Executive Summary: Why the Green Candle?

While most retail investors were checking out for the holidays, Boralex (TSX: BLX) quietly posted a robust ~1.2% gain on December 24, 2025. This wasn't just a "Santa Claus Rally"; it was a direct response to a major regulatory win in the United Kingdom announced late on December 23. The approval of the Clashindarroch Wind Farm Extension signals a massive de-risking of their UK pipeline, validating their 2030 expansion strategy.

Below is the analytical breakdown of why this stock is moving, the latest financials that retail often overlooks, and the risks you need to price in.

- Key Reasons & Drivers for the Move

Source: Kalkine Group

The Catalyst: UK Regulatory "Green Light"

On December 23, 2025, the Scottish Ministers officially approved the Clashindarroch Wind Farm Extension. This is not just "another project"—it is a cornerstone of Boralex's European growth.

- Scale: Up to 189 MW of new wind capacity.

- Hybridization: Includes a 50 MW battery storage facility, critical for grid stability revenues.

- Market Signal: Investors view this as proof of execution ability in the tough UK regulatory environment, unlocking future cash flows from the Scottish market.

The successful commissioning of the Apuiat Wind Farm (200 MW total / 100 MW Boralex share) in Quebec earlier in Q4 2025 has moved capital expenditure (Capex) into cash-flow-generating assets. The market is now pricing in the revenue from these new electrons.

Sector Tailwinds

By late December 2025, the broader utility sector has stabilized as bond yields moderate. Investors are rotating back into "growth utilities" that offer both dividends and capital appreciation, and Boralex fits this profile perfectly.

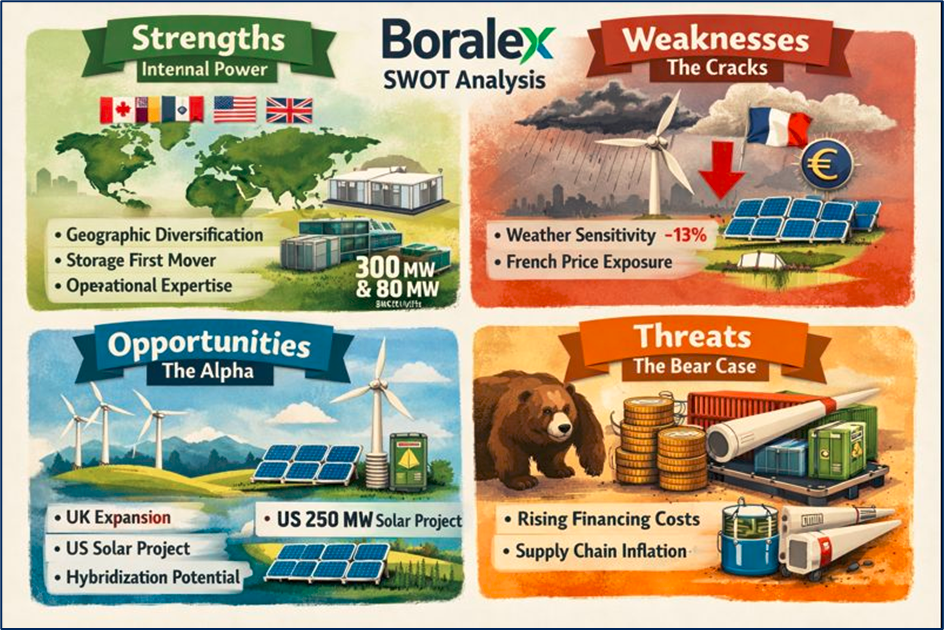

- SWOT Analysis

Source: Kalkine Group

Strengths (Internal Power)

- Geographic Diversification: Revenue is now split across Canada, France, the US, and the UK, reducing reliance on any single regulatory regime.

- Storage First Mover: With the Hagersville (300 MW) and Tilbury (80 MW) battery projects in Ontario nearing Q4 commissioning, Boralex is transitioning from a pure-play generator to a grid-stabilization asset manager.

- Operational Expertise: Over 3.4 GW of installed capacity with high availability rates (excluding weather anomalies).

Weaknesses (The Cracks)

- Weather Sensitivity: Q3 2025 results missed expectations due to poor wind resources in North America (-13% vs. anticipated production), highlighting the inherent volatility of their fuel source.

- French Price Exposure: Recent dips in French power prices have dragged down EBITDA compared to the record highs of 2024.

Opportunities (The Alpha)

- UK Pipeline: The Clashindarroch approval opens the door for further UK expansion, a market hungry for onshore wind.

- US Solar: A 250 MWac solar project in the US recently moved to the "secured" stage, diversifying the technology mix away from pure wind.

- Hybridization: Retrofitting existing wind farms with battery storage (like Clashindarroch) to capture peak pricing.

Threats (The Bear Case)

- Financing Costs: Despite stabilization, interest rates remain structurally higher than the 2010-2020 era, increasing the cost of debt for their 8 GW development pipeline.

- Supply Chain Inflation: Turbine and battery costs remain elevated, potentially squeezing Internal Rate of Return (IRR) on future projects.

- Latest Business Model: Beyond Just "Selling Power"

Boralex has evolved its business model in late 2025 from a simple Independent Power Producer (IPP) to an Energy Management Platform.

- Core Income: Long-term Power Purchase Agreements (PPAs) and Feed-in Premiums (FIPs) provide stable, contracted cash flows (approx. 13-14 years average remaining contract duration).

- The Shift: They are aggressively entering Energy Storage. By co-locating batteries with wind/solar, they can store cheap off-peak power and sell it during high-demand windows, effectively engaging in "energy arbitrage" and providing lucrative grid services.

- Growth Engines: The "2030 Strategy" targets a balanced portfolio where US Solar and UK Wind complement the cash-cow assets in Quebec and France.

- Financial & Operational Updates (Q3 2025 Recap)

- Revenue (Q3 '25): $144 Million (Down 4% YoY). Reason: Normalization of French power prices.

- EBITDA(A): $85 Million (Down 2% YoY).

- Installed Capacity: Reached 3,403 MW following the Apuiat commissioning in Oct 2025.

- Cash Flow: Net cash from operating activities swung positively to $37 Million (vs. outflow in Q3 '24), showing better working capital management.

- Development Pipeline: Added 395 MW of new projects to the pipeline in Q3, bringing the total pipeline to over 6 GW.

- Risks for Retail Investors

- Execution Risk on Storage: The Hagersville and Tilbury battery projects are massive. Any technical delays in their final commissioning (scheduled Q4 2025) could hurt Q1 2026 earnings.

- Merchant Price Volatility: While most contracts are fixed, the portion of revenue exposed to market prices (especially in France) can lead to earnings misses, as seen in Q3.

- Currency Fluctuations: With significant revenues in Euros (EUR) and Pounds (GBP), a strengthening Canadian Dollar (CAD) can artificially depress reported earnings.

Conclusion

The 1.2% move on December 24, 2025, is a rational market reaction to a tangible win. The Clashindarroch approval validates Boralex's ability to navigate complex European bureaucracies and deliver high-value hybrid projects.

While Q3 financials showed some weather-related weakness, the addition of the Apuiat Wind Farm and the imminent Ontario Battery Storage commissioning sets the stage for a potentially record-breaking 2026. For investors, Boralex represents a "Growth at a Reasonable Price" (GARP) play in the renewable transition, now supercharged by battery storage economics.

Please wait processing your request...

Please wait processing your request...