to the gold price is massive.

- M&A Target: Major miners are desperate to replenish reserves in safe jurisdictions like Nevada. A successful drill hit at Mustang or Amador could arguably make BMM an instant acquisition target.

Threats (External)

- Dilution Risk: To fund the upcoming drilling campaigns for 2026, the company will almost certainly need to issue more shares, which dilutes existing holders.

- Permitting Delays: Nevada is mining-friendly, but the BLM (Bureau of Land Management) can still be slow with drill permits, potentially stalling momentum.

Business Model: "Hunt, Stake, & De-Risk"

Black Mammoth’s business model is distinct from a mining operator. They are a Project Generator and Explorer.

- Identify: Find overlooked data in historic mining districts (e.g., "old timers mined high-grade veins here, but missed the bulk tonnage halo").

- Stake: Claim the land directly from the government to avoid paying millions to private vendors.

- De-Risk: Spend $50k-$100k on geophysics (IP, Magnetics) to prove a target exists.

- Monetize: Either drill it themselves (high risk/high reward) or farm it out to a major partner who pays for the drilling.

Current Status: They are currently shifting from step 3 to step 4, preparing to drill the anomalies they defined in late 2025.

Financial & Operational Update (Q4 2025 Snapshot)

- Stock Price Performance: The stock touched a 52-week high of ~$6.44 in mid-December before consolidating and popping again on Dec 31.

- Market Cap: hovering in the ~$150M - $240M range (depending on exact share count/dilution), which is a "mid-tier" valuation for an explorer—pricing in some success but not a major discovery yet.

- Liquidity: Trading volume spiked >15% above average in the final days of the year, indicating institutional or heavy retail accumulation.

- Liabilities: Q3 reports showed a ~70% increase in liabilities, likely due to the ramp-up in exploration activities. Investors should watch the next quarterly filing closely for cash positions.

Risks: What Could Go Wrong?

Retail investors often ignore the downside. Here is the reality check:

- The "Dust" Risk: Geophysical anomalies are often just graphite, pyrite, or water—not gold. If the maiden drill holes at Mustang come up empty ("dusters"), the stock could crash 30-50% overnight.

- Sector Rotation: If the Gold/Silver price corrects from its highs ($4,400/$60), capital will flee the risky junior sector first.

- Financing Overhang: If the company announces a private placement at a discount to the current price, the stock will likely drop to that financing price.

Conclusion: A High-Octane Bet on Nevada's Underground

Black Mammoth Metals closed 2025 with a 9% gain because it successfully transitioned from "looking for land" to "defining drill targets." The market is speculating that the blind anomaly at Mustang or the deep targets at Amador are the real deal.

For the retail investor, BMM represents a classic high-beta exploration play: You are paying for the probability of a discovery in a booming precious metals market. The technicals (price action) confirm momentum, and the fundamentals (assets/jurisdiction) are solid. The wildcard is the drill bit.

Verdict: The stock is up because the "fuse" has been lit. 2026 will determine if the bomb explodes (discovery) or fizzles out (dusters).

Please wait processing your request...

Please wait processing your request...