- The Surge: Why is C3 Metals Up 23% Today?

C3 Metals Inc. (TSXV: CCCM) is trading significantly higher today, driven by a perfect storm of high-impact exploration success and a sector-wide commodity super-rally. While the company did not release a specific press release this morning, the stock is catching a massive "delayed reaction" bid following its transformational discovery at the Khaleesi Project in Peru, amplified by today's global flight to hard assets.

The Trigger: A massive geopolitical shock involving Venezuela reported today has sent gold and silver prices to record highs ($4,549/oz gold mentioned in market reports). Investors are scrambling for junior miners with significant "leverage to discovery," and C3 Metals—with its massive new copper-gold intercepts—is a prime target.

- Key Drivers

Source: Kalkine Group

- The "Khaleesi" Discovery (The Game Changer):

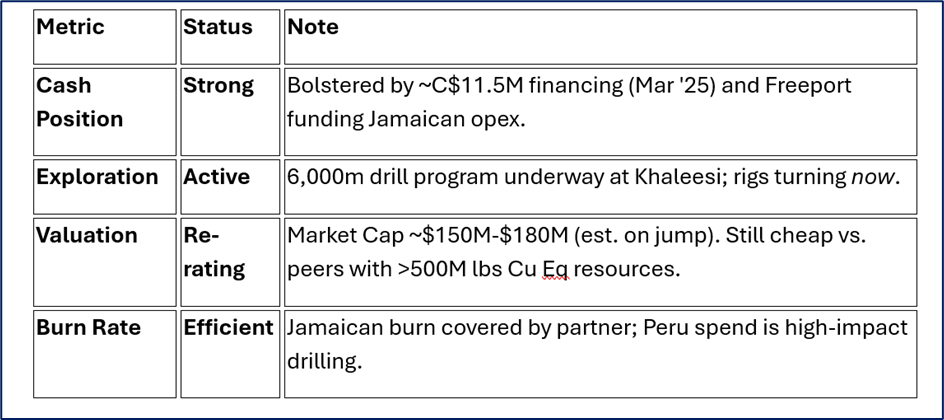

Investors are still pricing in the December 15, 2025 news, which many analysts believe changes the company's valuation floor. The first-ever hole at the Khaleesi Copper-Gold Project in Peru intersected 269m @ 0.30% Copper, including a high-grade magnetite skarn zone of 60.4m @ 0.41% Copper.

- Why it matters: This confirms a massive, mine-grade system under glacial till that was previously "blind" (invisible) to surface exploration. It opens up a potential billion-tonne target.

- Macro Tailwinds (Gold & Copper Supercycle):

With today's geopolitical instability (reports of the Venezuelan leadership crisis), capital is fleeing fiat currencies for tangible assets. C3 Metals is not just copper; its deposits have significant gold and silver credits, making it a "double hedge" for investors seeking safety + growth.

- The Freeport-McMoRan Factor:

The market is re-evaluating the US$75M earn-in deal with mining giant Freeport-McMoRan for the Jamaican assets (Bellas Gate). This deal validates C3’s portfolio and removes significant financing risk for the Jamaican operations, allowing C3 to focus cash on Peru.

- Updated Business Model

C3 Metals has pivoted from a "shotgun" explorer to a focused district developer with two flagship engines:

- Peru (The "Company Maker"):

- Focus: 100% owned Khaleesi and Jasperoide projects in the Andahuaylas-Yauri Belt (elephant country hosting Las Bambas and Constancia mines).

- Strategy: Aggressive drilling to define a "Tier-1" copper-gold porphyry/skarn resource.

- Jamaica (The "Free Carry"):

- Focus: Bellas Gate and Super Block projects.

- Strategy: Let partner Freeport-McMoRan pay for the drilling (up to US$75M) to earn their stake, while C3 retains upside with zero capital outlay.

- Financial & Operational Snapshot (Jan 2026)

Source: Company Data

- SWOT Analysis (Strategic Breakdown)

Source: Kalkine Group

Strengths (Internal)

- Tier-1 Geology: Located next to major mines (Glencore, MMG, Hudbay) in Peru.

- Validating Partners: Freeport-McMoRan deal creates a "halo effect" of credibility.

- Management Pedigree: Team has a track record of discovery and exits (Dan Symons, etc.).

- Dual Exposure: Exposure to both industrial (Copper) and precious (Gold/Silver) metals.

Weaknesses (Internal)

- Liquidity: As a TSXV junior, volume can dry up, leading to high volatility (gaps).

- Peru Dependency: While Jamaica is funded, the "home run" valuation relies entirely on Peru drilling success.

- Complexity: Managing active programs in two different jurisdictions (Caribbean & Andes) splits management attention.

Opportunities (External)

- M&A Target: Mid-tier miners are desperate for copper reserves. A defined resource at Khaleesi makes C3 a prime takeover candidate.

- Copper Deficit: Global copper supply crunch (for EVs/AI data centers) is keeping floor prices high ($4.50-$5.00+/lb).

- Drill Bit Catalyst: Every new assay from the current 6,000m program can spark a 10-20% move.

Threats (External)

- Geopolitics (Peru): Peru has a history of community protests blocking mining roads (e.g., Las Bambas). Any local unrest could halt drilling.

- Dilution: If the stock price sags, future drilling will require raising cash at lower prices, hurting existing shareholders.

- Market Risk: If the "war premium" on gold fades, the speculative bid for juniors could vanish overnight.

- Risks to Watch

- The "One Hole Wonder" Risk: The market is ecstatic about the first hole at Khaleesi. If holes 2, 3, and 4 miss or show lower grades, the stock will crash hard. Consistency is unproven.

- Permitting Delays: Peru is notoriously slow for drill permits. Any bureaucratic stall will kill momentum.

- Profit Taking: After a 23% single-day move, short-term traders will likely dump shares tomorrow to lock in gains.

- Conclusion

C3 Metals is no longer just a "promising story"—it is a proof-of-concept discovery play. The 23% surge today is a rational market repricing based on the Khaleesi discovery de-risking and a supportive macro environment for gold and copper.

The stock offers a rare combination in the junior space: Partner-funded exploration (Jamaica) providing a safety net, and 100%-owned high-octane drilling (Peru) providing the moonshot potential.

Verdict: For risk-tolerant retail investors, C3 Metals is a high-conviction watchlist candidate. The easy money might have been made today, but the big money depends on the next 3 drill holes.

Please wait processing your request...

Please wait processing your request...