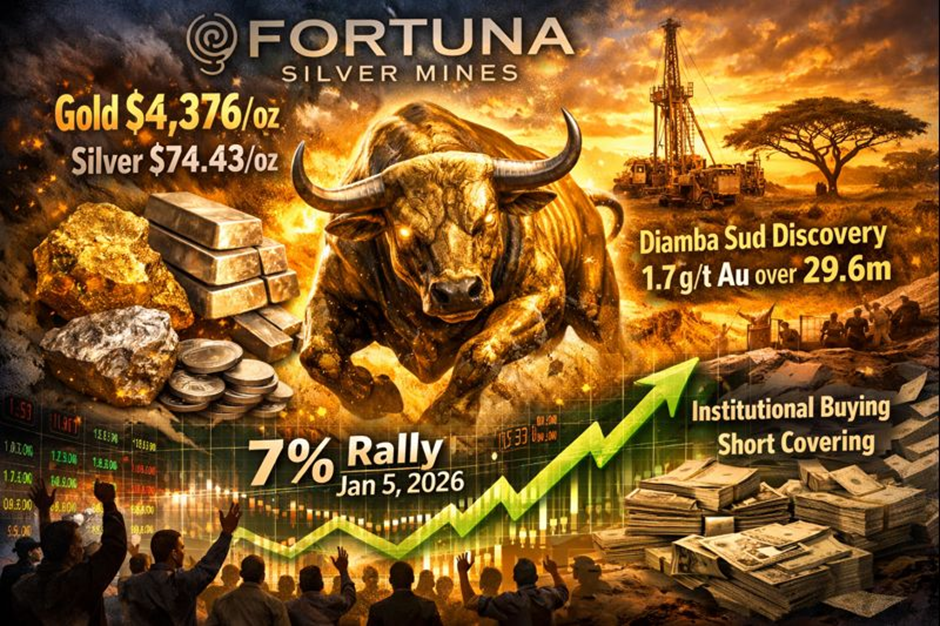

Fortuna Mining Corp. (TSX: FVI) kicked off the first full trading week of 2026 with a powerful 7% jump on January 5, defying the broader market's cautious start to the year. As gold prices hover near historic highs of $4,375/oz, the mid-tier producer is successfully rebranding itself from a silver-heavy play to a high-margin gold powerhouse.

Below is a deep-dive analytical breakdown of the drivers, financial health, and strategic pivot fueling this momentum.

Key Drivers: Why the Jan 5 Spike?

Source: Kalkine Group

The ~7% rally on January 5, 2026, was primarily fueled by a "perfect storm" of macro tailwinds and company-specific execution:

- Surging Precious Metals: Spot gold surged to $4,376/oz and silver reached $74.43/oz by the morning of Jan 5. Fortuna’s high operational leverage means every dollar increase in gold prices disproportionately boosts its bottom line.

- West African Momentum: Late December drill results from the Diamba Sud project in Senegal (including 1.7 g/t Au over 29.6 meters) have solidified investor confidence ahead of the Definitive Feasibility Study (DFS) due in H1 2026.

- Short Covering & Institutional Rebalancing: Following a 2.7% dip on Jan 2, the Jan 5 rally saw significant "buying the dip" from institutional players who have recently increased their stake to roughly 45% of the float.

Latest Business Model: The "Gold Pivot"

Fortuna has undergone a radical transformation. Once known as "Fortuna Silver," the company's 2026 business model is built on three pillars:

- High-Margin Gold Dominance: The Séguéla Mine in Côte d’Ivoire is now the crown jewel. With a mill expansion underway to reach 2.5 million tonnes per annum, it is on track to produce 160,000–180,000 oz of gold in 2026 at an industry-leading AISC (All-In Sustaining Cost) below $1,300/oz.

- Asset Optimization: The company successfully divested non-core, high-cost silver assets (like San Jose in Mexico) in 2025, shifting capital toward lower-risk, higher-return jurisdictions.

- Tier-1 Pipeline: The business model now relies on "organic growth" rather than expensive M&A, with Diamba Sud (Senegal) expected to reach a Final Investment Decision (FID) by mid-2026.

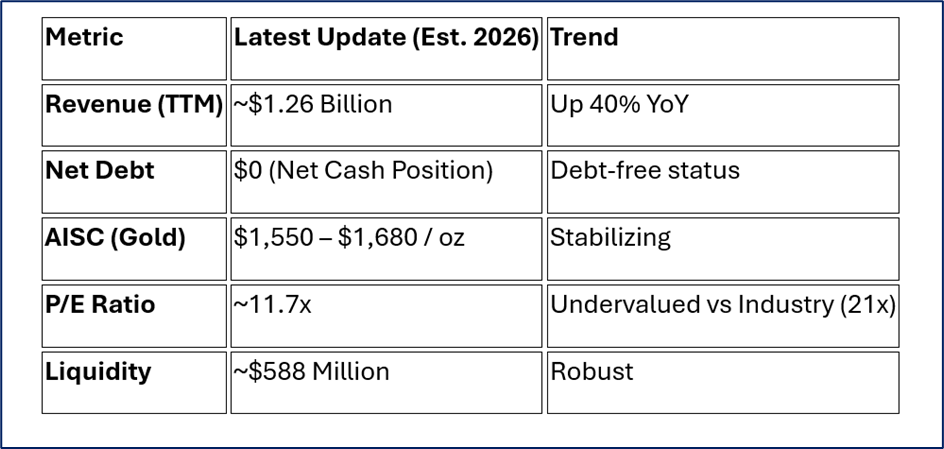

Financial & Operational Health Check

Source: Company Data

SWOT Analysis (2026 Outlook)

Source: Kalkine Group

Strengths

- Zero Net Debt: A rare feat for a mid-tier miner, providing massive flexibility for expansion.

- Low-Cost Production: Séguéla’s low AISC acts as a "margin shield" if gold prices soften.

- Diversification: Balanced portfolio across West Africa (Côte d'Ivoire, Senegal, Burkina Faso) and Latin America (Argentina, Peru).

Weaknesses

- Jurisdiction Risk: High concentration in West Africa and Argentina exposes the company to sudden regulatory or geopolitical shifts.

- Revenue Decline (Temporary): Divesting older silver mines has caused a slight dip in total silver volume as the company ramps up gold.

Opportunities

- Diamba Sud Construction: A positive FID in H1 2026 could trigger a massive re-rating of the stock.

- Silver Recovery: If silver hits the projected $100/oz mark, Fortuna’s remaining silver assets in Peru (Caylloma) become "cash cows."

- Mill Expansion: Increasing Séguéla's throughput will drive further economies of scale.

Threats

- Cost Inflation: Rising costs for cyanide, fuel, and labor could compress margins.

- Social License: Community unrest in Latin America remains a persistent risk for the mining sector.

- Gold Volatility: A "hawkish" pivot by central banks could cool the record-breaking gold rally.

Key Risks to Monitor

- The "2026 Production Cliff": Analysts are watching to see if Diamba Sud can come online fast enough to offset depleting older reserves.

- West African Stability: Recent geopolitical shifts in the Sahel region require close monitoring for any impact on the Yaramoko or Séguéla operations.

- Insider Selling: Recent CFO and COO stock sales in late 2025 have raised some eyebrows, though they were largely attributed to tax planning.

Conclusion

Fortuna Mining (TSX: FVI) is no longer a speculative silver play. It has matured into a lean, gold-centric producer with a "flawless" balance sheet and significant exploration upside. While the 7% jump on Jan 5 reflects the immediate surge in metal prices, the long-term thesis rests on the company's ability to execute its expansion at Séguéla and bring Diamba Sud into the fold.

Please wait processing your request...

Please wait processing your request...