Strong distributable cash flow, a fee-based infrastructure model, and disciplined capital allocation are positioning Keyera Corp (TSX: KEY) as one of Canada’s most resilient midstream dividend growth stories heading into 2026. With shares rising approximately 3.2% on 12 February 2026 and outperforming parts of the broader Canadian market, investors are asking a critical question:

Can Keyera continue delivering reliable dividend growth in a stabilizing but still uncertain global energy environment?

Why Did Keyera Stock Rise 3.2% on 12 February 2026?

Keyera shares gained momentum as capital rotated into Canadian midstream and dividend-oriented infrastructure stocks. Several catalysts supported the move:

- Higher natural gas liquids (NGL) volumes across Western Canada

- Stable crude oil benchmarks supporting upstream production activity

- Renewed institutional inflows into dividend growth equities

- Defensive positioning amid global equity volatility

- Strength in energy-heavy Canadian indices

As recession fears moderated and commodity markets stabilized in early 2026, midstream operators with predictable cash flows regained investor attention.

Global Macro Tailwinds Supporting Canadian Energy Infrastructure

The February 2026 macro environment reflects improving stability:

- Moderating inflation across G7 economies

- OPEC+ supply discipline supporting oil price stability

- Reduced volatility in U.S. Treasury yields

- Capital rotation into yield-focused infrastructure assets

Midstream companies like Keyera benefit structurally because their revenues are primarily:

- Volume-based

- Fee-based

- Contract-backed

- Less directly exposed to commodity price swings

This backdrop enhances the appeal of energy infrastructure dividend stocks relative to cyclical upstream producers.

How Canada’s Economy Is Reinforcing Keyera’s Outlook

Canada’s economic profile in early 2026 remains constructive:

- Stable GDP growth supported by energy exports

- Controlled inflation dynamics

- A relatively stable Canadian dollar (CAD)

- Continued infrastructure investment in Alberta’s energy sector

Keyera’s gathering, processing, and liquids infrastructure network directly benefits from rising production volumes and long-term take-or-pay contracts. A steady CAD also improves revenue predictability for export-linked throughput volumes.

What Sector Rotation Signals from the S&P/TSX Composite Index Mean for Keyera

Recent trading patterns show:

- Rotation into energy, utilities, and income-oriented equities

- Relative underperformance in high-growth technology stocks

- Defensive capital flows favoring dividend reliability

Keyera fits squarely within this rotation theme. When investors prioritize yield stability and cash flow visibility, midstream infrastructure stocks tend to outperform.

Understanding Keyera’s Resilient Business Model

Keyera operates across three primary segments:

- Gathering and Processing

- Liquids Infrastructure

- Marketing

Its model emphasizes:

- Long-term customer contracts

- Fee-based revenue streams

- High-barrier infrastructure assets

- Conservative payout ratios

- Disciplined capital allocation

Recent investor materials highlight steady distributable cash flow and margin stability, reinforcing the durability of its dividend framework.

How Attractive Is Keyera’s Dividend in 2026?

Keyera remains widely regarded as a Canadian dividend growth stock with:

- A competitive yield relative to midstream peers

- A monthly dividend structure favored by income investors

- A payout ratio supported by recurring infrastructure revenue

- Predictable distributable cash flow coverage

Unlike upstream producers, Keyera’s dividend is not directly tied to volatile commodity pricing. Instead, it is supported by contracted infrastructure cash flow — a key differentiator in uncertain markets.

How Does Keyera Compare to Peers?

Within the Canadian midstream space, key competitors include:

- Enbridge Inc. – Larger scale, diversified pipelines, strong dividend history

- TC Energy Corporation – Major North American natural gas infrastructure operator

- Pembina Pipeline Corporation – Significant liquids infrastructure exposure

Keyera differentiates itself through:

- Concentrated NGL infrastructure focus

- Nimble capital deployment

- Volume growth leverage during production upcycles

- Smaller but efficient operating footprint

While not as diversified as Enbridge, Keyera often offers stronger sensitivity to improving NGL volumes.

Technical and Fundamental Outlook for 2026

Short-Term (3–6 Months): Moderately Bullish

- Positive price momentum

- Energy sector capital inflows

- Stable oil and gas backdrop

Potential risk: sudden commodity price weakness or macro volatility.

Medium-Term: Neutral to Constructive

- Dependent on Canadian production growth

- Infrastructure utilization rates critical

- Dividend stability remains key

Long-Term: Structurally Constructive

- Natural gas and NGLs remain transition fuels

- Infrastructure bottlenecks support processing demand

- Capital discipline underpins shareholder returns

Analyst Sentiment in February 2026

Consensus across major Canadian brokerages indicates:

- Majority rating: Buy / Outperform

- Price targets moderately above current levels

- Emphasis on predictable free cash flow

The investment thesis centers on cash flow visibility, dividend sustainability, and infrastructure defensiveness.

Key Risks Investors Should Monitor

- Decline in NGL volumes

- Regulatory policy shifts in Canada

- Environmental compliance costs

- Rising interest rates impacting yield stocks

- Debt refinancing exposure

Although the business model is defensive, it remains volume-sensitive and macro-aware.

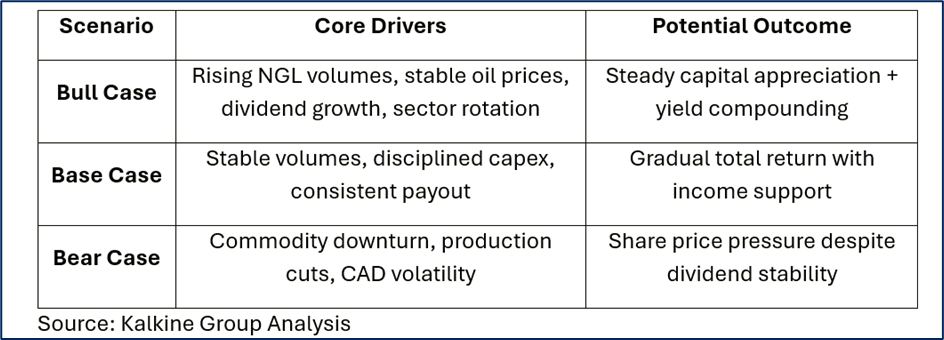

Bull vs Bear Scenario Analysis

Frequently Asked Questions About Keyera in 2026

Is Keyera sensitive to oil prices?

Indirectly via production volumes, but largely insulated through fee-based contracts.

Is the dividend secure?

Currently supported by distributable cash flow and conservative payout metrics.

Is Keyera better than Enbridge?

Depends on objectives: Enbridge offers scale and diversification; Keyera offers targeted NGL growth leverage.

Does CAD strength matter?

Yes. Currency stability influences export competitiveness and investor sentiment.

Final Investment Perspective: Is Keyera a Dividend Growth Stock to Watch in 2026?

Keyera appears positioned as:

- A defensive Canadian energy infrastructure operator

- A reliable monthly dividend payer

- A midstream company benefiting from resilient production volumes

- A disciplined capital allocator

Short-term momentum is constructive.

Medium-term stability hinges on throughput growth.

Long-term returns depend on sustained capital discipline and structural energy demand.

For income-focused investors seeking stable cash flow exposure within Canada’s energy infrastructure sector, Keyera remains a compelling dividend growth watchlist candidate in 2026.

This analysis is for informational purposes only and does not constitute investment advice.

Please wait processing your request...

Please wait processing your request...