Endeavour Silver (TSX: EDR) is capturing global headlines as a "silver squeeze" narrative and massive production growth converge. On January 9, 2026, the stock surged approximately 10%, a move fueled by a blockbuster 2025 production report and a historic supply-demand imbalance in the precious metals market.

Key Reasons and Drivers for the Jan 9 Surge

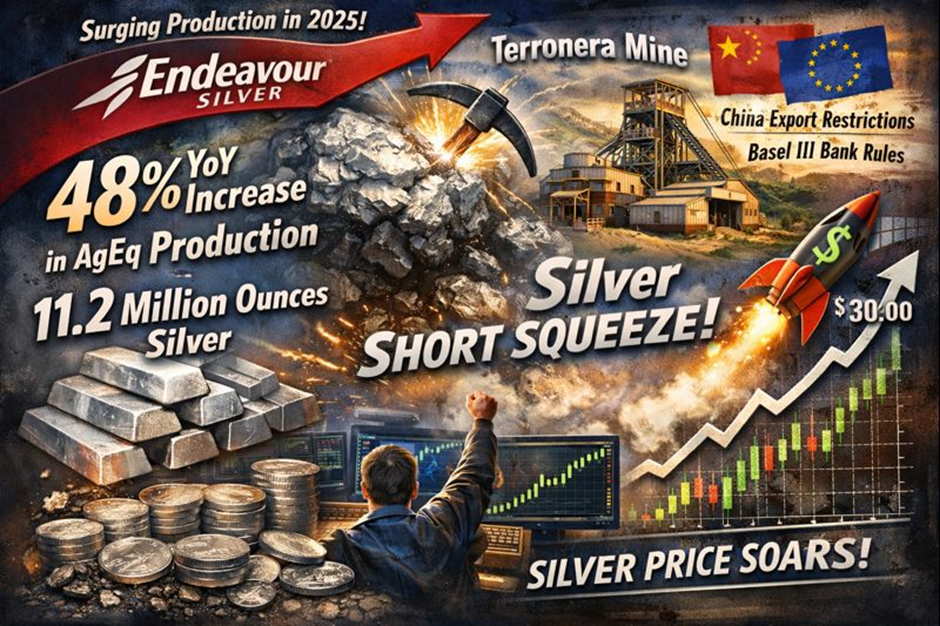

Source: Kalkine Group

The primary catalyst for the double-digit jump was the release of Endeavour’s full-year 2025 operational results. The company reported a staggering 48% year-over-year increase in silver equivalent (AgEq) production, totaling 11.2 million ounces. This massive growth was largely driven by the successful commercial ramp-up of the Terronera Mine, which hit its stride in late 2025.

Furthermore, a macro-driven "short squeeze" in the silver market—triggered by new Chinese export restrictions on silver and Basel III physical metal requirements for European banks—sent spot prices soaring, providing a powerful tailwind for high-beta miners like EDR.

Current Technical Analysis: The Breakout Paragraph

Source: Trading View

From a technical perspective, EDR has entered a high-momentum "Golden Star" phase. After consolidating near its 50-day moving average of C$12.00, the stock decisively broke through the C$14.50 resistance level on heavy volume. The Relative Strength Index (RSI) is currently hovering near 64, indicating the stock is nearing overbought territory, but the absence of a "pivot top" suggests the trend remains bullish. Traders are closely watching the C$15.88 fair value target; if the stock holds above the C$14.00 support level on a weekly close, the next psychological resistance is seen at C$18.00.

Latest Analyst Ratings: Upgrades and Targets

The sentiment on Bay Street and Wall Street has shifted aggressively toward "Strong Buy" in early 2026.

- CIBC World Markets: Upgraded EDR from Neutral to Sector Outperform with a price target of C$16.00, citing the de-risking of the Terronera project.

- National Bank of Canada: Recently raised its rating to Strong Buy, highlighting the company’s improved cash flow profile.

- BMO Capital Markets: Increased its price target to C$15.00, noting that the integration of the Kolpa mine is exceeding expectations.

- H.C. Wainwright: Reaffirmed a Buy rating, focusing on the massive leverage Endeavour has to rising silver prices compared to its peers.

Latest Business Model and Strategic Pivot

Endeavour Silver has successfully transitioned from a high-cost, aging producer to a growth-oriented mid-tier powerhouse. The business model now centers on "disciplined expansion," where cash flow from mature mines like Guanaceví funds the development of next-generation, high-margin assets. A critical component of this strategy was the US$350 million convertible note offering completed in December 2025, which allowed the company to retire expensive third-party debt and fully fund the Pitarrilla project, one of the world’s largest undeveloped silver resources.

Financial and Operational Update: 2025 Retrospective

- Record Production: Produced 6.49 million oz of silver and 37,164 oz of gold in 2025.

- Terronera Impact: The mine contributed 3.8 million AgEq ounces in Q4 alone, proving it is the company's new flagship asset.

- Asset Optimization: Endeavour signed a definitive agreement to sell the Bolañitos mine for US$40 million to streamline operations and focus on higher-grade core assets.

- Liquidity Boost: Ending 2025 with a significantly strengthened balance sheet, showing a quick ratio of 2.38 and a focus on shifting to higher-grade mining areas by H2 2026 to further lower All-In Sustaining Costs (AISC).

Risk Factors to Monitor

Despite the euphoria, several risks remain for EDR investors.

- Operational Execution: Any technical setbacks in the high-grade transition scheduled for late 2026 could impact earnings.

- Metals Volatility: Silver is notoriously volatile; a "flash crash" in broader tech markets often triggers margin calls that force liquidations in precious metals.

- Jurisdictional Risk: Ongoing changes to Mexican mining laws and environmental regulations continue to pose a long-term regulatory hurdle.

- Dilution Concerns: While the convertible debt helped clean up the balance sheet, it represents potential future dilution if the share price continues to climb.

Conclusion

Endeavour Silver’s 10% surge on January 9, 2026, is a reflection of a company hitting its operational "sweet spot" at the exact moment the global silver market is starving for physical supply. With Terronera online and Pitarrilla in the wings, EDR has transformed its fundamental profile. While the technicals suggest a short-term cooling period may be healthy, the long-term narrative of record production and debt reduction has made it a favorite for institutional and retail investors alike.

Please wait processing your request...

Please wait processing your request...