Denison Mines Corp. (TSX: DML) kicked off the 2026 trading year with a massive bang, surging approximately 9% on January 2nd. As the global energy transition places nuclear power at the center of the "Net Zero" narrative, Denison has positioned itself as a frontrunner in the Athabasca Basin.

But what exactly triggered this New Year’s rally? Here is a deep dive into the latest operational updates, the "construction-ready" status of their flagship project, and the risks that still lie beneath the surface.

The Catalyst: Why DML Surged 9% Today

The primary driver for today's price action was a major corporate announcement: Denison is officially ready to build.

On the morning of January 2, 2026, Denison reported it is prepared to make a Final Investment Decision (FID) and commence construction of its flagship Phoenix In-Situ Recovery (ISR) uranium mine. This follows the successful conclusion of the Canadian Nuclear Safety Commission (CNSC) public hearings in late 2025.

Key Drivers for the Jan 2 Rally:

Source: Kalkine Group

- Permitting Confidence: Final federal regulatory approvals are now expected in Q1 2026, removing the largest "red tape" hurdle for the project.

- Production Timeline Fixed: Management confirmed a two-year construction schedule, targeting first production by mid-2028.

- Engineering De-risking: The company revealed that 87% of project engineering is complete, significantly reducing the risk of technical delays during the build.

- Capital Cost Clarity: While costs have risen (see below), the market reacted positively to the transparency and the fact that the project remains highly profitable at current uranium spot prices.

Latest Business Model: From Developer to Producer

Denison’s business model has shifted from pure-play exploration to a de-risked development-to-production strategy.

- The ISR Advantage

Unlike traditional underground mining, Denison is pioneering the use of In-Situ Recovery (ISR) in the Athabasca Basin. This method involves pumping a solution into the ore body to dissolve uranium and then bringing it to the surface. It is significantly lower in capital and operating costs compared to conventional shaft mining.

- Physical Uranium Holding

Denison maintains a strategic "buffer" of physical uranium (approx. 2.2 million lbs). This serves as:

- Collateral for project financing.

- Exposure to rising spot prices while they wait for their own production to go online.

- Strategic Joint Ventures

In December 2025, Denison closed a major transaction with Skyharbour Resources, forming four joint ventures. This expands their "footprint" around the Wheeler River area, ensuring a pipeline of secondary projects like Waterbury Lake and McClean Lake.

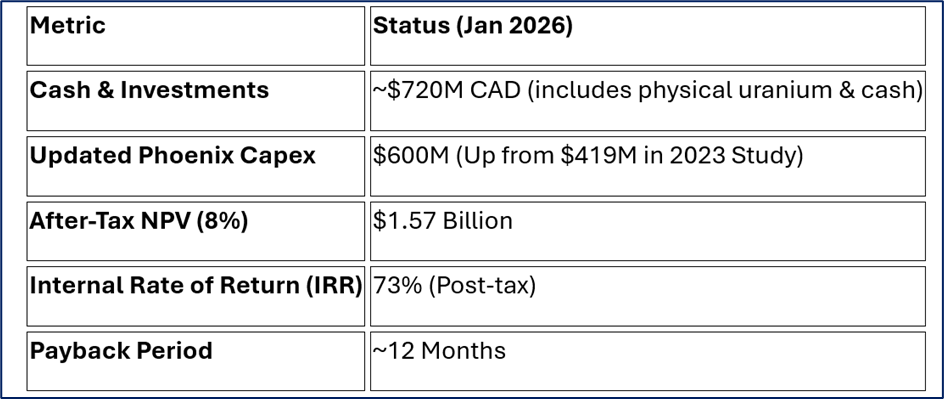

Operational & Financial Health Update

As of early 2026, Denison’s balance sheet is one of the strongest in the junior/mid-tier uranium space.

Source: Company Data

The capital cost for the Phoenix project rose to $600 million, a roughly 43% increase over the 2023 Feasibility Study. However, management noted that after adjusting for 2024–2025 inflation, the "real" increase is closer to 20%. The market seems to believe the high-grade nature of the ore can easily absorb these costs.

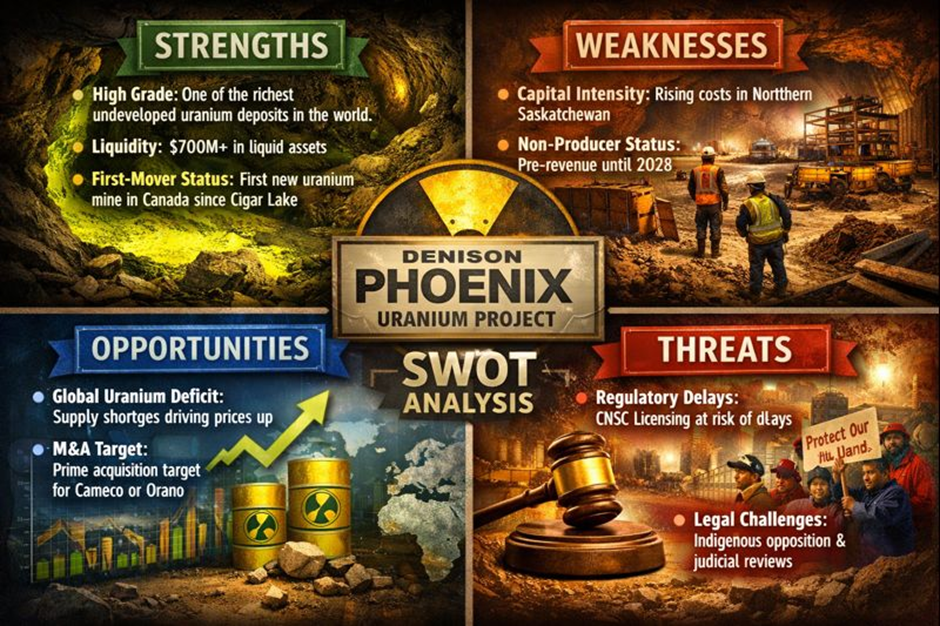

SWOT Analysis

Source: Kalkine Group

Strengths

- High Grade: Phoenix is one of the highest-grade undeveloped uranium deposits in the world.

- Liquidity: With over $700M in liquid assets, they are fully funded for the initial capital requirements.

- First-Mover Status: Poised to be the first new large-scale uranium mine in Canada since Cigar Lake.

Weaknesses

- Capital Intensity: Rising costs of labor and materials in Northern Saskatchewan.

- Non-Producer Status: Currently pre-revenue; the company is reliant on capital markets or asset sales until 2028.

Opportunities

- Global Uranium Deficit: Supply gaps from Kazakhstan and Niger are keeping spot prices at multi-year highs.

- M&A Target: As a "construction-ready" asset, Denison remains a prime acquisition target for majors like Cameco or Orano.

Threats

- Regulatory Delays: While expected in Q1, any delay in the final CNSC license would stall the 2028 production goal.

- Legal Challenges: The Peter Ballantyne Cree Nation has filed for a judicial review regarding project approvals; legal friction with Indigenous groups remains a critical watch-point.

Key Risks to Watch

- Technical Risk: ISR has never been used at this scale in the Athabasca Basin’s specific geology.

- Uranium Price Volatility: A sudden drop in spot prices would hurt the valuation of their physical holdings and the project's NPV.

- Indigenous Consultation: Maintaining the "Social License to Operate" is vital. While they have signed benefit agreements with several nations (including the Métis Nation-Saskatchewan), legal challenges from others could cause delays.

Conclusion

Denison Mines’ 9% jump isn't just a "dead cat bounce" or retail hype; it’s a reaction to the company reaching a terminal development milestone. By confirming construction readiness and securing a massive cash pile, Denison has transitioned from a speculative explorer into a "near-term" producer.

Investors are now pricing in the high probability that Denison will be the next major contributor to the global nuclear fuel supply chain.

Please wait processing your request...

Please wait processing your request...