_01_23_2026_17_05_41_607834.jpg)

G Mining Ventures Corp. (TSX: GMIN) has captured the spotlight on the Toronto Stock Exchange today, January 23, 2026, with a robust 4.5% surge that underscores its emergence as a premier mid-tier gold producer. This upward momentum is fueled by a confluence of high-impact operational catalysts and a macroeconomic environment where gold prices are testing historic thresholds.

As the company transitions from a developer to a multi-asset producer, the market is aggressively pricing in the "production sprint" outlined in its latest guidance. With its flagship Tocantinzinho mine in Brazil reaching a steady state and the world-class Oko West project in Guyana clearing major construction hurdles, GMIN is increasingly viewed by institutional and retail investors alike as a high-growth vehicle within a traditionally defensive sector.

Latest Key Reasons for the Surge and Market Drivers

Source: Kalkine Group

The primary driver behind today’s 4.5% gain is the market’s continued digestion of the comprehensive 2026-2027 operational guidance released earlier this week. Investors are reacting to the clarity provided regarding the company’s ability to scale production while maintaining a competitive cost structure.

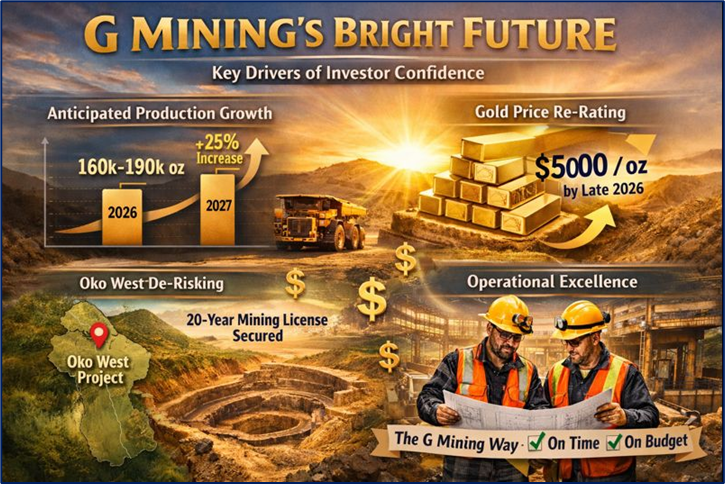

- Anticipated Production Growth: The 2026 guidance projects gold production between 160,000 and 190,000 ounces, with a significant 25% jump expected in 2027 as higher-grade Phase 2 ore becomes accessible (GlobeNewswire, Jan 20, 2026).

- Gold Price Re-rating: Macroeconomic sentiment has shifted as institutional forecasts now project gold toward the $5,000/oz mark by late 2026. G Mining’s leverage to these spot prices, combined with its low-cost profile, makes it a top candidate for a systemic re-rating (Canada Newswire, Jan 15, 2026).

- Oko West De-risking: The recent receipt of the 20-year mining license for the Oko West project in Guyana has removed a significant regulatory overhang, allowing for the initiation of pre-production open-pit mining in Q1 2026 (Company Release, Jan 13, 2026).

- Operational Execution: Unlike many peers facing inflationary pressures, GMIN has demonstrated a disciplined adherence to timelines and budgets, which has bolstered investor confidence in their "G Mining Way" of self-perform construction.

Current Business Model and Operational Framework

G Mining Ventures operates under a differentiated business model that prioritizes internal technical expertise to minimize capital risk and maximize returns during the mine-building phase.

- Self-Perform Construction: The company utilizes an in-house team (G Mining Services) to manage engineering and construction, a strategy that has historically kept projects like Tocantinzinho on budget and on schedule.

- Hub-and-Spoke Growth: The business model focuses on acquiring high-quality, permitted, or near-permitting assets in stable mining jurisdictions (Brazil and Guyana) and applying a standardized development blueprint.

- Dual-Asset Foundation: The current model is built on two pillars: the cash-flowing Tocantinzinho (TZ) mine in Brazil and the high-growth Oko West project in Guyana, which is targeted for first gold in H2 2027.

Latest Financial, Operational, and Dividend Updates (company source)

Recent corporate filings and news releases provide a transparent look at the company’s fiscal health and production trajectory as of January 2026.

- Production Outlook: 2026 production at TZ is expected to be weighted toward the second half of the year (62%), as higher-grade mineralization becomes available in the mine plan (GlobeNewswire, Jan 20, 2026).

- Cost Management: For 2026, All-In Sustaining Costs (AISC) are projected to range between $1,230 and $1,444 per ounce, assuming a gold price of $4,000. Costs are expected to drop by approximately 20% in 2027 as grade and throughput increase (Company Release, Jan 20, 2026).

- Capital Allocation: The company has committed approximately $423 million to Oko West to date (44% of upfront capital), with $514 million to $568 million in growth capital planned for 2026 (Markets Insider, Jan 20, 2026).

- Dividend Policy: Currently, G Mining Ventures does not pay a dividend, opting instead to reinvest free cash flow from its Brazilian operations into the construction and exploration of Oko West and the Gurupi project (Morningstar, Jan 22, 2026).

- Exploration Budget: 2026 marks the largest exploration program in company history, with a budget of $42 million to $50 million dedicated to resource expansion (GlobeNewswire, Jan 20, 2026).

Latest SWOT Analysis (January 2026)

Source: Kalkine Group

Strengths

- Strong Balance Sheet: Significant cash position and a $350 million revolving credit facility provide ample liquidity for growth.

- Execution Record: Proven ability to build and operate mines in South America with minimal delays.

- High-Grade Assets: Ownership of one of the largest undeveloped gold resources in Guyana (Oko West).

Weaknesses

- Concentration Risk: Revenue is currently dependent on a single operating mine (Tocantinzinho) until Oko West comes online.

- High Capital Requirements: Sustained heavy spending on construction at Oko West could strain cash reserves if gold prices see a sudden, sharp downturn.

Opportunities

- Resource Expansion: Ongoing drilling at the Gurupi project in Brazil could lead to a third major production center.

- Gold Price Appreciation: Continued central bank demand and inflation could drive realized gold prices significantly higher than the $4,000 baseline used in guidance.

Risks

- Geopolitical Stability: Potential for regulatory shifts in South American jurisdictions.

- Execution Risk: Any delays in the H2 2027 target for first gold at Oko West could dampen current market sentiment.

- Currency Volatility: Exposure to fluctuations in the Brazilian Real (BRL) and Canadian Dollar (CAD) against the US Dollar.

Outlook and Risk Profile

The outlook for G Mining Ventures for the remainder of 2026 is decidedly bullish, predicated on its transition toward a 500,000-ounce annual production profile by 2028. Analysts are closely watching the "Phase 2" transition at Tocantinzinho in H2 2026, which is expected to trigger a significant increase in free cash flow. However, the risk profile remains moderate-to-high, as is standard for development-heavy mining firms. The primary risks involve the heavy capital expenditure cycle required to bring Oko West to fruition and the inherent volatility of the global commodities market.

Compelling Conclusion

G Mining Ventures is no longer just an exploration story; it is a rapidly maturing producer that has successfully navigated the "developer's gap." Today’s 4.5% rise reflects a market that is gaining confidence in the company's ability to hit its aggressive 2026 milestones. With a clear path to becoming a half-million-ounce gold producer and a world-class asset currently under construction in Guyana, GMIN stands as a focal point for those seeking exposure to the current gold bull cycle through a management team that has consistently delivered on its promises.

Please wait processing your request...

Please wait processing your request...