CyberCatch Holdings (TSXV: CYBE) just delivered a massive holiday gift to shareholders, surging ~13.2% on December 24, 2025. After a volatile year, this sudden jump isn't random—it is the market finally digesting a slew of aggressive strategic pivots announced earlier this month.

Here is the analytical breakdown of why this micro-cap cybersecurity player is suddenly commanding attention, stripped of the corporate jargon.

Key Reasons & Drivers for the Surge

The +13.2% move is likely a delayed reaction to the 2nd December, Corporate Update, compounded by low-float dynamics and year-end "window dressing" by micro-cap funds.

Source: Kalkine Group

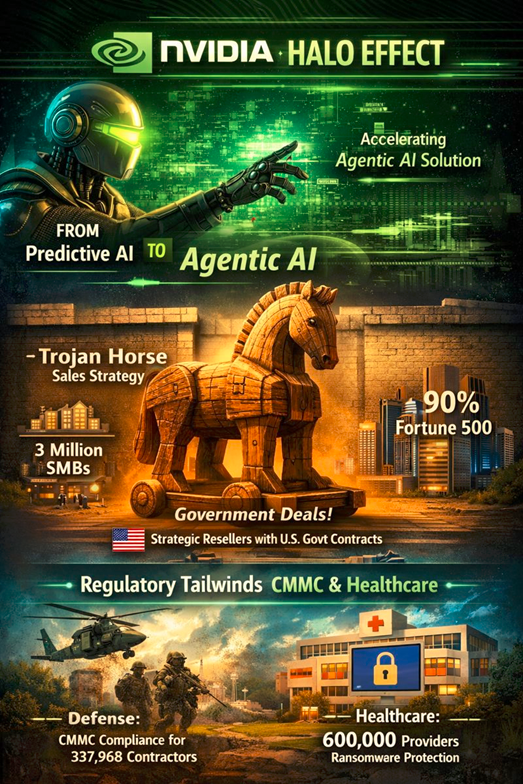

- The NVIDIA "Halo Effect"

CyberCatch officially joined the NVIDIA Inception Program. In the current market, mere association with NVIDIA’s ecosystem acts as a massive validation stamp.

- The Catalyst: They are using this partnership to accelerate their new "Agentic AI" solution.

- Why it matters: Investors are rotating out of "predictive AI" (old gen) into "agentic AI" (systems that act on threats, not just flag them).

- The "Trojan Horse" Sales Strategy

Instead of building a sales force from scratch (expensive/slow), CyberCatch unlocked a massive distribution channel.

- Deal: They teamed up with a global business decisioning/analytics giant (unnamed in snippets but described as a major player).

- Reach: This partner will market CyberCatch to 3 million SMBs and 90% of the Fortune 500.

- Govt Wins: Signed 3 strategic resellers who already hold large U.S. government contracts, bypassing the notoriously long federal sales cycle.

- Regulatory Tailwinds (CMMC & Healthcare)

- Defense Sector: Launched a specific solution for the 337,968 defense suppliers who must comply with new CMMC regulations. This is a "comply or die" market—companies must buy a solution to keep their government contracts.

- Healthcare: Rolled out a specialized compliance tool for 600,000 healthcare providers facing daily ransomware threats.

Strategic SWOT Analysis

Source: Kalkine Group

Strengths (Internal)

- AI-First Architecture: The platform uses a unique three-dimensional testing model (outside-in, inside-out, and social engineering) that is harder for legacy competitors to replicate.

- Partnership Leverage: Low Customer Acquisition Cost (CAC) model by piggybacking on resellers and insurance brokers.

- Insurance Hook: Unique "no-application" cyber insurance benefit for customers—a massive sweetener for SMBs who hate paperwork.

Weaknesses (Internal)

- Financial Fragility: Revenue bases have historically been low (~$400k CAD range in previous reports), with significant net losses (-$5M+ range).

- Balance Sheet: History of negative shareholder equity and dilution to fund operations.

- Micro-Cap Volatility: With a small float, a single large sell order can crush the stock just as fast as it rose.

Opportunities (External)

- Mandatory Compliance: The U.S. government (CMMC) and EU (NIS2) are effectively mandating CyberCatch's product category.

- Agentic AI Trend: If their beta "Agentic" solution works, they move from a "compliance tool" to an "active defense" tool, commanding higher pricing power.

- M&A Target: As they integrate with larger aggregators, they become a prime acquisition target for a larger legacy firm needing an AI refresh.

Threats (External)

- Execution Risk: Great press releases do not always equal great revenue. The "conversion rate" from their 3 million SMB partner channel is unproven.

- Dilution: The company may need to raise more cash to support this growth phase, potentially diluting the current 13% gain.

Latest Business Model: "SaaS + Insurance"

CyberCatch has pivoted from a standard SaaS tool to a Continuous Compliance Ecosystem.

- The Hook: "Root Cause" mitigation. They don't just patch holes; they test mandated controls continuously.

- The Upsell: Agentic AI. A new beta tier that doesn't just report risks but uses AI agents to actively mitigate them.

- The Moat: Integration with Cyber Insurance. By partnering with brokers to offer insurance benefits, they make the software "pay for itself" via premium reductions or exclusive access to coverage.

Financial & Operational Reality Check

- Operational: The company effectively transformed its R&D into a sales engine in Q4 2025. The focus shifted from "building" to "distributing" via the new strategic partners.

- Financials (The Sobering Part):

- While the stock is up, the underlying financials (based on last available data) showed a company burning cash to grow.

- Revenue: Historical revenue has been under $1M CAD/year. The "13% jump" is betting that the new partnerships will 10x this number in 2026.

- Profitability: Currently loss-making. The path to profitability relies entirely on the high-margin SaaS revenue from the new government and B2B channels kicking in immediately.

Key Risks to Watch

- Liquidity Risk: It is a TSX Venture stock. Volume can dry up instantly, making it hard to exit a position.

- The "News vs. Numbers" Gap: There is often a lag between announcing a partnership and seeing cash in the bank. If Q1 2026 numbers don't show revenue spikes, the stock could retrace.

- Tech Giants: Microsoft or CrowdStrike could release a "lite" compliance feature that renders standalone tools like CyberCatch obsolete for smaller SMBs.

Conclusion

CyberCatch (CYBE) is a high-risk, high-reward "derivative bet" on AI regulation.

The 13.2% jump isn't about what they earned today, but about the distribution pipes they opened for tomorrow. They have successfully aligned themselves with the three biggest trends of 2026: NVIDIA AI, Government Compliance (CMMC), and Cyber Insurance.

If the new partners convert even 1% of their 3 million SMBs, CyberCatch fundamentally changes its valuation bracket. If they don't, it remains a speculative micro-cap.

Please wait processing your request...

Please wait processing your request...