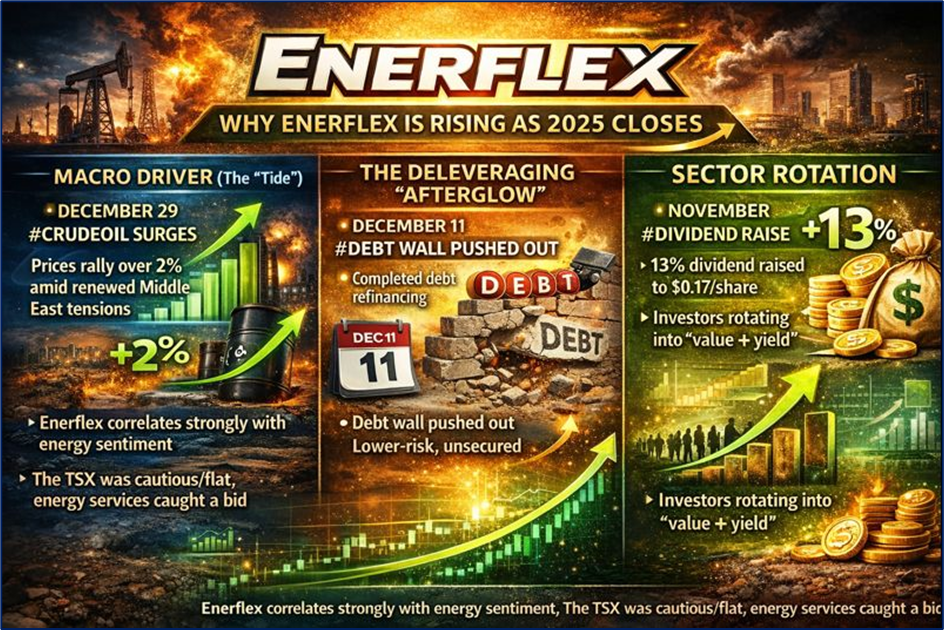

The Pulse: Why Enerflex Jumped ~1.73% on Dec 29

While a 1.73% move might look like standard noise, yesterday’s green candle for Enerflex wasn't an isolated event—it was a confirmation of broader sector strength intersecting with company-specific tailwinds.

Source: Kalkine Group

- Macro Driver (The "Tide"): On December 29, crude oil prices rallied over 2% amid renewed geopolitical tensions and risks of supply disruptions in the Middle East. As a critical service provider for gas compression and processing, Enerflex correlates strongly with energy sentiment. While the broader TSX was cautious/flat, energy services caught a bid.

- The Deleveraging "Afterglow": The market is still digesting the December 11, 2025 completion of Enerflex's debt redemption (redeeming 9.00% 2027 notes). By refinancing with lower-risk unsecured notes due in 2031, they have successfully pushed their "debt wall" out, removing a major overhang that suppressed the stock earlier in the year.

- Sector Rotation: As 2025 closes, investors are rotating into "value with yield." With Enerflex raising its dividend by 13% in November, it has become a prime target for portfolios seeking defensive growth heading into 2026.

The Engine: Latest Business Model (2025)

Enerflex has fundamentally changed its identity. It is no longer just a "fabrication shop" subject to boom-and-bust oil cycles.

1. Energy Infrastructure (EI) – The "Utility" Layer

- Model: Build-Own-Operate-Maintain (BOOM). Enerflex builds the plant, owns it, and sells the capacity to the client on long-term contracts.

- Status: This segment now provides stable, recurring cash flow that covers the dividend.

- Key Regions: Heavy footprint in the Middle East (Oman, Bahrain) and Latin America.

2. Engineered Systems (ES) – The "Cash Cannon"

- Model: Modular gas processing and compression units sold directly to customers.

- 2025 Update: Focusing on high-complexity projects (like the Cryogenic gas processing facility awarded in the Permian).

- Backlog: Sitting at a robust $1.1 Billion (as of Q3), providing clear revenue visibility through 2026.

3. After-Market Services (AMS)

- Model: Parts, maintenance, and overhauls.

- Role: The "sticky" revenue. Once Enerflex equipment is installed, they service it for decades.

The Pivot: In 2019, recurring revenue was small. Today, EI and AMS combined generate roughly 60%+ of Gross Margin, effectively putting a "floor" under the stock price during volatile oil prices.

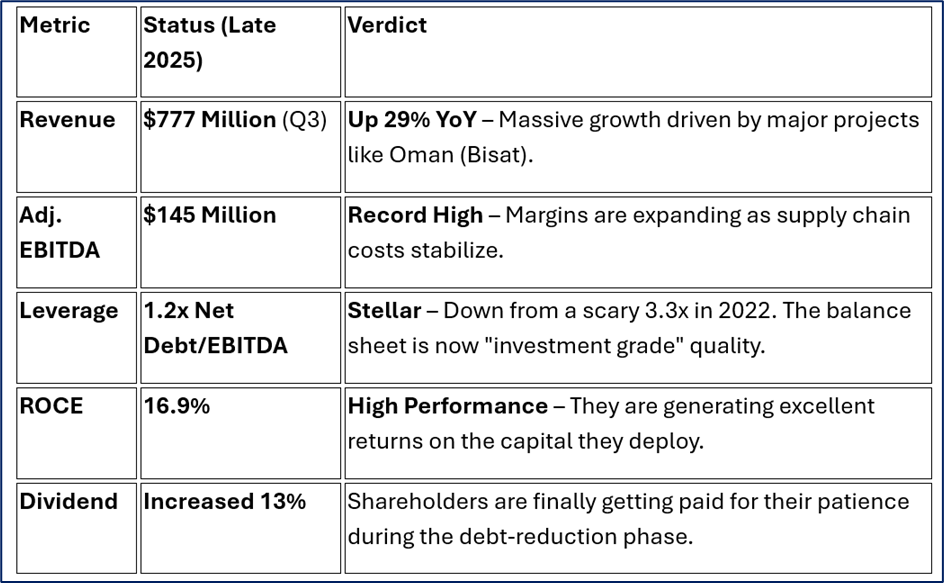

The Scorecard: Q3/Q4 2025 Financial & Operational Update

Source: Company Data

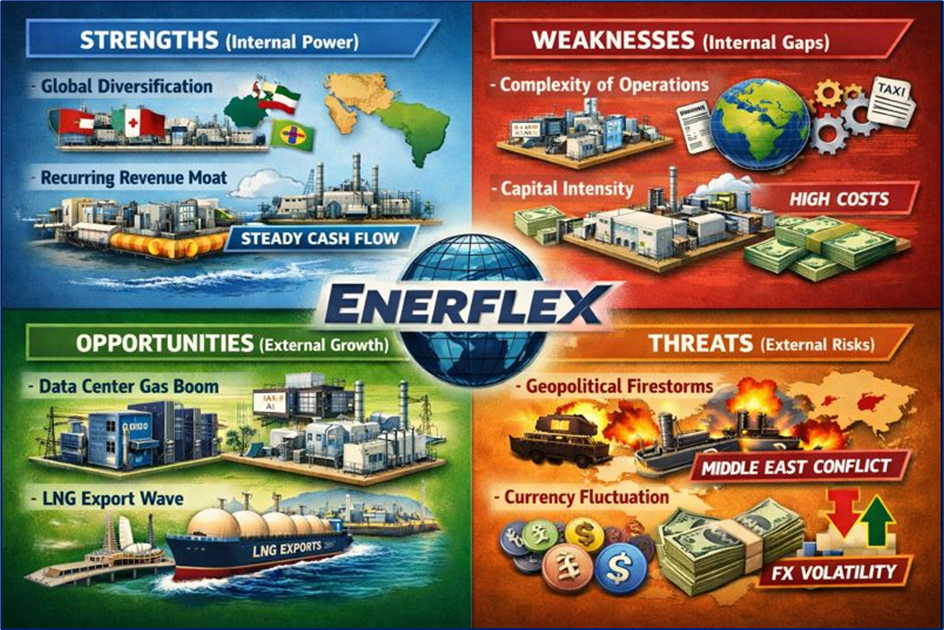

SWOT Analysis

Source: Kalkine Group

Strengths (Internal Power)

- Global Diversification: Unlike peers focused solely on the Permian Basin (US), Enerflex dominates in niche international markets (Oman, Bahrain, Brazil) where competition is lower and margins are higher.

- Recurring Revenue Moat: The shift to "Energy Infrastructure" means they get paid even if drilling slows down, provided gas keeps flowing.

- Modular Tech Leadership: Their ability to pre-fabricate gas plants reduces on-site construction risk, a massive advantage in remote regions.

Weaknesses (Internal Gaps)

- Complexity of Operations: Operating in multiple jurisdictions (Middle East, LATAM, North America) creates high overhead and complex tax/compliance structures.

- Capital Intensity: The BOOM model requires massive upfront capital (building the plant before getting paid), which can strain free cash flow during growth spurts.

Opportunities (External Growth)

- The "Data Center" Gas Boom: AI and data centers need massive power. Natural gas is the bridge fuel. Enerflex is perfectly positioned to build the "behind-the-meter" power generation infrastructure for these tech hubs.

- LNG Export Wave: As North American LNG exports double by 2030, the demand for upstream compression (to get gas to the coast) will remain secularly high.

Threats (External Risks)

- Geopolitical Firestorms: A significant portion of revenue comes from the Middle East. Any conflict expansion there could disrupt operations or spook investors.

- Currency Fluctuation: Earnings are reported in USD/CAD but collected in various currencies, creating FX headwinds.

The Risks: What Could Break the Thesis?

- Fixed-Price Contracts: In their Engineered Systems division, if inflation spikes again, they could be trapped in fixed-price contracts that bleed margins (though they have improved hedging here).

- Customer Concentration: In international markets, they often rely on National Oil Companies (NOCs). Losing a relationship with a player like OQ (Oman) would be catastrophic.

- Interest Rates: While they deleveraged, the BOOM model is debt-heavy. If rates stay "higher for longer" into 2026, the cost of funding new infrastructure projects increases, squeezing returns.

Conclusion: The "Silent Winner" of 2025

Enerflex’s 1.73% rise on December 29 isn't just about a good day for oil; it’s recognition of a successful turnaround.

For years, the market penalized EFX for high debt and a messy acquisition (Exterran). In late 2025, that narrative is dead. The debt is gone (down to 1.2x), the "bad" contracts are worked off, and the dividend is growing.

They are no longer just an "oil services" company; they are an energy infrastructure utility trading at an industrial multiple. If natural gas remains the baseload fuel for the AI/Electrification era, Enerflex is arguably one of the most undervalued plays on the TSX.

Bottom Line: The chart looks technical, but the fundamentals are structural.

Please wait processing your request...

Please wait processing your request...