Endeavour Silver (TSX: EDR): The 8% Surge and the Road to 15.6 Million Ounces

Endeavour Silver Corp. (TSX: EDR) commanded the spotlight on the Toronto Stock Exchange on January 22, 2026, as its share price surged by 8%, marking a decisive breakout amid a broader rally in the precious metals sector. This sudden vertical movement represents more than just market sentiment; it is the culmination of a fundamental transformation as the company transitions from a mid-tier miner into a significantly larger, more diversified producer.

Driven by a combination of surging global silver prices, which recently crossed the $95 mark, and the highly anticipated ramp-up of the flagship Terronera project, Endeavour is currently navigating a "pivotal turning point" that has reignited investor appetite for silver-leveraged equities.

Latest Drivers and Reasons for the Surge

Source: Kalkine Group

The immediate catalyst for the January 22nd rally is the convergence of macro-economic tailwinds and company-specific execution. Silver has reclaimed its role as a premier safe-haven asset, buoyed by geopolitical instability and its recent inclusion in the U.S. Critical Minerals List, which has fundamentally altered its demand profile. Specifically for Endeavour, the market is reacting to the successful commissioning and commercial production status of the Terronera mine, which is now entering its first full year of operation. Furthermore, the stock's momentum was amplified by recent analyst upgrades from major firms like BMO Capital and B. Riley, who raised their price targets citing improved growth visibility and "clean" operational quarters.

Current Business Model and Portfolio

Endeavour Silver operates on a model of high-grade underground mining with a focus on organic growth and strategic asset rotation. The company recently streamlined its portfolio by divesting non-core assets to focus on its highest-margin opportunities. Its current operational base rests on three primary pillars:

- Guanaceví (Mexico): A long-standing, high-grade silver-gold mine that remains a consistent cash-flow generator.

- Terronera (Mexico): The company’s new "primary growth engine," designed to be a low-cost, high-output silver-gold operation.

- Kolpa (Peru): A recently acquired and integrated asset that provides geographic diversification and introduces significant base metal credits (Lead, Zinc, Copper) to the production mix.

Latest Financial, Operational, and Dividend Updates

In a significant news release on January 16, 2026, Endeavour provided its consolidated 2026 guidance, outlining a transformative year ahead. The company projects silver production to range between 8.3 and 8.9 million ounces, with total silver equivalent (AgEq) production reaching 14.6 to 15.6 million ounces (Endeavour Silver News Release, Jan 16, 2026). This follows a record 2025 performance where the company produced 11.2 million AgEq ounces.

Operationally, the company completed the sale of the Bolañitos Mine on January 15, 2026, for US$40 million plus contingent payments, allowing management to redirect resources toward the massive Pitarrilla development project. On the financial front, Endeavour bolstered its liquidity through a US$350 million convertible note offering in late 2025, ensuring the balance sheet is well-funded for its $157.8 million 2026 capital budget. While the company currently prioritizes growth capital over dividends, the transition to lower consolidated cash costs ($12.00–$13.00/oz) is intended to build the long-term value necessary for future shareholder returns (Endeavour Silver News Release, Jan 15, 2026).

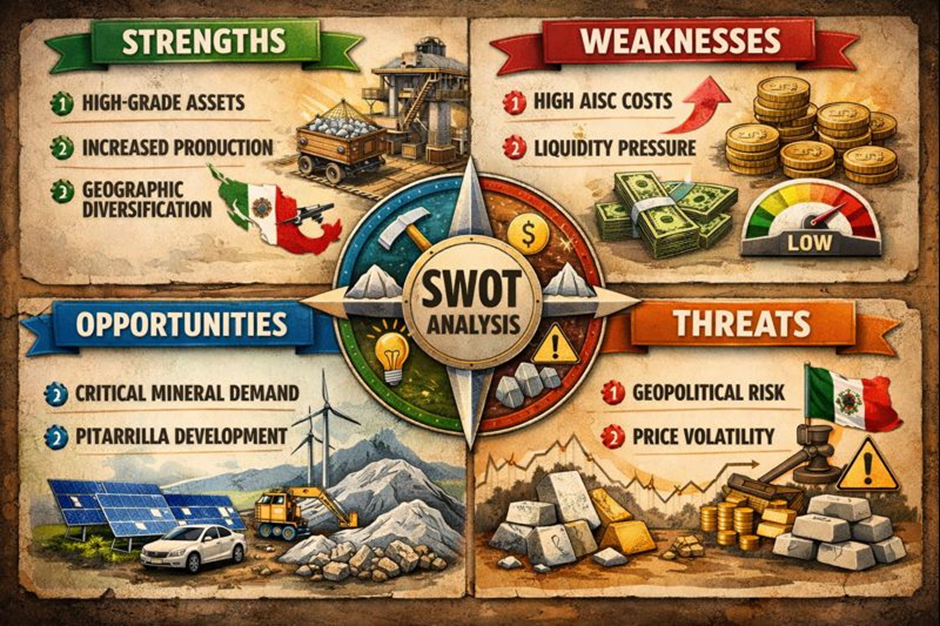

Latest SWOT Analysis

Source: Kalkine Group

Strengths

- High-Grade Asset Base: Focus on high-grade deposits like Guanaceví and Pitarrilla ensures efficient production.

- Operational Scale: The ramp-up of Terronera and integration of Kolpa nearly doubles previous production capacities.

- Geographic Diversification: Expansion into Peru with the Kolpa acquisition reduces reliance on Mexican jurisdiction alone.

Weaknesses

- Cost Sensitivity: Despite lower cash costs, All-In Sustaining Costs (AISC) remain sensitive to inflationary pressures in Mexico and Peru.

- Liquidity Ratios: High capital expenditure for growth has historically kept current and quick ratios under pressure.

Opportunities

- Critical Mineral Status: Silver’s role in the green energy transition and its U.S. Critical Mineral status creates a long-term demand floor.

- Pitarrilla Development: One of the world’s largest undeveloped silver deposits provides a multi-decade growth runway.

Threats

- Geopolitical Risk: Significant concentration in Mexico exposes the company to changing mining laws and tax duties.

- Price Volatility: As a primary silver producer, the company’s margins are highly leveraged to volatile spot prices of silver and gold.

Outlook and Risks

The outlook for Endeavour Silver for the remainder of 2026 is defined by "execution and scale." Management expects consolidated cash costs to decline as higher-grade areas are accessed in the second half of the year. The focus will remain on the Pitarrilla project, where a US$48 million growth budget is earmarked to define high-grade mineralized structures. However, risks persist; the company’s AISC is projected to range between $27.00 and $28.00 per ounce, which leaves a narrow margin if silver prices face a sharp correction. Additionally, the reliance on diesel power at Terronera until a permanent LNG plant is operational represents a temporary but significant operating expense.

Compelling Conclusion

Endeavour Silver’s 8% surge on January 22 is a clear signal that the market is beginning to price in the company's new identity as a senior-tier producer. By successfully transitioning the Terronera project into a cornerstone asset and strategically divesting older mines like Bolañitos, the company has effectively "de-risked" its growth profile while maximizing its leverage to the current silver bull market. As the mining sector continues to hunt for scale and high-grade reserves, Endeavour’s aggressive 15.6 million ounce target for 2026 positions it as a dominant player in the silver space, provided it can navigate the inherent cost and political volatilities of the Latin American mining landscape.

Please wait processing your request...

Please wait processing your request...