-Copy_02_05_2026_20_49_09_664366.jpg)

Is Celestica Inc. emerging as one of the most compelling AI-driven growth stories on the TSX in 2026? With blockbuster earnings, raised revenue guidance, and accelerating global AI infrastructure spending, Celestica has firmly landed on investors’ radar. But alongside the upside, volatility and concentration risks remain very real.

Key Takeaways – February 2026 Snapshot

- Is Celestica Stock Up Today?

CLS shares have shown sharp momentum with swings approaching +8% intraday as of 5 February 2026, reflecting both bullish sentiment and elevated volatility.

- Did Celestica Beat Earnings and Lift Guidance?

Yes. Q4 2025 EPS and revenue exceeded expectations, and management raised FY2026 revenue guidance to approximately US$17 billion. - Why Is CLS So Volatile Right Now?

Markets are weighing AI-led growth optimism against customer concentration and execution risks, particularly exposure to hyperscalers. - What Do Analysts Expect Next?

Consensus ratings skew Buy / Strong Buy, with average 12-month price targets implying meaningful upside from current levels. - Short vs Long-Term Outlook?

Near term: choppy but constructive.

Long term: structurally bullish if AI and cloud spending trends persist.

What Is Celestica Stock Doing Right Now? (February 5, 2026)

Celestica is trading with heightened momentum and wide price fluctuations, recently changing hands around C$370–405 (live prices may vary). The sharp moves follow:

- A clear earnings beat

- A raised full-year outlook

- Growing enthusiasm around AI data-centre hardware demand

At the same time, investors remain sensitive to headlines around hyperscaler dependency, which explains the sharp intraday swings despite strong fundamentals.

Can Celestica Outperform in the Current Global & Canadian Economic Backdrop?

Celestica’s trajectory is tightly linked to three macro layers: global AI demand, Canada’s economic setup, and broader TSX sector rotation.

Global AI & Technology Cycle

- Hyperscalers and enterprises continue to scale AI, cloud, and networking infrastructure

- This fuels demand for advanced hardware platforms and contract manufacturing, where Celestica has deep expertise

Canada Macro & TSX Context

- The TSX Composite’s balance of financials, energy, and exporters provides a stabilising backdrop for high-growth tech

- Profitable, globally exposed tech manufacturers are increasingly favoured

Currency Dynamics

- A weaker or volatile CAD vs USD can enhance export competitiveness but also add earnings translation noise

Together, these forces amplify both upside leverage and short-term volatility for CLS.

Industry Positioning: How Does Celestica Stack Up?

Within the electronics manufacturing services (EMS) and AI infrastructure supply chain, Celestica stands out:

- Faster revenue and EPS growth than many traditional EMS peers

- Premium valuation justified by AI, cloud, and data-centre exposure

- Strong execution record relative to industry averages

The trade-off? Higher expectations and lower tolerance for missteps.

Is Celestica Stock Bullish, Bearish, or Neutral?

Short-Term Outlook (3–6 Months)

- Bullish: Sustained AI server and cloud orders

- Neutral: Pullbacks on valuation or execution concerns

- Bearish risk: Any signal of hyperscaler order slowdown

Long-Term Outlook (12–36+ Months)

- Bullish: Structural AI, networking, and cloud growth

- Neutral: Cyclical moderation in enterprise spending

- Bearish risk: Loss or renegotiation of major customer contracts

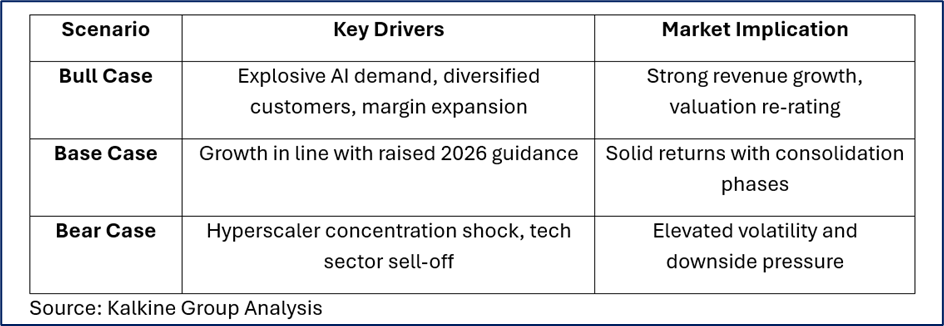

Scenario Analysis: Bull vs Base vs Bear

Analyst Sentiment & 12-Month Forecasts

- Ratings: Majority Buy / Strong Buy

- Target Prices: Wide dispersion, with bullish forecasts in the C$500–600+ range

- Interpretation: Strong conviction in long-term story, tempered by near-term execution risk

Business Model & Financial Momentum

Celestica operates as a global, high-value electronics manufacturing partner, with strengths in:

- AI and data-centre platforms

- Cloud and networking hardware

- Enterprise and communications systems

Recent highlights:

- Q4 2025 revenue growth ~44% YoY

- Raised FY2026 revenue outlook to ~US$17B

- Capex ramping toward ~US$1B to support demand

Key Risks Investors Should Monitor

- Heavy customer concentration among hyperscalers

- Cyclical swings in tech and cloud capex

- Macro slowdowns impacting enterprise IT budgets

- Currency volatility affecting CAD-reported results

Frequently Asked Questions (SEO-Friendly)

Is Celestica stock a buy in February 2026?

Analysts largely say yes, but suitability depends on risk tolerance and time horizon.

Does Celestica pay a dividend?

No. Returns are driven by capital appreciation, not income.

What’s driving the CLS rally?

AI infrastructure demand, earnings beats, and raised guidance.

Is valuation stretched?

Somewhat — reflecting growth expectations tied to AI momentum.

Final Verdict: Is Celestica a Fact-Driven Opportunity, Not Just AI Hype?

As of February 2026, Celestica sits at the crossroads of AI infrastructure expansion, hyperscaler capex cycles, and global supply-chain realignment. Its recent surge reflects real operational momentum, not speculative excess — but the market’s sharp reactions highlight just how sentiment-sensitive the stock has become.

The big picture:

- Strong fundamentals

- Powerful secular tailwinds

- Legitimate execution and concentration risks

Bottom line (informational only):

Celestica represents a high-quality, AI-levered TSX growth stock with compelling long-term upside, near-term volatility, and outsized sensitivity to earnings and AI spending headlines. That combination explains both the rally — and the turbulence — and is exactly why CLS remains one of the most talked-about Canadian tech stocks across global search, AI platforms, and social media right now.

Please wait processing your request...

Please wait processing your request...