Calfrac Well Services Ltd. (TSX: CFW) just handed its shareholders an early Christmas gift. On December 23, 2025, the stock surged approximately 17.6%, hitting a 52-week high of CAD 4.26 during intraday trading. For a company that was fighting for its life during the pandemic, this "Santa Rally" is backed by more than just holiday cheer—it is the result of a massive balance sheet cleanup.

Why the 17.6% Spike? The "Big Debt" Exit

The primary driver behind today's vertical move is the closing of an oversubscribed Rights Offering and the subsequent total redemption of Second Lien Notes.

Source: Kalkine Group

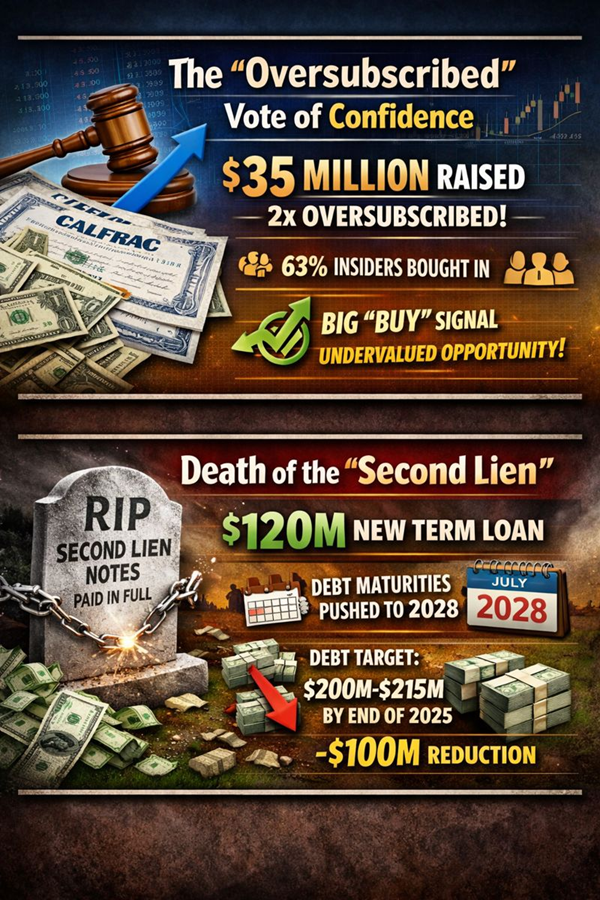

1. The "Oversubscribed" Vote of Confidence

On December 23, Calfrac announced it successfully raised $35 million through a rights offering that was more than 2x oversubscribed.

- Why it matters: Retail and institutional investors fought for shares at $2.69. When a rights offering is oversubscribed, it signals to the market that insiders and major holders believe the stock is significantly undervalued.

- Insider Skin in the Game: Directors and officers snapped up 63% of the offering, a massive "Buy" signal to the public.

2. Death of the "Second Lien"

Calfrac is using the $35 million plus a new $120 million term loan to wipe out its Second Lien Notes.

- The Result: Long-term debt maturities have been pushed out to July 1, 2028.

- The Deleveraging Story: The company expects to exit 2025 with total debt between $200M – $215M, a reduction of over $100 million in just one year.

Latest Business Model & Strategy

Calfrac has evolved from a "growth-at-all-costs" pumper to a high-efficiency, debt-reduction machine.

- Tier IV Modernization: In North America, Calfrac has pivoted to Dynamic Gas Blending (DGB) Tier IV fleets. These use natural gas to displace diesel, lowering costs for E&P (Exploration & Production) companies and meeting ESG mandates.

- The Argentina Powerhouse: While North America is stable, Argentina (Vaca Muerta shale) is the growth engine. Calfrac now operates two large unconventional fracturing spreads there, taking advantage of higher margins and better pricing than in the saturated US/Canadian markets.

- Focus on Free Cash Flow (FCF): The 2026 outlook calls for "significantly lower" capital expenditure, meaning almost every dollar earned will go toward further debt reduction or potential shareholder returns.

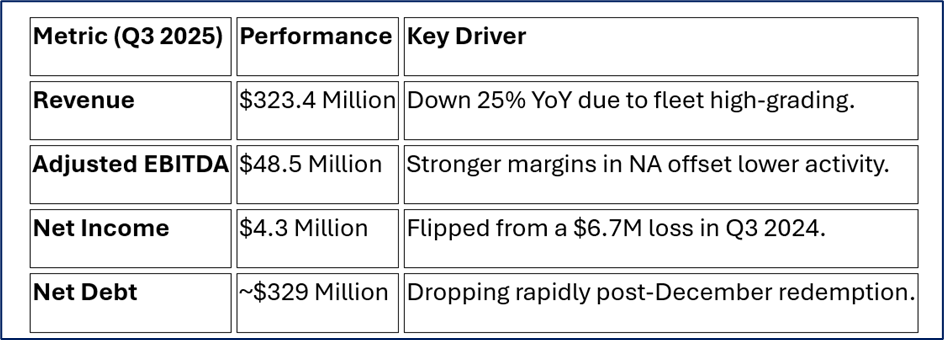

Financial & Operational Pulse

Source: Company Data

SWOT Analysis: The No-Fluff Breakdown

Source: Kalkine Group

Strengths

- Modern Fleet: Heavy investment in Tier IV DGB technology.

- Market Share: Top-tier provider in Western Canada and Argentina.

- Operational Discipline: Successful "right-sizing" of the North American footprint to 10 active fleets.

Weaknesses

- Historical Debt Load: While improving, debt levels still limit aggressive expansion.

- Regional Concentration: Heavily reliant on the Western Canadian Sedimentary Basin and the Vaca Muerta.

Opportunities

- Argentina Repatriation: Recent government moves in Argentina make it easier for Calfrac to bring cash back to Canada.

- Gas-Oriented Demand: Increased LNG exports from Canada (LNG Canada project) could spike demand for fracturing services in 2026.

Threats

- E&P Capital Discipline: Oil companies are spending less on drilling to pay dividends, limiting Calfrac's "top-line" growth.

- Geopolitical Volatility: Trade tensions and OPEC+ shifts can swing oil prices and drilling budgets overnight.

Critical Risks to Watch

- Macro-Slowdown: If oil prices sustain a drop below $65-70/bbl, North American activity could crater.

- Labor Inflation: The cost of specialized crews remains high, squeezing margins.

- Currency Risk: Significant operations in Argentina expose the company to the volatile Peso and local inflation.

Conclusion

The 17.6% jump on Christmas Eve isn't just a technical bounce—it’s the market re-rating Calfrac as a "survivor." By clearing the 2026 debt hurdle and securing long-term runway until 2028, management has removed the "bankruptcy risk" premium that has dogged the stock for years.

What’s next? Investors will be watching the Q4 2025 earnings (expected March 2026) to see if the leaner 10-fleet North American model can maintain its improved EBITDA margins.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...