Forget the noise; the TSX just witnessed a masterclass in energy resilience. On December 30, 2025, Canadian Natural Resources (TSX: CNQ) defied broader market jitters to climb ~2.2%. While other energy players are treading water, CNQ is swimming in free cash flow.

Here is why the "King of the Oil Patch" is ending the year on a high note and what the latest fundamentals actually look like.

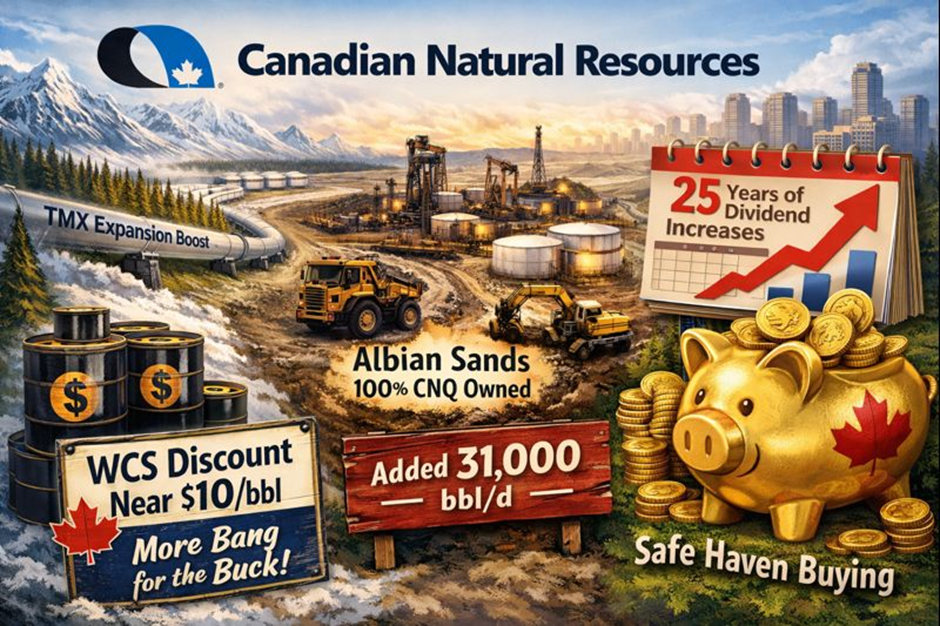

The Big Spark: Why CNQ Popped 2.2% on Dec 30

The late-December rally wasn't a fluke. It was driven by a "perfect storm" of operational wins and favorable macro shifts:

Source: Kalkine Group

- WCS Differential Tightening: The Trans Mountain Expansion (TMX) pipeline, now fully integrated into 2025 flows, has kept the Western Canadian Select (WCS) discount to WTI remarkably narrow (near $10/bbl). This means CNQ is getting more "bang for its buck" for every barrel produced.

- Operational Alpha: Just weeks after closing the Albian Sands swap with Shell (now 100% owned), the market is pricing in the added 31,000 bbl/d of zero-decline production.

- Year-End "Safe Haven" Buying: With 2025 being the 25th consecutive year of dividend increases, retail and institutional investors rotated into CNQ as a defensive yield play to close out the year.

Latest Business Model: The "Low-Decline" Machine

CNQ has evolved from a traditional driller into a manufacturing-style energy giant.

The 2025 Blueprint

- Long-Life, Low-Decline: Approximately 77% of production now comes from assets like oil sands mining that require very little capital to maintain output.

- Multilateral Drilling Mastery: In 2025, CNQ deployed advanced "multilateral" wells in its heavy oil assets, drilling 182 net wells—a 50% increase over 2024—driving costs down to an industry-leading $18-$21/bbl.

- The "Albian" Strategy: By owning 100% of the Albian mines, CNQ has eliminated partner friction, allowing for seamless "debottlenecking" and 100%+ upgrader utilization.

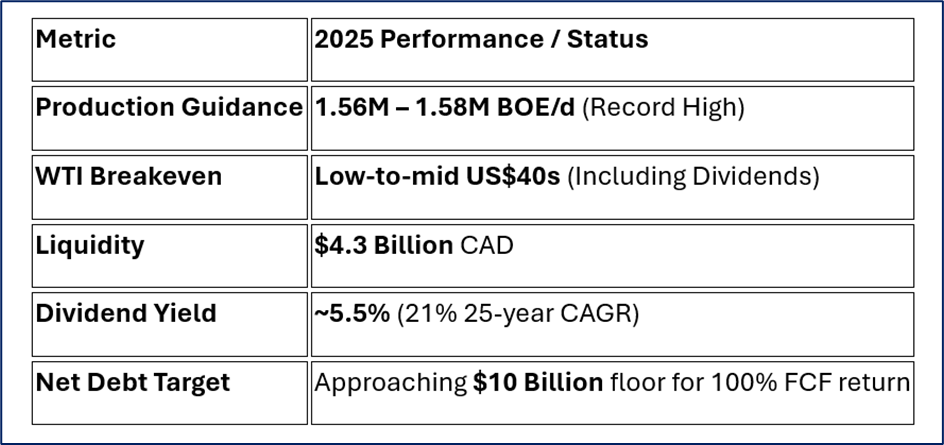

Financial & Operational Scorecard (Q4 2025 Update)

CNQ’s balance sheet is currently a fortress. Here are the hard numbers from the latest updates:

Source: Company Data

SWOT Analysis: The Unfiltered Reality

Source: Kalkine Group

Strengths

- Best-in-Class Costs: Operating costs for synthetic crude oil (SCO) hit $21.29/bbl in late 2025.

- Shareholder Alignment: A clear policy to return 60-100% of Free Cash Flow (FCF) to shareholders via buybacks and dividends.

- Asset Diversity: Massive footprint across natural gas, light oil, and bitumen provides a natural hedge.

Weaknesses

- Carbon Footprint: Despite an 18% reduction in intensity since 2020, oil sands remain a target for ESG-focused funds.

- Capital Intensity: While maintenance is low, "growth" projects like Carbon Capture (CCS) require billions in long-term spend.

Opportunities

- Natural Gas Renaissance: As LNG Canada ramps up, CNQ’s massive Montney and Duvernay gas assets are positioned for premium pricing.

- Technological Gains: AI-driven drilling and "length-normalized" well designs are cutting completion costs by 16% YoY.

Threats

- Regulatory Squeeze: Increasing federal carbon taxes ($15/tonne annual hikes) put pressure on margins.

- Takeaway Constraints: Projections suggest TMX capacity could be "full" by 2028 if production growth continues at this pace.

Risks to Watch

- Commodity Volatility: Without a significant hedging program, CNQ is "naked" to sudden drops in WTI prices.

- Labor Scarcity: Specialized human capital in the Fort McMurray region is becoming increasingly expensive.

- Wildfire Season: As seen in previous years, summer wildfires remain a persistent operational threat to production sites and pipelines.

Conclusion

Canadian Natural Resources’ 2.2% jump on December 30 isn't just a "green day" on the screen; it is a validation of their "drill-to-fill" strategy and the successful integration of recent massive acquisitions. With production at record highs and a breakeven price that allows them to thrive even in a slump, CNQ remains the definitive benchmark for the Canadian energy sector heading into 2026.

Please wait processing your request...

Please wait processing your request...