The mining sector is electrified as Endeavour Silver (TSX: EDR) registered a massive ~15% gain on January 5, 2026. While the broader TSX Composite started the year on a positive note, Endeavour’s outperformance signals a "perfect storm" of fundamental breakthroughs and macroeconomic tailwinds.

From the long-awaited ramp-up of the Terronera flagship to a geopolitical shockwave in South America, here is the analytical breakdown of why EDR is the talk of the retail trading desk today.

The "Big Three" Drivers Behind the Jan 5 Spike

Source: Kalkine Group

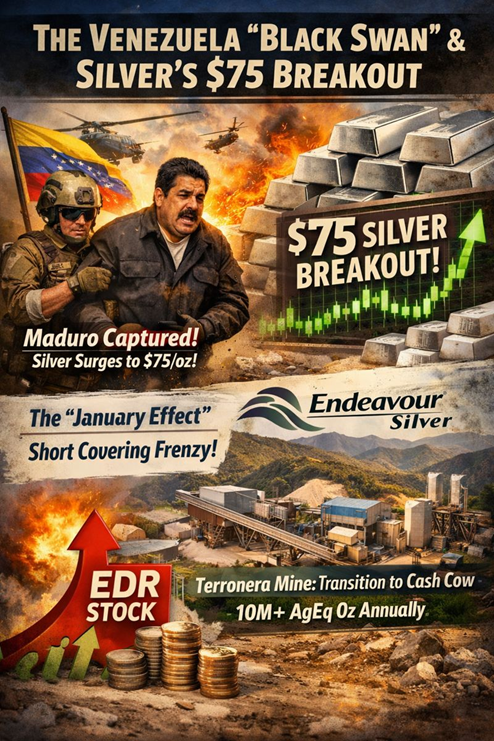

- The Venezuela "Black Swan" & Silver’s $75 Breakout

The primary catalyst for the 15% jump wasn't just internal; it was global. Over the weekend of January 4, 2026, a U.S. military raid in Venezuela resulting in the capture of Nicolas Maduro sent shockwaves through the commodities market.

- Safe-Haven Demand: Spot silver surged over 4% to cross $75/oz on Monday morning.

- Leverage: As a "pure-play" silver producer, Endeavour Silver historically trades with a high beta to the metal. When silver moves 4%, EDR often moves 10–15% due to its operational leverage.

- Terronera Milestone: Transition to Cash Cow

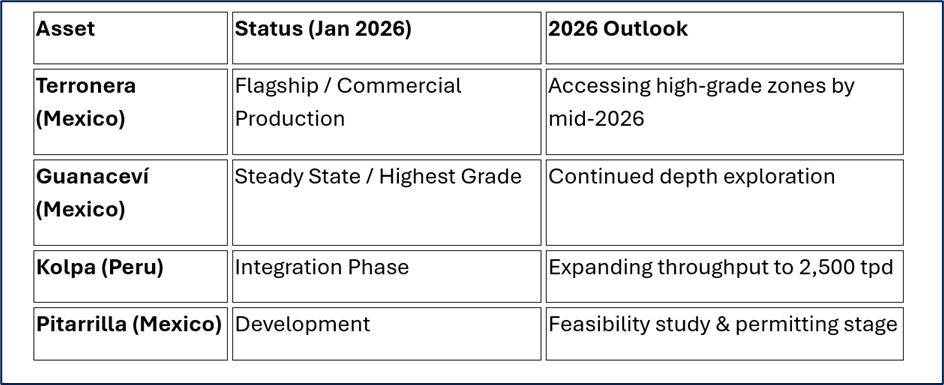

Endeavour confirmed that its Terronera mine in Jalisco, Mexico, is now operating at 90% nameplate capacity.

- For years, Terronera was a "capital sink." As of January 2026, it has officially transitioned into a free cash flow generator.

- Management is expected to release its 2026 Consolidated Guidance this month, with analysts anticipating a massive jump in silver equivalent (AgEq) production toward the 10 million ounce annual goal.

- The "January Effect" & Short Covering

After missing Q3 2025 earnings due to derivative losses, EDR saw significant tax-loss selling in late December. Today’s move represents a classic "January Effect" where institutional and retail buyers return to high-growth names, compounded by short-sellers being forced to cover positions as the $75/oz silver floor holds firm.

Business Model & 2026 Operational Update

Endeavour Silver has evolved from a high-cost, aging asset manager into a modernized mid-tier producer.

Latest Business Model Focus:

- Portfolio Optimization: In late 2025, the company signed a definitive agreement to sell the high-cost Bolañitos mine for $50 million, streamlining its focus on high-margin assets.

- Geographic Diversification: The 2025 acquisition of the Kolpa Mine in Peru is now fully integrated, adding base metal (Lead/Zinc) credits that significantly lower "All-In Sustaining Costs" (AISC).

Source: Company Data

Latest Financial Health

- The $350M War Chest: In December 2025, Endeavour completed a $350 million convertible note offering. This move fortified the balance sheet, allowing the company to pay down high-interest debt and fund the 2026 Pitarrilla feasibility study without further diluting shareholders through equity raises.

- Margin Expansion: With silver prices at $75 and AISC trending toward $18–$22/oz at Terronera, the company's profit margins are currently at historic highs.

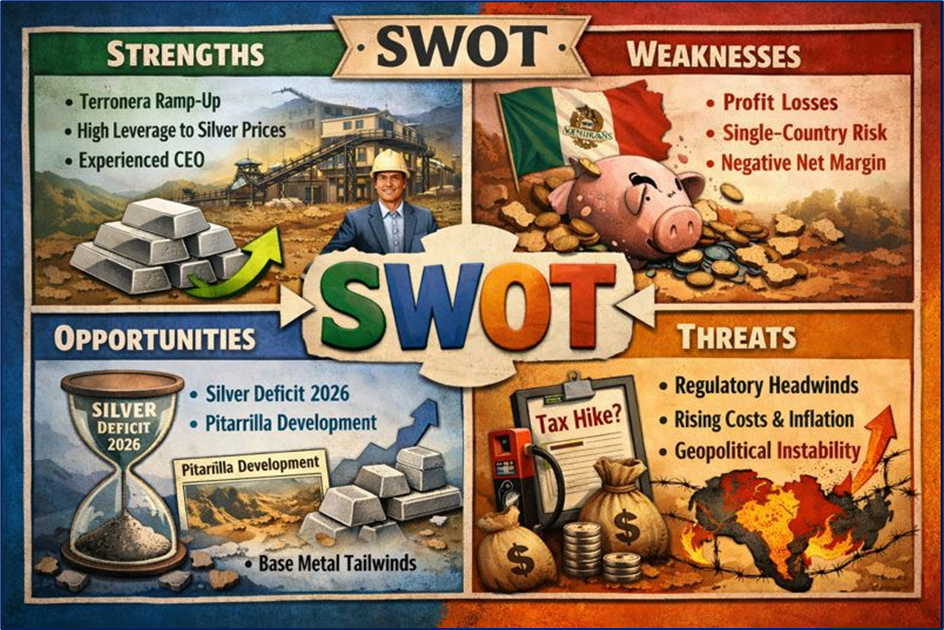

SWOT Analysis: Endeavour Silver 2026

Source: Kalkine Group

Strengths

- Terronera Ramp-up: Transitioned from developer to producer.

- High Leverage: One of the most sensitive stocks to silver price increases.

- Management Continuity: CEO Dan Dickson has successfully navigated the capital-intensive construction phase.

Weaknesses

- Historical Profitability: Recent quarters saw losses due to poor hedging/derivatives timing.

- Single-Country Risk: Heavy reliance on Mexican mining regulations (which have been volatile).

- Negative Net Margin: Still working through the financial "hangover" of construction costs.

Opportunities

- Silver Deficit: 2026 is projected to be the 5th consecutive year of silver supply deficits.

- Pitarrilla Development: One of the world’s largest undeveloped silver deposits provides a long-term growth "tail."

- Base Metal Tailwinds: Increased Lead/Zinc prices from the Kolpa mine.

Threats

- Regulatory Headwinds: Potential for increased mining taxes in Mexico.

- Inflation: Rising labor and energy costs in Latin America could eat into margins.

- Geopolitical Instability: While the Venezuela crisis boosted prices, regional instability can disrupt supply chains.

Key Risks to Watch

Despite the 15% rally, investors should monitor:

- The $75 Support Level: If the "Venezuela premium" fades and silver drops back toward $60, EDR could give back today’s gains just as quickly.

- Operational Hiccups: Terronera is in its first full year of commercial production; any technical downtime would be a major setback.

- Convertible Dilution: The $350M debt issued in Dec 2025 is "convertible," meaning if the stock hits certain price targets, new shares will be issued, potentially capping the upside.

Conclusion

The 15% surge on January 5, 2026, is a reflection of Endeavour Silver finally "crossing the chasm" from a risky developer to a major cash-flow producer. While the geopolitical chaos in Venezuela provided the spark, the fuel was the successful ramp-up of Terronera and a cleaned-up balance sheet. As the company prepares to release its 2026 guidance later this month, the market is betting that the "new" Endeavour is a leaner, more profitable beast than the one of years past.

Please wait processing your request...

Please wait processing your request...