G Mining Ventures Corp. (TSX: GMIN) capped off a stellar week on December 19, 2025, with its stock price jumping 5.23% to close at CAD 41.66. This rally isn't just a flash in the pan; it reflects a massive 283% gain over the past year, significantly outperforming the broader TSX 300 Composite Index.

As the company transitions from a single-asset developer to a multi-asset "mid-tier" producer, retail and institutional interest is hitting an all-time high.

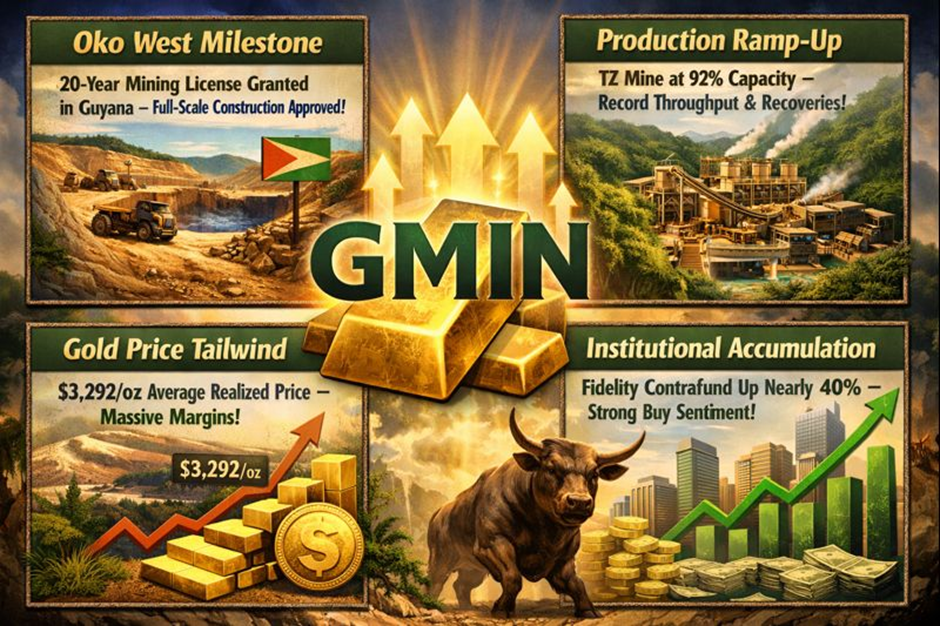

Key Reasons & Drivers for the Dec 19 Surge

Source: Kalkine Group

- Oko West Milestone: The primary catalyst was the Dec 8 announcement that Guyana has officially granted a 20-year Mining License for the Oko West Gold Project. This was the final major regulatory hurdle before full-scale construction.

- Production Ramp-Up: The Tocantinzinho (TZ) Mine in Brazil is now operating at 92% of nameplate capacity, hitting record throughput and recoveries.

- Gold Price Tailwind: With realized gold prices averaging $3,292/oz in Q3/Q4, GMIN is capturing massive margins against its low-cost production profile.

- Institutional Accumulation: Fund sentiment has turned "Strong Buy," with major players like Fidelity Contrafund increasing their positions by nearly 40% in recent months.

SWOT Analysis: The GMIN Outlook

Source: Kalkine Group

Latest Business Model: The "Self-Perform" Strategy

Unlike many junior miners that outsource construction, GMIN utilizes a Self-Perform Business Model. By acting as their own EPC (Engineering, Procurement, and Construction) firm, they eliminate the "margin on margin" typically paid to third-party contractors. This allows them to:

- Lower Initial Capex: Historically saving 10-15% on build costs.

- Accelerate Timelines: Moving from construction decision to first gold faster than the industry average.

Financial & Operational Updates (Q4 2025)

- Revenue Surge: Reported record quarterly revenue of $161.7 million (up 25% from the previous quarter).

- Cash King: Generated $95.8 million in Free Cash Flow (FCF) in the most recent quarter alone—a 59% jump.

- Tax Incentives: Secured the SUDAM tax-incentive in Brazil, slashing their nominal corporate tax rate from 34% down to 15.25% for the next decade.

- Balance Sheet: Ended the year with over $156 million in cash and an untapped $350 million credit facility to fund Oko West.

The Risks: What to Watch

While the momentum is bullish, investors should monitor:

- Execution Risk: Moving Oko West into full construction in Q1 2026 is a massive undertaking.

- Technical Overbought Signals: The RSI (Relative Strength Index) recently hit 79, suggesting the stock is technically overextended in the short term.

- Inflationary Pressures: While one-time fleet purchases are complete, labor and energy costs in Brazil and Guyana remain volatile.

Conclusion

G Mining Ventures has successfully shed its "developer" label to become a cash-flow-generating machine. With the TZ mine firing on all cylinders and the "world-class" Oko West project now fully licensed for construction, the company is on a clear path to becoming a 500,000+ ounce per year producer. The December 19 rally confirms that the market is finally pricing in GMIN as a premier mid-tier gold play rather than a speculative junior.

Source: Trading View, 19 December 2025

Please wait processing your request...

Please wait processing your request...