The copper market is heating up, and Capstone Copper (TSX: CS) is leading the charge. On December 30, 2025, the stock climbed ~1.9%, outperforming many of its peers in the mid-tier mining sector.

As the global energy transition accelerates, Capstone is no longer just a "promising junior"—it has transformed into a high-margin production powerhouse.

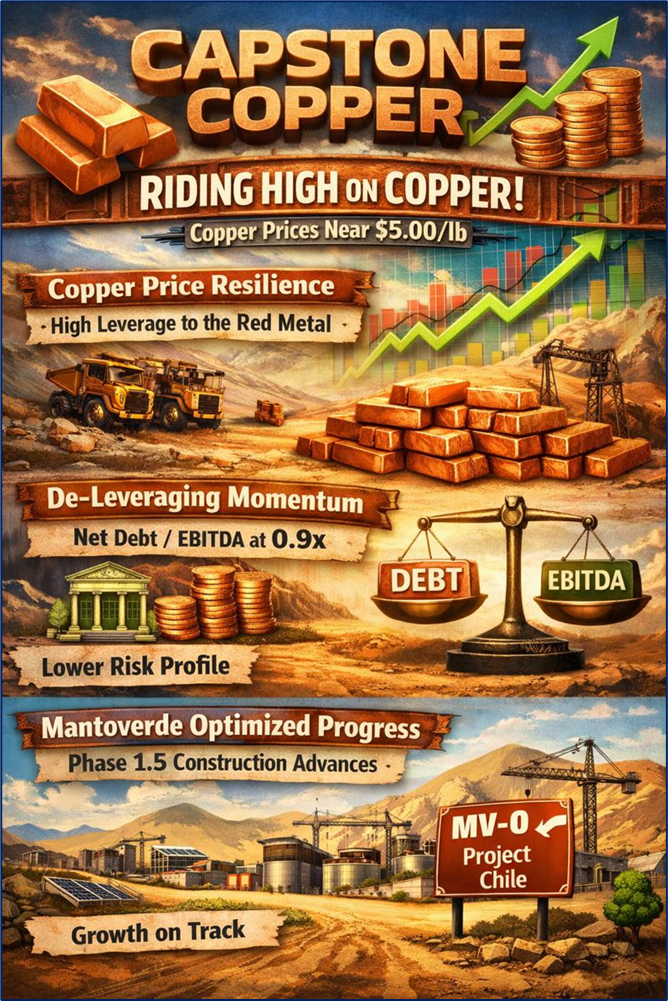

Key Drivers: Why the Stock Popped on Dec 30

The 1.9% gain wasn't a fluke; it was a reflection of several converging tailwinds:

Source: Kalkine Group

- Copper Price Resilience: With LME copper prices hovering near or above $5.00/lb, Capstone’s high leverage to the red metal makes it a primary beneficiary for investors looking for pure-play exposure.

- De-leveraging Momentum: Recent updates confirmed the company is aggressively paying down debt (Net Debt/EBITDA now at a lean 0.9x), significantly lowering the risk profile for institutional buyers.

- Mantoverde Optimized (MV-O) Progress: Reports indicating that construction on the MV-O project in Chile is hitting key milestones have boosted confidence in the company's "Phase 1.5" growth.

Latest Business Model & Strategy

Capstone’s 2025 business model is built on Scale, Jurisdiction, and Cost Reduction.

- Intermediate Producer Status: Moving away from small-scale mining to a consolidated 250,000+ tonne per year producer.

- Sulphide Focus: Shifting the mix toward sulphide concentrators (higher grade, lower cost) versus older cathode operations.

- District Integration: Leveraging the "Chilean Cluster"—sharing infrastructure between the Mantoverde and Santo Domingo sites to drive massive capital efficiencies.

Latest Financial & Operational Updates (Q3/Q4 2025)

Capstone recently reported record-breaking figures that have set the stage for a strong year-end:

- Record EBITDA: Q3 2025 Adjusted EBITDA reached $249.2 million, a staggering 106% increase year-over-year.

- Production Growth: Consolidated copper production is trending toward the 220,000–255,000 tonne range for the full year 2025.

- Cost Efficiency: C1 Cash Costs dropped to $2.42/lb, driven by the successful ramp-up of the new Mantoverde concentrator.

- Strategic Partnership: The entry of Orion Resource Partners into a 25% stake in Santo Domingo for up to $360 million has de-risked the funding for their next mega-project.

SWOT Analysis: The Deep Dive

Source: Kalkine Group

Risks to Watch

While the outlook is bullish, smart money is watching these red flags:

- Technical Execution: Any further delays in the "Mantoverde Optimized" ramp-up could dent the 2026 guidance.

- Macro Volatility: A global slowdown could cool copper demand, even if the "Green Energy" narrative remains strong.

- Arizona Water Issues: The Pinto Valley mine continues to face water constraints that may cap production upside in the US.

Conclusion

Capstone Copper has successfully navigated its "inflection point." By transitioning from a developer to a major producer with falling costs and rising volumes, the company is perfectly positioned for the "Copper Age." The 1.9% move on December 30 likely reflects the market realizing that Capstone is no longer just a "growth story"—it is now a cash-flow machine.

Please wait processing your request...

Please wait processing your request...