Celestica Inc. (TSX: CLS) delivered a stunning performance yesterday, November 24, 2025, surging nearly 15% to close at CAD 454.05. This move wasn't driven by a single press release but by a "perfect storm" of market factors re-igniting the stock's momentum.

1. Why Did the Stock Surge Yesterday?

The 14.95% spike on November 24 was driven by three converging catalysts:

- Sector-Wide AI Optimism: A broader rally in AI infrastructure stocks (like Broadcom and server makers) lifted the entire sector. Investors are rotating back into "pick-and-shovel" AI plays after a brief pullback, betting that hyperscaler spending (Google, Amazon, Meta) will accelerate in 2026.

- Analyst Validation: Major financial research firms, including Zacks, reiterated a positive view on Nov 24, highlighting Celestica's superior valuation compared to peers like Pinterest. This fresh coverage acted as a green light for institutional buying.

- Technical "Catch-Up": The stock had recently dipped approx. 15% from its highs in mid-November. Yesterday’s move was a classic "buy the dip" reaction, as value investors stepped in to capitalize on the discrepancy between the stock's lower price and its raised 2026 guidance.

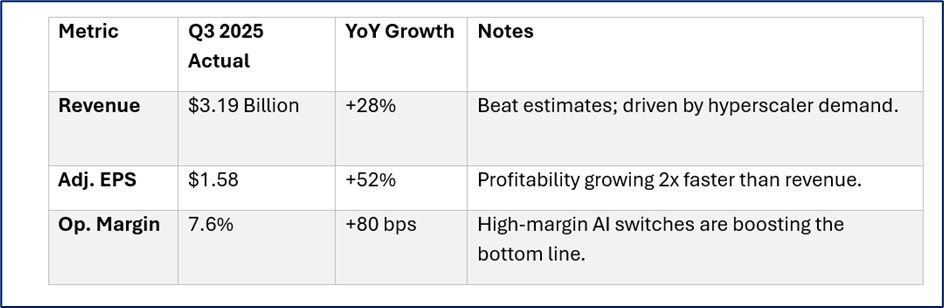

2. Financial & Operational Snapshot (Q3 2025)

Celestica is no longer just a contract manufacturer; it has successfully pivoted to becoming a high-value data center partner.

Source: Kalkine Group

Operational Highlights:

- CCS Segment (Connectivity & Cloud): Now accounts for 74% of total revenue. This segment builds the "backbone" of the internet—servers, storage, and networking switches for AI data centers.

- Hyper-Growth in HPS: The Hardware Platform Solutions (HPS) unit (where Celestica designs its own products rather than just assembling others') grew 79% YoY. This is the "crown jewel" of their business model because it carries much higher profit margins.

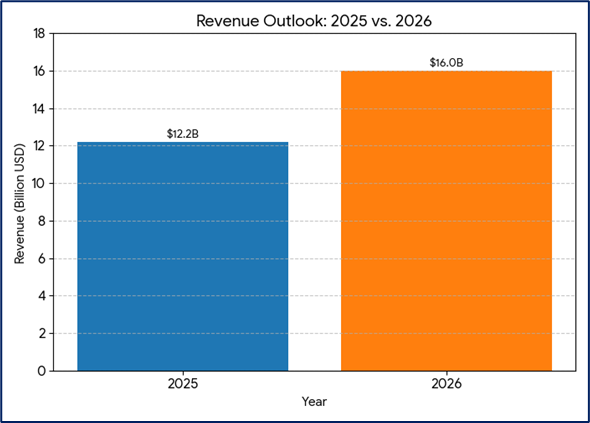

3.Future Guidance

Management has issued incredibly confident guidance, signaling they see no slowdown in AI spending.

- Full Year 2025 Outlook: Raised revenue to $12.2 Billion and Adj. EPS to $5.90.

- 2026 "Look Ahead": Projected revenue of $16.0 Billion with Adj. EPS of $8.20.

Source: Kalkine Group

4. Drivers, Risks & Business Model

Key Growth Drivers

- AI Infrastructure Cycle: Hyperscalers are upgrading to 800G (gigabit) switches to handle massive AI workloads. Celestica is a market leader in manufacturing these specific high-speed switches.

- Diversification: While still tech-heavy, their ATS Segment (Aerospace, Defense, Industrial) provides a stable, recession-resistant cash flow floor (approx. $3.2B annual revenue).

Critical Risks

- Customer Concentration: A massive portion of revenue comes from 2-3 top hyperscalers (likely Google and Amazon). If one cuts spending or switches vendors, the stock would crash.

- Valuation Premium: Trading at ~$450 CAD, expectations are sky-high. Any "slight miss" in future earnings could lead to a sharp sell-off (volatility risk).

- Trade Policy: With manufacturing hubs in Asia and Mexico, potential future tariffs (e.g., from US policy changes) could impact margins, though contracts typically allow them to pass these costs to customers.

5. Conclusion

Celestica has transformed from a low-margin assembler into a critical high-margin partner for the AI revolution. Yesterday's 15% surge confirms that the market believes the "AI Supercycle" is far from over. The company is trading on aggressive growth assumptions, but so far, they have executed flawlessly against them.

Source: Trading View, 24 Nov 2025

Please wait processing your request...

Please wait processing your request...