The stock of Galleon Gold Corp. (TSXV: GGO) experienced a significant one-day surge of 24.0% on the TSX Venture Exchange (TSXV) on December 15, 2025. This move suggests a strong positive reaction from the market to recent corporate developments and a favorable shift in investor sentiment toward the company's prospects.

Key Reasons and Drivers for the Stock Jump

The sharp increase appears to be driven by a confluence of recent, highly positive corporate and financial announcements:

- Major Strategic Funding & Partner Endorsement: The most significant driver is the successful closing of an oversubscribed C$30 million equity financing, which included lead orders from major institutional players:

- Pan American Silver Corp. (PAAS): A significant strategic investment by a major senior miner lends substantial credibility and a strong vote of confidence in Galleon Gold's flagship project. Pan American Silver is reportedly moving towards a near-20% ownership position and has provided an indicative term sheet for a C$46 million debt facility, which greatly de-risks the path to development.

- Eric Sprott: Continued, and increased, investment from this prominent resource investor further validates the project's potential.

- Project De-Risking and Advancement: The substantial capital infusion is earmarked to advance surface infrastructure and underground development for a planned 86,500-tonne bulk sample program at the West Cache Gold Project. This bulk sample is a critical step in technical studies (feasibility) and de-risking the asset toward potential near-term production.

Source: Kalkine Group

Latest Business Updates and Project Status

The company's recent activity centers entirely on financing and advancing its main asset:

- Financing Closure (Early Dec 2025): Closed the oversubscribed C$30 million equity financing, cementing the key strategic investments from Pan American Silver and Eric Sprott.

- Debt Facility Indication (Late Nov 2025): Received an indicative term sheet for a significant C$46 million debt facility from Pan American Silver, signaling a pathway for full project funding.

- Royalty Repurchase: A portion of the proceeds is allocated to repurchasing a 3% Net Smelter Royalty (NSR) on the West Cache Gold Project. Repurchasing a royalty directly improves the future cash flow economics of the project, increasing its net present value (NPV).

- West Cache Gold Project (Flagship): The company is focused on its advanced exploration and development gold project near Timmins, Ontario, a prolific Canadian mining camp. The immediate objective is to execute the large-scale bulk sample program to gather data for feasibility studies and ultimately position the asset for production.

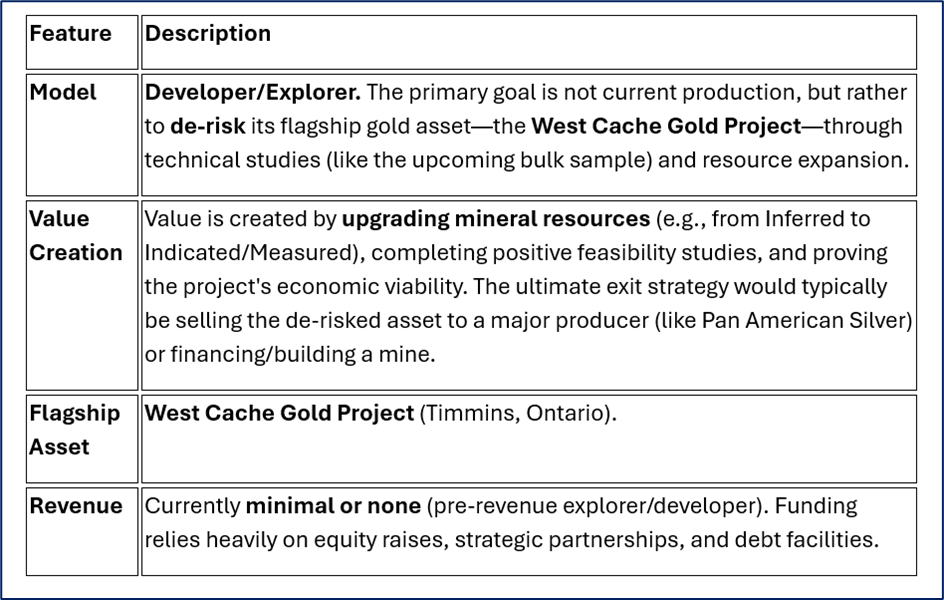

Galleon Gold's Business Model

Galleon Gold operates as an Advanced Exploration and Development Company in the gold sector.

Source: Kalkine Group

Key Risks for Analytical Consideration

As a junior resource company, Galleon Gold faces inherent risks:

- Exploration and Development Risk: There is no guarantee that the bulk sample program will yield the expected economic results or that the inferred resources will be converted to reserves with demonstrated economic viability.

- Commodity Price Volatility: The project's ultimate profitability is highly dependent on the worldwide price of gold. Significant price drops could render the project uneconomic.

- Financing and Dilution Risk: While a major financing has closed, future funding will be required for mine construction. Equity raises can lead to dilution of existing shareholders, and debt financing adds interest and repayment obligations.

- Permitting and Regulatory Risk: The ability to move from exploration to commercial mining requires securing numerous environmental, social, and regulatory permits, which can be time-consuming and uncertain.

- Concentration Risk: The stock's performance is heavily tied to the West Cache Gold Project and the continued involvement and support of strategic partners like Pan American Silver.

Conclusion: Analyst Viewpoint

The 24% surge in Galleon Gold's stock is a strong indication that the market is decisively re-rating the company based on major de-risking events. The C$30M financing and the powerful endorsement via strategic investment and potential debt from Pan American Silver have significantly mitigated financing and project credibility risks. The company has moved from a pure explorer to an advanced developer with a clear, funded path to a bulk sample, which is analytically significant. The current focus must now shift to the successful execution of the bulk sample and the conversion of resources into viable reserves to justify the new, higher valuation.

Source: Trading View, 15 December 2025

Please wait processing your request...

Please wait processing your request...